You spot the issue late. A rental property expense was treated incorrectly. A CIS figure was carried through from records that looked fine at the time. A company tax return from a prior period now shows you paid more than you should have, but the normal amendment route has closed.

That's usually the moment people assume the money is gone.

Sometimes it is. Often it isn't. An overpayment relief claim is HMRC's formal route for recovering tax that was overpaid because of a genuine mistake after the usual correction options have fallen away. For landlords, small companies, sole traders, and construction businesses, it can be the difference between writing off an old error and getting cash back that still belongs to the business.

Generic guidance tends to stop at “write to HMRC and explain the mistake”. That's not enough. Claims fail on technical points, and two of the most overlooked are the ones that cause the most frustration in practice: the declaration signed by the wrong person, and the construction-specific problem of relying on guidance that counted as prevailing practice at the time.

If you're reviewing older returns as a sole trader, this practical guide on tax for sole traders is also worth keeping nearby because overpayments often start with missed deductions or miscategorised expenses. If your concern is tied to balancing historic liabilities with current liabilities, it also helps to understand payments on account so you don't confuse a real overpayment with a timing issue.

Table of Contents

- Have You Overpaid Tax? Understanding Overpayment Relief

- Checking Your Eligibility for an Overpayment Relief Claim

- How to Prepare and Submit Your Overpayment Relief Claim

- Common Pitfalls That Invalidate Overpayment Relief Claims

- Sector-Specific Examples for UK Businesses

- When to Engage an Accountant for Your Claim

Have You Overpaid Tax? Understanding Overpayment Relief

An overpayment relief claim is a formal request to HMRC to repay tax that was overpaid because of an error, omission, or misinterpretation of tax law, where the normal correction route is no longer available. It isn't a shortcut. It's a fallback remedy for genuine mistakes.

That matters because people often use the term loosely. They say they want to “claim tax back” when what they need is a return amendment, an appeal, or a recalculation. Overpayment relief sits in a narrower category. It comes into play when the ordinary fix has already expired.

The basic test

A valid claim has to be rooted in a real mistake. If you merely prefer a different treatment with hindsight, or you're revisiting an accounting choice because it now looks less tax-efficient, that won't usually get you there.

The claim also has to stand on its own facts. HMRC expects you to identify what went wrong, which year was affected, and what amount was overpaid. Vague letters rarely help.

Practical rule: If you can't explain the original error in one plain sentence, you probably aren't ready to file the claim yet.

Typical situations include:

- Landlords finding omitted reliefs or duplicated income entries in an older return.

- SMEs discovering bookkeeping errors that fed into corporation tax or personal tax figures.

- Construction firms revisiting CIS-related positions after a detailed records review.

- Directors spotting personal tax overstatements linked to dividends, expenses, or reporting mistakes.

A useful check before doing anything else is to gather the original return, the working papers behind it, and the records that now show the figure should have been different. If you're sorting through a large bundle of statements, invoices, and tax papers, tools that help organise and search financial records can speed things up. Something like this AI agent for finance documents can help you identify the paperwork you'll need before you commit time to the claim itself.

The deadline that decides everything

The most important gatekeeper is the time limit. In the UK, the statutory limit for an overpayment relief claim is four years from the end of the relevant tax year for individuals or the accounting period for companies, and HMRC doesn't extend that deadline. A claim for the 2021/22 tax year must be filed before 5 April 2026, according to this HMRC overpayment relief time limit guide.

That deadline catches people out because the clock runs from the tax year or accounting period, not from the day you discovered the error. If you're unsure whether the original return could still be corrected by the standard route instead, checking the difference between amendment windows and formal claims is a sensible first step. For personal filings, this overview of Self Assessment tax return help can help you separate those routes properly.

Checking Your Eligibility for an Overpayment Relief Claim

A landlord finds an old property return error after a mortgage review. A construction company spots CIS deductions that were never given full credit. Both situations look fixable on the numbers. That does not mean both qualify for overpayment relief.

