Your Corporation Tax Return: A Guide to the CT600 in 2026

Action Accountants •4 July 2026

You've incorporated the company, opened the business bank account, started invoicing, and then HMRC sends a letter that sounds far more serious than it feels you're ready for. That's a very normal moment for a new director. New directors aren't worried about doing the right thing. They're worried about missing something technical, filing the wrong form, or discovering too late that “no profit” doesn't mean “nothing to do”.

A corporation tax return is one of those jobs that seems simple until you get into the detail. The broad idea is straightforward. You tell HMRC what your company made, what it spent, and what tax is due. The confusion starts when accounting profit and taxable profit aren't the same, when filing and payment deadlines get mixed up, and when marginal relief sits in the middle and catches people who assume they can just apply one rate or the other.

This guide focuses on the two areas new business owners misunderstand most often. First, you still have to file even if the company made no profit or a loss. Second, profits between £50,000 and £250,000 can fall into the marginal relief band, which means the calculation needs more care than many founders expect.

Table of Contents

- That First HMRC Notice and What It Really Means

- What Exactly Is a Corporation Tax Return

- How to Prepare Your Accounts for the CT600 Form

- Calculating Your Corporation Tax Liability Correctly

- Filing Your Return and Paying HMRC on Time

- Common CT600 Mistakes and Costly Penalties

- Special Cases and When to Hire an Accountant

That First HMRC Notice and What It Really Means

The brown envelope tends to land at the wrong time. You're already juggling customers, suppliers, bookkeeping, payroll, and a dozen things that feel more urgent. Then HMRC sends a formal notice asking for a Company Tax Return, and it can read as if you've done something wrong.

You probably haven't.

For most directors, that notice is HMRC acknowledging that your company exists and is now expected to meet its corporation tax obligations. It's part of becoming a functioning limited company in the UK tax system. The letter is formal because the duty is legal, but the message is practical. HMRC wants a return from the company for the relevant accounting period.

Why HMRC takes it seriously

Corporation tax is a major part of the UK tax picture. In the 2025/26 financial year, UK corporation tax receipts are projected to reach approximately £95.1 billion, a total that has grown nearly 2.5-fold over the last decade, according to Statista's UK corporation tax receipts data. That helps explain why HMRC's systems are built around routine filing, automated checks, and quick follow-up where something is missing.

That doesn't mean every return is a minefield. It does mean the process matters.

What the notice is really telling you

Think of the notice as a prompt to get organised rather than a sign of trouble. In practice, it means:

- HMRC expects a CT600 for the period it has identified.

- Your company records now matter in tax terms, not just for your own management.

- The return stands apart from other filings, so filing Companies House accounts or sending a VAT return doesn't replace it.

Practical rule: Don't ignore the first notice because the company “has barely traded”. New companies often create problems by waiting until year end to deal with something HMRC expected them to act on much earlier.

A lot of stress disappears once you translate the letter into plain English. HMRC isn't asking you to become a tax specialist overnight. It's asking your company to submit a proper annual tax return, backed by figures that tie back to its accounts.