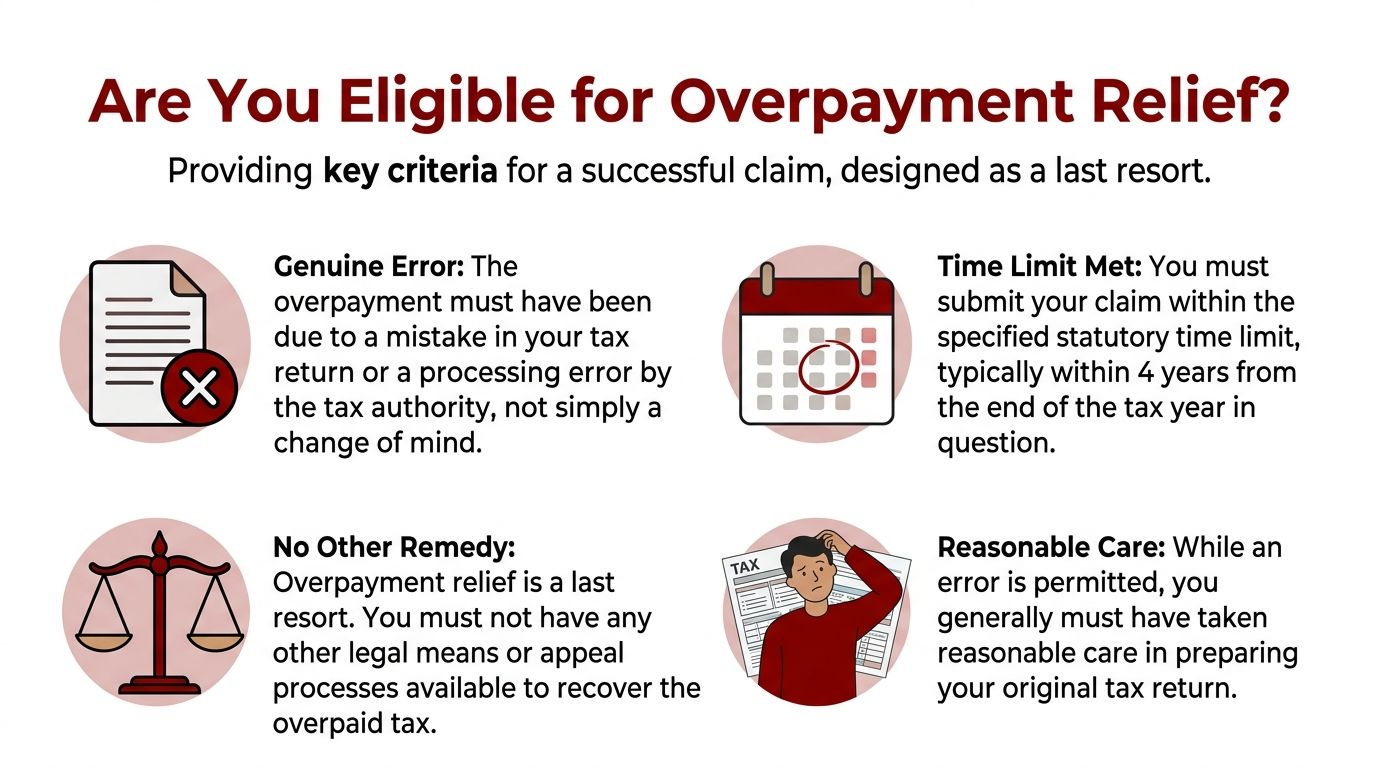

Eligibility is where weak claims usually fail. HMRC is not just asking whether too much tax was paid. It is asking whether this is the correct legal route, whether the claim is still in time, and whether the claim is being made by the right person in the right form.

HMRC's Strict Eligibility Checklist

Start with the cause of the overpayment. Overpayment relief is meant for cases where the original return or assessment was wrong because of an error, omission, or mistaken understanding of the facts or law. It is not there to rescue a late change of approach, or to reopen a point that could still be dealt with through an amendment, enquiry, or appeal.

In practice, I tell clients to test five points before any drafting starts:

- There was a genuine error in the original filing position. A revised preference or a better tax outcome found later is not enough.