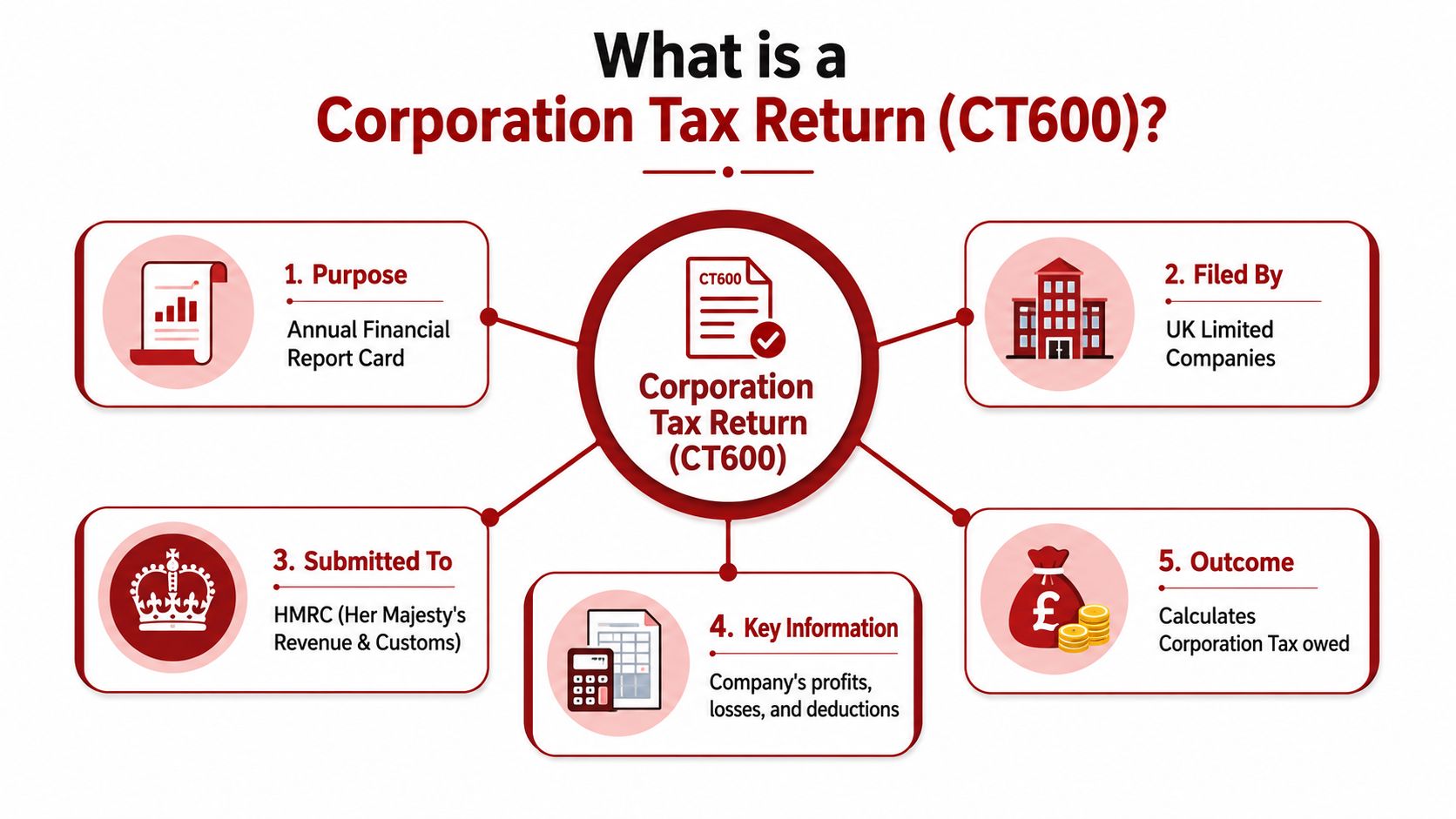

What Exactly Is a Corporation Tax Return

A Corporation Tax Return, usually called the CT600, is the company's tax submission to HMRC. If your statutory accounts are the financial story of the year, the CT600 is the tax version of that story. It tells HMRC what profit or loss the company made and how that turns into a corporation tax position.

For a new owner, the easiest way to think about it is this. Your accounts show how the business performed under accounting rules. Your corporation tax return shows what HMRC wants to tax under tax rules. Those aren't always identical.

What goes into it

The return normally sits alongside your accounts and tax computations. Together, they give HMRC the numbers behind the tax bill. A straightforward company return often needs to reflect:

- Income received from sales, services, fees, rent, or other trading activity

- Expenses incurred in running the business

- Adjustments for tax purposes, where an accounting cost isn't fully deductible

- The final taxable result, whether that's tax due, a loss, or nil liability

That's why the CT600 is not the same as VAT, payroll reporting, or a director's Self Assessment return. Those are separate obligations with different rules.

Who usually needs to file

In practical terms, active UK limited companies should assume they need to deal with corporation tax unless there is a very specific reason otherwise. New owners sometimes assume no revenue means no return. That's a mistake, and it becomes expensive when HMRC's systems record a missing submission.

A better mindset is to assume the company must account for its position each year, even if the answer is “no tax payable”.

The return is about reporting the company's tax position, not just paying tax.

Accounting period versus filing deadline

Many founders often confuse these two concepts. The accounting period is the stretch of time the figures relate to. The filing deadline is the last date by which HMRC wants the return submitted. They are connected, but they are not the same thing.

The same goes for your statutory accounts. They support the return, but they don't replace it.

If you keep that distinction clear, the process becomes much easier to manage. One set of dates relates to the financial period you're reporting on. Another set relates to when HMRC expects the completed corporation tax return and when it expects any tax to be paid.

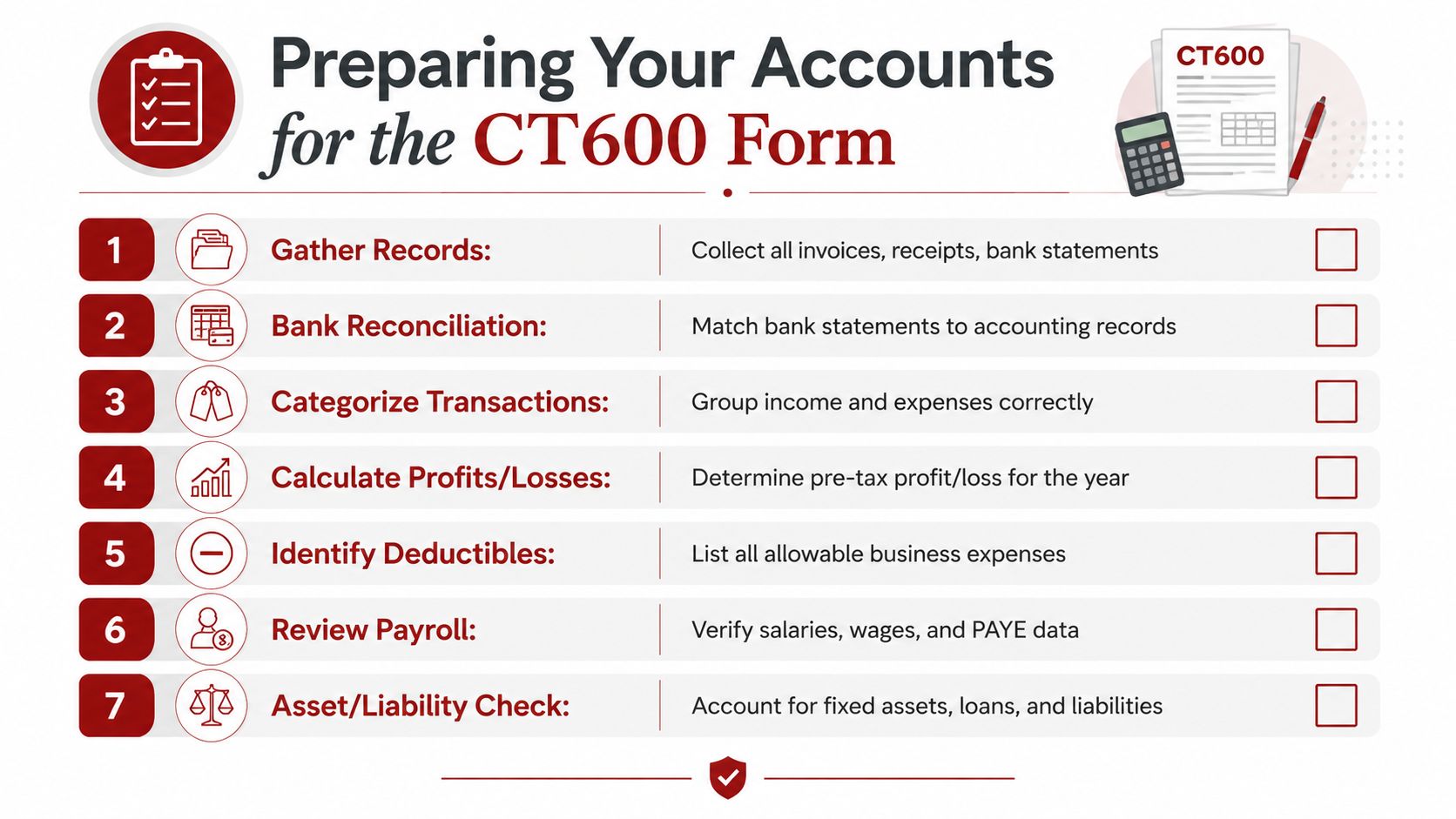

How to Prepare Your Accounts for the CT600 Form

A clean CT600 starts long before the form itself. The best returns come from tidy bookkeeping, reconciled bank records, and clear support for each major balance. If your records are rushed at year end, the tax work becomes slower, more expensive, and more likely to include avoidable mistakes.

Start with the raw material. That means bank statements, sales invoices, purchase invoices, expense receipts, payroll summaries, finance agreements, and records for anything the business bought or sold during the year.

The records to pull together first

If you're doing your own bookkeeping in Xero, QuickBooks, FreeAgent, or spreadsheets, gather the records before you look at the tax form. Don't try to build the return from memory.

- Sales records: invoices issued, credit notes, and anything showing money earned but not yet received.

- Purchase and expense support: supplier bills, card statements, and receipts for business spending.

- Bank and loan paperwork: statements for every account, plus finance and borrowing documents.

- Payroll and pension information: wages, PAYE records, and employer pension contributions where relevant.