- Another remedy is no longer available. If the return can still be amended, or an appeal route is still open, HMRC will usually expect that route to be used instead.

- The overpayment can be calculated properly. A claim needs a worked figure, not a rough estimate.

- The claimant can support the correction with records. For landlords, that might be tenancy records, invoices, and finance statements. For contractors, CIS statements and contract records are often central.

- The declaration will be signed correctly. This is a common rejection point, especially where an agent signs without the right wording or authority.

That last point gets missed far too often. An accountant can prepare the claim, but HMRC still expects the taxpayer, partner, trustee, or authorised company officer to make the declaration properly. We see claims delayed or rejected because the numbers were right but the signature was wrong.

If you are still within the normal amendment window, overpayment relief is usually the wrong tool. For personal returns, it helps to check the normal correction route first using this guide to Self Assessment tax return help.

Two overlooked rejection risks

Two issues catch out otherwise sensible claims.

The first is the agent signature flaw. A covering letter on an accountant's letterhead is not enough by itself. If the formal declaration is not made by the correct person, or the agent does not have the right authority for the exact claim being made, HMRC may refuse the claim without getting into the tax analysis at all.

The second is the prevailing practice trap. This matters particularly for construction firms and some owner-managed businesses. If the original treatment followed what was generally accepted practice at the time, HMRC can resist overpayment relief even where a later review suggests too much tax was paid. Contractors run into this with CIS treatment, subcontractor status issues, and industry habits that were followed routinely but not challenged at the time. It is one of the reasons these claims need careful framing rather than a simple recalculation.

An AI agent for finance documents can help organise old returns, CIS statements, and supporting records before you decide whether the claim is worth pursuing.

A practical filter before you spend time on the file

| Question | If yes | If no |

|---|---|---|

| Was the original tax position actually wrong? | Keep reviewing eligibility | Stop and check whether this is only a later preference change |

| Is the usual amendment or appeal route closed? | Overpayment relief may be appropriate | Use the ordinary route instead |

| Can you show the corrected tax figure clearly? | Prepare the evidence file | Rework the calculation first |

| Will the declaration be signed by the correct person? | Draft the claim | Fix authority and sign-off first |

| Could HMRC argue the original treatment followed prevailing practice? | Review the technical position carefully | Lower risk on this point |

The Four-Year Rule in Practice

The time limit still needs checking early, but the practical issue is often simpler than clients expect. Count from the end of the relevant tax year for individuals, or from the end of the accounting period for companies. If that date has passed, the claim is usually finished before it starts.

Check the date first. Then check the legal route. Then check the evidence. That order saves time, and it prevents businesses from spending hours preparing claims HMRC was always going to reject.

How to Prepare and Submit Your Overpayment Relief Claim

A typical problem looks like this. A contractor finds an old return understated CIS deductions, or a landlord spots expenses that were omitted years ago. The tax has been overpaid, the normal amendment window has gone, and HMRC will only consider the claim if the paperwork is technically right first time.

A good overpayment relief claim starts with the corrected result and works back to the evidence. That approach keeps the file focused and reduces the risk of sending HMRC a long letter with no clear tax calculation behind it.

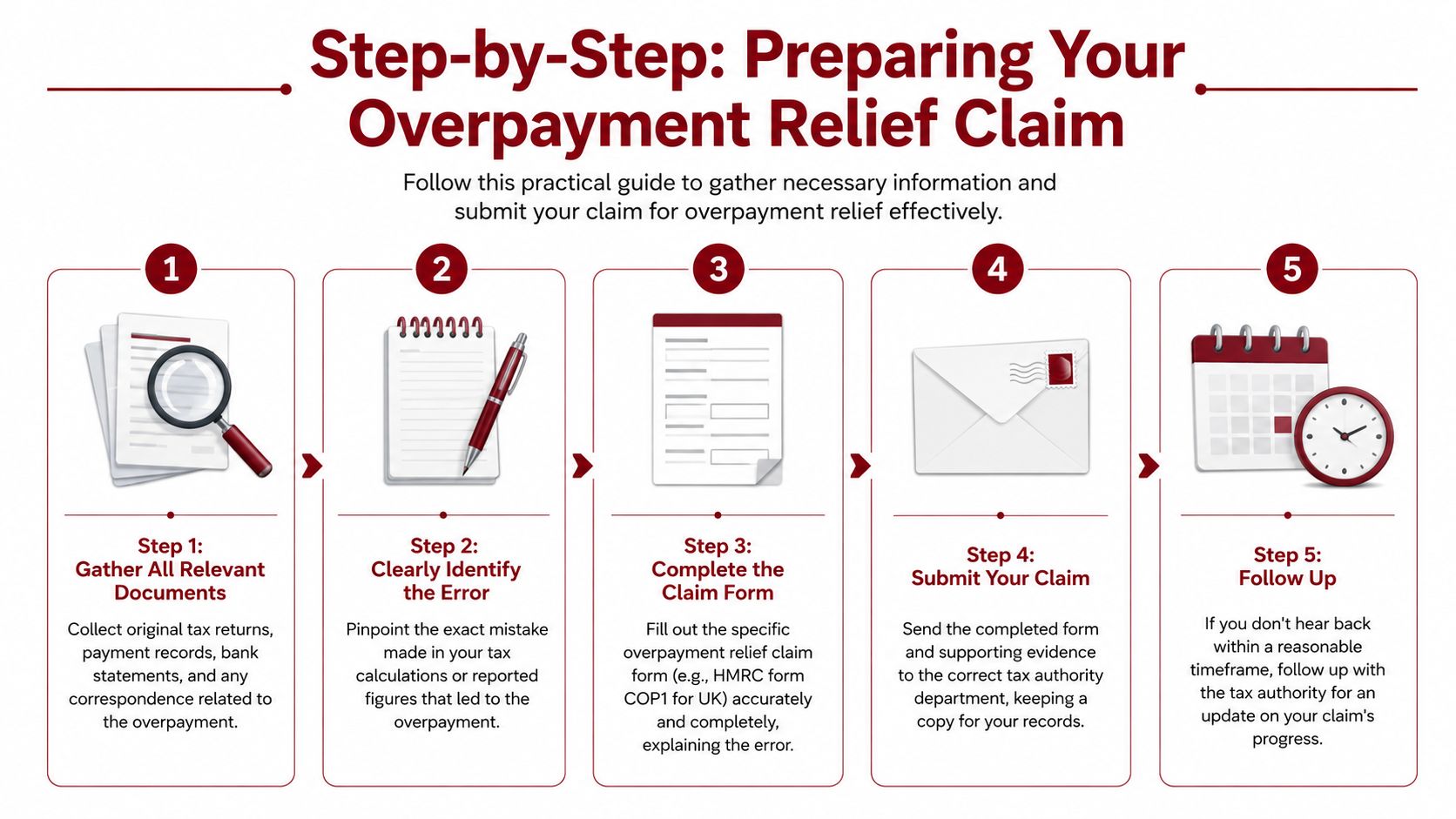

Build the file before you draft the letter

Start by assembling the documents that prove three separate points. What was filed originally. What the correct position should have been. How the difference produces the overpayment.

In practice, that usually includes:

- Original submission documents such as the tax return, computation, and supporting schedules.

- Correcting evidence such as invoices, bank statements, tenancy records, CIS deduction statements, or bookkeeping reports.

- A clear recalculation showing the corrected tax liability and the amount overpaid.

The supporting records vary by trade. For a landlord, the file often turns on rental accounts, finance costs, repair invoices, and the property pages that used the wrong figure. For a construction business, we usually review CIS statements, subcontractor records, contract income schedules, and the working papers used in the original return. For a limited company, the useful evidence is often the nominal ledger, year-end journals, and the original versus corrected tax computation.

If the issue sits in corporation tax, compare the original and revised computations side by side before you write the claim. That usually exposes weak spots quickly. It also helps directors understand why the figure has changed. If you need context on how the return and computation interact, this guide to corporation tax return support is a sensible starting point.

What the claim must say

The claim needs to be formal and precise. It must be made in writing, it must clearly state that it is a claim for overpayment relief, and it must identify the relevant tax year or accounting period and the amount being claimed.