- Asset purchases: equipment, vehicles, furniture, and other items that may need capital allowance treatment rather than a simple expense entry.

For founders who want a good discipline around evidence, Receipt Router's HMRC compliance guide is a useful practical reference on keeping records in a way that stands up later if HMRC asks questions.

Turn bookkeeping into year-end accounts

The CT600 doesn't begin with the tax rate. It begins with year-end accounts that are complete and internally consistent. That usually means a profit and loss account, a balance sheet, and supporting schedules for key items such as fixed assets, loans, director balances, accruals, and prepayments.

If you're not sure what should be reviewed before year end is finalised, a simple year-end accounts checklist can help you spot gaps before they become filing problems.

A practical review at this stage often picks up issues such as personal spending posted as business costs, missing loan documentation, duplicate supplier entries, or revenue coded to the wrong period.

What iXBRL means in real life

The technical part that worries many directors is iXBRL. It sounds specialised, but the underlying idea is simple. It's a digital tagging format that lets HMRC's systems read your accounts and computations properly.

Since 2011, all Company Tax Returns, including the CT600 form and accompanying accounts, must be filed online in iXBRL format, and HMRC's automated systems will reject submissions that fail to meet this technical requirement, as set out in HMRC's guidance on the format for online Company Tax Returns.

That matters because a return can be wrong in two different ways. The tax can be wrong. Or the format can be wrong. Either creates delay.

This short video gives a useful overview before filing work starts:

What works and what doesn't

What works is boring but effective. Keep bookkeeping current, reconcile monthly, and separate business from personal spending. Review the year-end trial balance before anyone starts the corporation tax return.

What doesn't work is treating the CT600 as a standalone form-filling exercise. Once the accounts are messy, every later step gets harder.

Calculating Your Corporation Tax Liability Correctly

This is the part directors usually mean when they say, “I just want to know what I owe.” Fair enough. But the answer only works if you start with the right profit figure.