It also needs a proper declaration and signature from the right person. That point is missed more often than clients expect. If an agent signs instead of the taxpayer, company officer, or nominated partner, HMRC can reject the claim without getting as far as the tax analysis. We see that with SMEs regularly, especially where the accountant has prepared everything and the signature is treated as an admin step at the end.

The letter should also explain, briefly and directly:

-

What period the claim covers

State the exact tax year or accounting period. -

What the error was

Describe the mistake in plain terms. -

What the corrected position is

Show the revised tax figure and how the overpayment arises. -

Why overpayment relief is the correct route

Confirm that no amendment, appeal, or other statutory remedy is still open. -

Who is making the declaration

Ensure the signature comes from the taxpayer personally, a company officer, or the nominated partner.

Short, factual wording is usually best. For example:

I am making a claim for overpayment relief in respect of the tax year [year]. The overpayment arose because [brief explanation of the error]. The amount overpaid is [amount]. No other statutory remedy is available. I declare that the information in this claim is correct and complete to the best of my knowledge and belief.

Keep the tone businesslike. HMRC is looking for a valid claim supported by evidence, not a long account of how the mistake happened.

One technical point deserves attention before anything is posted. Construction firms are especially exposed to the "prevailing practice" issue. If the original return followed an approach that was widely used at the time, HMRC may argue overpayment relief is blocked even if the treatment now looks wrong. That needs checking before the claim is drafted, not after rejection. Landlords can face similar issues where older property treatment was adopted consistently without being challenged.

To see a walk-through of the process in action, this short video can help frame the practical steps:

Where to send it

The claim is made separately. It does not go into a routine return or a standard amendment.

The process described in this overpayment relief process guide notes that income tax and capital gains tax claims are sent to PAYE Self-Assessment at BX9 1AS, while corporation tax claims go to Corporation Tax Services at BX9 1AX.

Send a complete copy file with the claim. Include the signed declaration, the calculation, and the key evidence. For larger files, add an index and label the attachments clearly. That small bit of discipline makes review easier and helps prevent the underlying issue being buried under paperwork.