Your accounting profit is not always your taxable profit. Some costs are allowable for tax. Some aren't. Some asset purchases may need capital allowance treatment instead of going straight through the profit and loss account. That means the tax computation adjusts the accounts before the corporation tax rate is applied.

Start with taxable profit, not bookkeeping profit

A sensible workflow looks like this:

- Take the accounting profit or loss from the year-end accounts.

- Review expenses that may be disallowable for corporation tax purposes.

- Check capital items that may need capital allowances instead of ordinary expense treatment.

- Arrive at taxable total profits before applying the relevant rate or relief.

Founders often go wrong by assuming bookkeeping software has already done the tax thinking for them. It usually hasn't.

A common flashpoint is money moving between the company and the director. If the bookkeeping around drawings, repayments, or company-paid personal costs is muddled, the tax picture gets muddled too. If that area sounds familiar, it's worth understanding how a director's loan account works before finalising the return.

The rates many owners know, and the part they miss

For UK resident companies with augmented profits below £50,000, the lower corporation tax rate is 19%. For companies with profits above £250,000, the main rate is 25%. The awkward middle ground is where marginal relief can apply.

This is not a niche point. Confusion over marginal relief for profits between £50,000 and £250,000 is a primary driver of tax liability errors for startups, with 42% of UK SMEs in this profit band filing incorrect returns in 2025, according to HMRC's Tax Confident guidance.

A worked example of marginal relief

Suppose a fictional company has taxable profits that fall between the lower and upper thresholds. Many founders try one of two bad shortcuts. They either apply 19% to the whole amount because the company is “small”, or they jump straight to 25% because profits are above the lower threshold.

Neither approach captures the taper correctly.

The right answer is to calculate marginal relief using HMRC's method for companies in that band. In practice, that means:

- Confirm the company is within the relevant profit band

- Check whether associated companies affect the thresholds

- Apply the marginal relief formula to the taxable profits

- Use the result to reduce the tax that would otherwise arise at the main rate

Marginal relief isn't a judgement call. It's a calculation. If the company sits in that band, guessing the rate is what creates the problem.

The key lesson is less about memorising a formula in isolation and more about recognising that the middle band needs a proper computation. For a founder doing a first return, this is one of the clearest points where software alone can give false confidence if the underlying setup is wrong.

What works in practice

A good calculation process is methodical. Reconcile the accounts, identify tax adjustments, then calculate the liability. A bad process starts with, “What rate do I probably pay?” and works backwards.

That shortcut is exactly why so many small companies get the return wrong in the first place.

Filing Your Return and Paying HMRC on Time

Once the accounts, computations, and CT600 are ready, the final job is procedural. You submit the return online using HMRC's service or approved commercial software, and you pay the corporation tax separately using one of HMRC's accepted payment methods.

Those are two related tasks, but they are not the same task.

Filing and paying are separate actions

This catches new directors every year. They assume that if the return has been filed, the payment side must be taken care of too. It won't be unless you actively arrange it.

A simple way to keep it straight is to treat the process as two checklists:

| Task | What you're doing |

|---|---|

| File the return | Send the CT600, accounts, and computations in the correct digital format |

| Pay HMRC | Transfer the corporation tax due using the right company reference |

If you leave both until the last minute, it's much easier to miss one.

Practical filing habits that help

The businesses that stay on top of this usually do a few simple things well:

- Use software that handles the submission properly: that reduces format issues and keeps a record of what was sent.

- Check the payment reference before sending funds: payments can go astray if the reference is wrong.

- Keep proof of submission and payment together: if there's ever a query, you want both in one place.

Treat tax timing as a cash flow issue

The tax calculation may be annual, but the cash planning shouldn't be. If the company is profitable, start setting money aside before the deadline comes into view. Many directors don't get into trouble because the tax was surprising. They get into trouble because the tax was known but the cash wasn't reserved.

That's why tax compliance and working capital planning belong together. If you want a practical read on that side of the business, cash flow improvement strategies for small businesses are often more relevant to corporation tax than founders first realise.