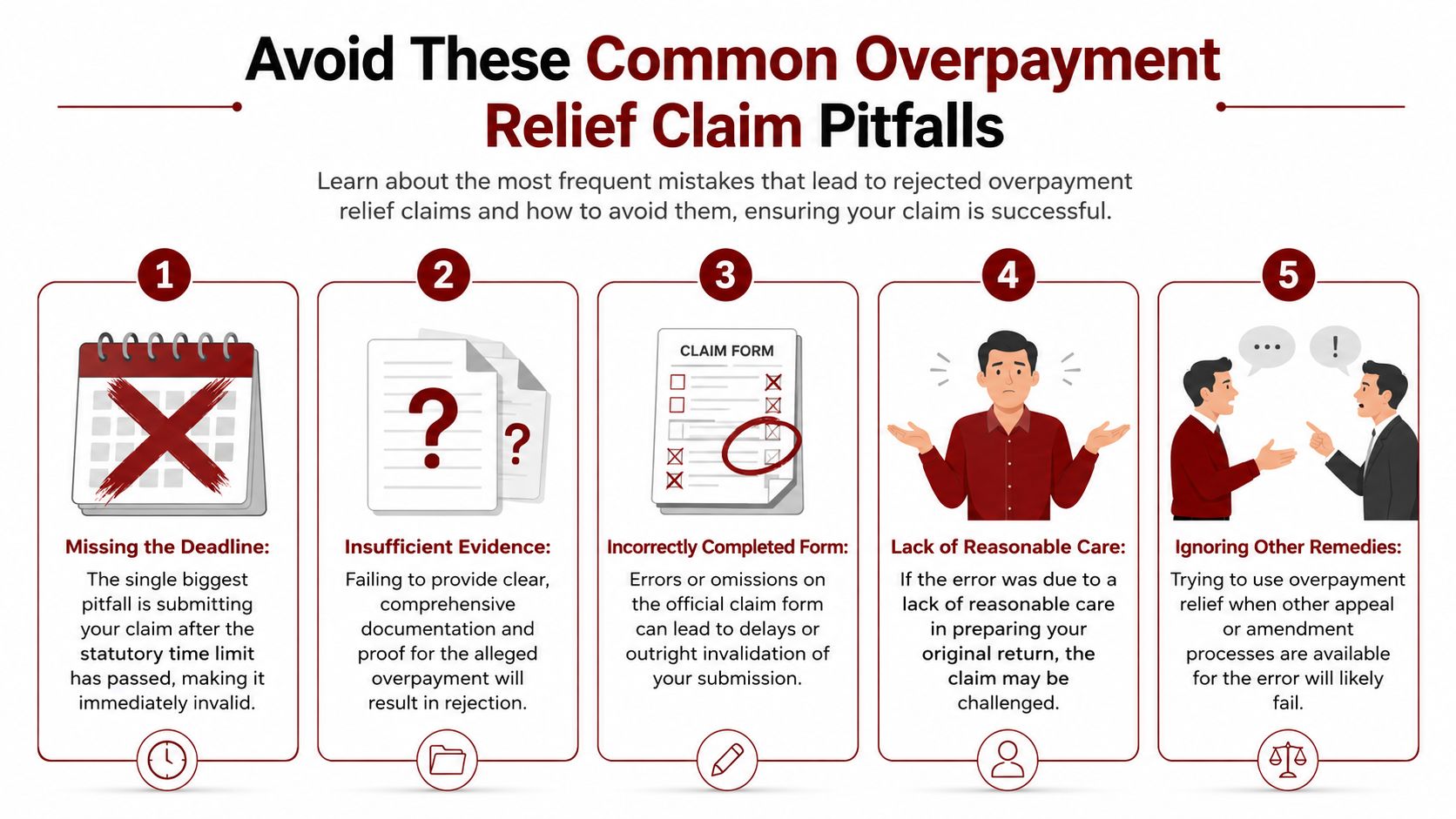

Common Pitfalls That Invalidate Overpayment Relief Claims

A lot of rejected claims are not rejected because the tax analysis is weak. They're rejected because the claim was invalid from the moment it was filed.

The agent signature flaw

This is the trap most generic guides barely mention. HMRC will automatically reject overpayment relief claims if the signed declaration is made by a tax agent rather than the taxpayer or company officer. Updated guidance says the signature must come from the taxpayer, a company officer, or the nominated partner, as explained in ICAEW's note on updated guidance on claims for overpayment relief.

That catches business owners by surprise because they assume their accountant can sign anything tax-related on their behalf. For most routine interactions, the agent handles the process. Not here.

If you run a limited company, a director or other authorised company officer needs to sign. If you're an individual landlord or sole trader, you sign personally. If it's a partnership case, the nominated partner signs.

Don't leave the signature step until the end. For some businesses, getting the correct sign-off is the slowest part of the entire submission.

Other mistakes that sink valid claims

The signature issue is the standout procedural flaw, but it isn't the only one.

-

Using overpayment relief when another remedy was available

If the return could still have been amended at the time, HMRC may say the claim doesn't qualify. -

Describing the issue too vaguely

“Tax was overpaid” is a conclusion, not a ground of claim. HMRC needs the mechanism of the error. -

Submitting weak evidence

A claim without the documents behind the revised figures looks speculative, even if you know the answer is right. -

Treating the claim like a negotiation

This isn't a goodwill request. It's a statutory claim. Precision matters more than persuasion. -

Ignoring prevailing practice issues

This is especially important for contractors and deserves separate thought before filing anything.

A practical way to reduce rejection risk is to review the claim against a short pre-submission list:

| Check | What to confirm |

|---|---|

| Signature | Signed by the taxpayer, company officer, or nominated partner |

| Claim wording | Clearly states it is for overpayment relief |

| Period | Exact tax year or accounting period identified |

| Amount | Exact overpayment stated |

| Evidence | Supporting documents match the corrected figures |

The harsh reality is that a technically valid tax argument can still fail if the submission mechanics are wrong.

Sector-Specific Examples for UK Businesses

The rules make more sense when you see how they play out in ordinary business situations.

Construction contractors and CIS

A contractor reviews older records and realises too much tax was borne because CIS treatment was applied in line with guidance that was understood one way at the time, then later clarified differently. On the surface, that sounds like a classic refund case.

The problem is the prevailing practice rule. HMRC bars overpayment relief where the original return followed HMRC's published guidance or prevailing practice at the time. That's a major hurdle for construction businesses dealing with changing CIS interpretations, as discussed in this overview of overpayment relief and prevailing practice.

Contractors often feel unfairly treated. They followed what was then accepted. Later clarification suggests the tax burden was heavier than it needed to be. But overpayment relief isn't designed to reopen every return affected by evolving interpretation.

What works here is caution before claiming. Review whether the original position was an error in your records or computation, or whether it was the accepted treatment at the time. If it's the latter, an overpayment relief claim may be blocked.

For CIS cases, the first question isn't “Did we pay too much?” It's “Why was the return wrong?”

Landlords with missed property reliefs

A landlord spots an issue in an older return after reviewing property expenses. The original figures were based on incomplete records, and a legitimate property deduction wasn't reflected. The amendment window has gone, but the paperwork exists and the corrected computation is clear.

That can be a workable claim if the error was genuine and the records support it. The strongest landlord files usually include:

- The original property pages or computation

- The invoices or statements behind the missed expense

- A revised rental profit calculation

- A short written explanation of how the error arose

What doesn't work is treating a retrospective tax planning idea as if it were an old mistake. If the issue is a fresh preference about how to present the return, that's different from a true omission.

Small companies with accounting misclassifications

A common SME problem is a bookkeeping misclassification that flows into the tax computation. For example, a significant business purchase was posted one way, the corporation tax position followed that bookkeeping, and a later review shows the tax treatment should have been different.

In these cases, HMRC will usually expect the company to do more than assert the final number. The company needs to trace the path from bookkeeping entry to tax computation to overpayment. A persuasive file often includes the nominal ledger detail, year-end journals, invoices, and the revised computation.

The trade-off is time. Straightforward claims can be assembled relatively cleanly. Multi-layered company claims can become document-heavy fast, especially where director transactions, VAT interactions, or prior adviser working papers are involved.

The lesson across all three examples is the same. The best claims are not the most forceful. They are the most coherent.

When to Engage an Accountant for Your Claim

Some overpayment relief claims are manageable without much outside help. Some really aren't. The sensible dividing line is complexity, not confidence.

When a DIY claim can work

A do-it-yourself approach can work where the error is narrow, the records are complete, and the corrected position is easy to show. That usually means one tax year, one clear mistake, and a straightforward recalculation.

Examples include a landlord correcting an obvious omitted expense with clean invoices, or an individual correcting a duplicated income figure where the records line up neatly. In those cases, the main challenge is following HMRC's format properly and getting the declaration signed by the right person.

If you do it yourself, be disciplined:

- Write the claim formally

- Attach the corrected figures

- Keep the explanation short and exact

- Check the signatory before posting

- Retain a full copy of the submission

When getting help is the safer route

Professional help is worth considering when the risk of getting it wrong is higher than the cost of support. That usually applies where:

- The claim spans more than one period

- The calculation involves corporation tax adjustments

- CIS treatment or construction sector practice is involved

- The records are incomplete or messy

- HMRC has queried related issues before

- You're not sure whether the problem is a genuine error or a blocked prevailing practice case

An accountant's job here isn't just to draft a letter. It's to test whether the claim should be made at all, assemble the evidence properly, and avoid procedural mistakes that can sink a valid case.

If you're weighing up whether outside support is worthwhile more generally, this guide on ways an accountant can help your small business is a useful starting point. For claims like this, the value is usually in reducing avoidable risk.

A good overpayment relief claim is careful, not clever. That's why many clients benefit from having someone challenge the assumptions before anything goes to HMRC.

If you think you may have overpaid tax and want a clear view on whether a claim is still viable, Action Accountants Limited can help you review the facts, test the technical position, and prepare a compliant submission without unnecessary delay.