Common CT600 Mistakes and Costly Penalties

The costliest CT600 mistakes are rarely dramatic. They're ordinary misunderstandings repeated at scale. The most common one is also the easiest to avoid. A company makes no profit, so the director assumes there's no need to file.

That assumption causes a surprising amount of damage.

The nil-profit myth

73% of UK startups incorrectly believe they can skip filing a corporation tax return if they have no profit, yet 31% of penalties issued to new companies in 2025 were for this exact reason, according to Orrick's FAQ on UK company tax return filing.

That's the filing versus payment distinction in its clearest form. No tax due does not automatically mean no return due.

If the company had no profit, the tax bill may be nil. The filing obligation may still be live.

Other errors that keep showing up

Some mistakes come from confusion. Others come from rushing.

- Disallowable expenses included without review: personal or non-deductible costs can distort the tax position.

- Poor supporting records: if the bookkeeping doesn't support the return, corrections take longer and enquiries become harder to answer.

- Deadline mix-ups: directors often remember one date and assume it covers everything.

- DIY adjustments without understanding the accounts: changing figures late in the process can break the link between accounts and computations.

HMRC late filing penalties at a glance 2026

The exact penalty outcome depends on the circumstances and how late the return is, but the practical point is simple: penalties escalate the longer a return remains outstanding.

| Delay | Penalty |

|---|---|

| Late filing | A penalty applies |

| Longer delays | Further penalties can be added |

| Persistent non-compliance | HMRC can increase the cost and scrutiny |

That table is deliberately simple because the important lesson for a new founder is behavioural rather than mathematical. Once a return is late, the position doesn't improve by waiting.

What actually reduces risk

The safest companies don't rely on memory. They keep a tax calendar, close their bookkeeping regularly, and review the company's year-end position before the filing pressure arrives.

The riskiest pattern is waiting for HMRC to tell you something is missing. By that point, you're managing a problem rather than preventing one.

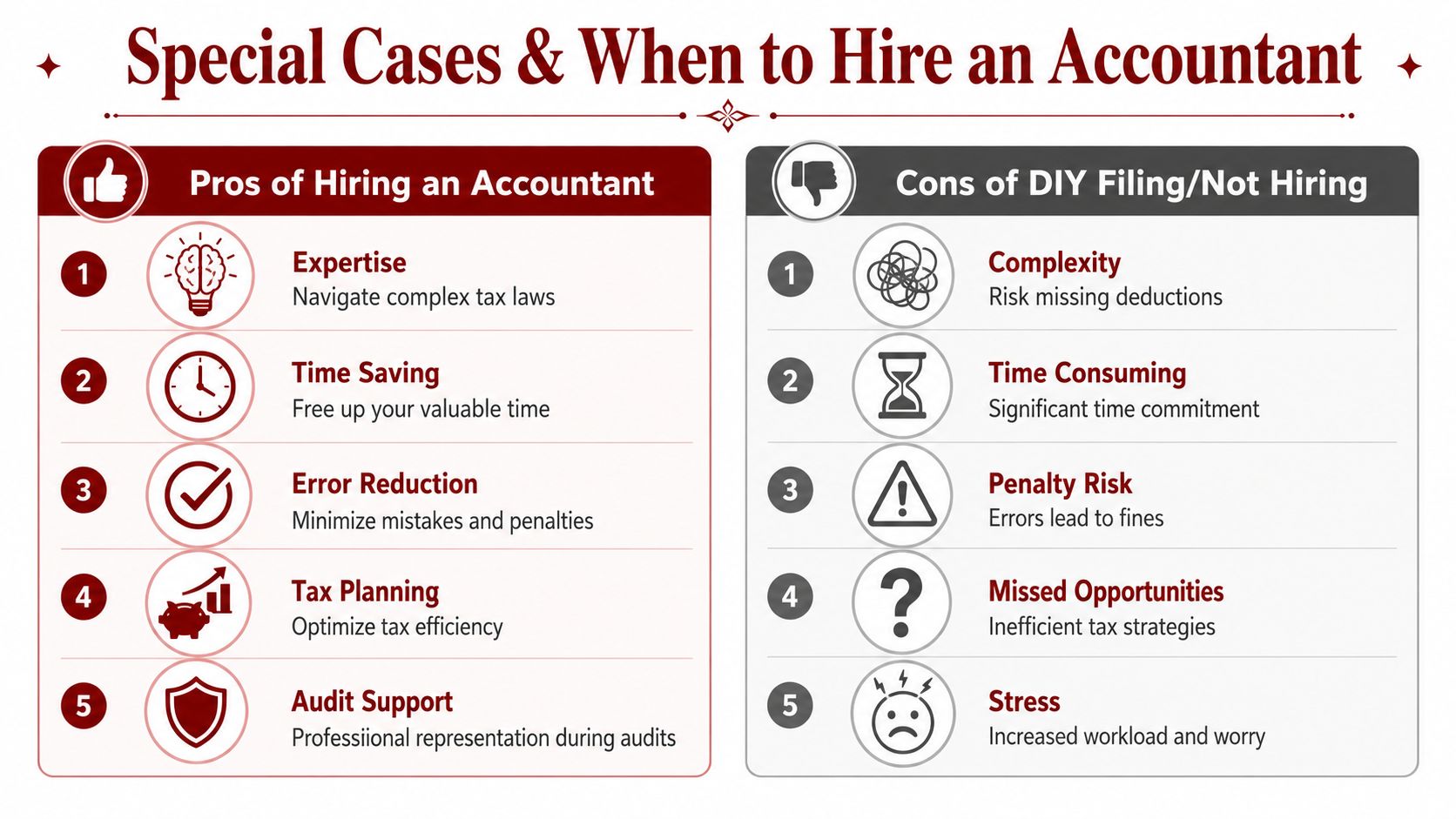

Special Cases and When to Hire an Accountant

Some corporation tax returns are straightforward. Others stop being straightforward very quickly. The line usually gets crossed when the company has sector-specific rules, specialist claims, property complications, or owner transactions that need more than basic bookkeeping.

Construction businesses are a good example. If you're dealing with CIS, subcontractor payments, retention issues, and irregular project timing, the corporation tax return depends on records being right long before year end. The same goes for landlords operating through a limited company. Rental income may look simple on the surface, but finance costs, repairs versus capital expenditure, and property-specific bookkeeping often need closer judgement.

The point where DIY becomes risky

R&D claims are another area where process matters as much as the figures. Companies claiming Research and Development tax relief must submit an Additional Information Form to HMRC before filing their CT600. Failure to do so in the correct order will result in automatic rejection of the return and potential loss of the R&D credit, as explained in HMRC guidance discussed here.

That “before” matters. It's not a paperwork detail. It's a submission condition.

A sensible checklist for getting help

Bring in an accountant when any of the following is true:

- Your profits sit in the marginal relief band: that's where seemingly small mistakes can alter the liability.

- You've mixed personal and company spending: untangling that after the fact is harder than most owners expect.

- You operate in construction or property: sector rules and record-keeping issues tend to multiply.

- You want to claim reliefs, especially R&D: submission order and supporting detail matter.

- You're unsure whether the bookkeeping reflects reality: tax software won't fix bad inputs.

For many founders, the value isn't just form filling. It's judgement, timing, and a second pair of eyes on the parts most likely to go wrong. If you're weighing that up, it helps to understand the broader ways an accountant can support a small business, especially beyond the return itself.

A good accountant doesn't just send the CT600. They help you avoid the avoidable.

If you want clear, practical help with your company's corporation tax return, Action Accountants Limited can support you with year-end accounts, CT600 filing, bookkeeping clean-up, tax planning, and advice specific to growing businesses, contractors, landlords, and founders who'd rather get it right than guess.