VAT Reclaim UK: Maximize Savings in 2026

Action Accountants •15 July 2026

You've paid for fuel, software, tools, materials, subcontract costs, phones, laptops, and office kit. The VAT on those purchases adds up quickly. Then the paperwork lands on your desk, and the core problem emerges. You're not asking whether the business spent the money. You're asking whether HMRC will accept the evidence.

That's where many valid claims go wrong. A business owner keeps a quote instead of the final invoice. A startup stores receipts in three inboxes and two phones. A contractor pays promptly but can't match the payment back to the right supplier document. The cost was real, the VAT was charged, but the reclaim still stalls or fails because the document trail isn't right.

Handled properly, VAT reclaim is a cash-flow tool, not just another compliance job. For a founder watching every outgoing payment, for a small business trying to stay organised, and for a construction firm juggling materials, CIS admin, and supplier paperwork, getting VAT back can make a genuine difference to working capital. If you need a quick refresher to understand Added Value Tax, that's a useful starting point before you deal with reclaim rules in practice.

Many smaller firms also benefit from grounding the basics in plain English before diving into records and claims. This practical guide on VAT for small businesses is helpful if you're still tightening up your setup.

Table of Contents

- Your Guide to Unlocking Cash with VAT Reclaim

- Can You Reclaim VAT? The Essential Eligibility Check

- Choosing Your VAT Reclaim Path

- Your VAT Return Reclaim Process Step by Step

- VAT Reclaim in Action Worked Examples

- Common Pitfalls and When to Get Expert Help

Your Guide to Unlocking Cash with VAT Reclaim

If you're searching for VAT reclaim UK advice, you probably want a straight answer to a simple question. Can the business get that VAT back, and if so, what will HMRC accept?

In practice, VAT reclaim means recovering input VAT on qualifying business purchases. That reclaim usually matters most when spending is front-loaded. Startups buy equipment before revenue settles. Small businesses pay recurring software and supplier bills while margins are still tight. Construction contractors often carry material costs and admin pressure at the same time.

The part that frustrates owners isn't usually the principle. It's the mismatch between commercial reality and tax evidence. You know the expense was genuine. HMRC still wants the right document, in the right form, tied to the right transaction.

Why reclaim work deserves attention

A careful VAT reclaim process does three useful things at once:

- Protects cash flow: Recovering input VAT reduces the amount of money left sitting in cost lines that should be reclaimed.

- Improves bookkeeping quality: Clean purchase records make VAT returns easier and year-end work less painful.

- Reduces avoidable disputes: Good evidence means fewer awkward moments when someone asks for proof months later.

Practical rule: VAT reclaim works best when you treat it as part of purchasing discipline, not as a rescue exercise at quarter end.

Where businesses usually lose money

Losses often come from ordinary admin habits, not complicated tax planning. Someone saves a screenshot instead of the invoice. A supplier sends a pro forma first, and that version gets posted to the accounts system. A director pays on card, but nobody uploads the VAT invoice afterward.

For most businesses, the route is straightforward once the paperwork is under control. The rest of this guide focuses on what works, what doesn't, and how the same rule plays out differently for founders, owner-managed firms, and contractors.

Can You Reclaim VAT? The Essential Eligibility Check

Before looking at receipts and invoices, check the basic gate. For the standard reclaim route, the business must be VAT registered. If it isn't, reclaim through a normal VAT return isn't available.

That sounds obvious, but many owners blur together three separate ideas. Being in business isn't enough. Paying VAT on costs isn't enough. Having a real expense isn't enough. The registration position comes first.

Start with the registration question

If you're VAT registered, reclaim normally sits inside your VAT return. If you operate in construction, there's another layer of care because subcontractor and contractor arrangements can already be complex. If the reverse charge applies in your trade, you need to keep the VAT treatment clear from the outset, and this guide on VAT reverse charge explained is worth reviewing alongside your reclaim process.

Use a business-purpose filter

Once registration is confirmed, test each expense with a practical question. Was it bought for the business, or is there private or blocked use mixed in?

A useful working checklist looks like this:

- Clear business purchases: Stock, office furniture, commercial overheads, and professional fees are usually the easiest category to review because the business purpose is obvious.

- Operational running costs: Fuel, software subscriptions, tools, and supplier services may be reclaimable when they support taxable business activity and the records are complete.

- Mixed-use spending: Mobile phones and similar items need more care where business and personal use are both present.

- High-risk categories: Entertainment, private spending, and certain vehicle-related costs often create problems because owners assume that “partly business” automatically means “fully reclaimable”. It doesn't.

If you wouldn't be comfortable explaining the business purpose of an item to someone outside the company, pause before reclaiming the VAT.

A simple owner test

Ask these questions before posting the purchase:

| Check | What you need to answer |

|---|---|

| Business link | What did the business need this for? |

| User | Who used it, and in what role? |

| Evidence | Do you hold the proper supplier invoice? |

| Private element | Is any part of the cost personal or mixed use? |

For startups, the common trap is early-stage spending made quickly by founders on personal cards, with paperwork saved badly or not at all. For SMEs, the issue is volume. Small errors repeat across dozens of transactions. For contractors, the pressure comes from site activity moving faster than the back office.

Eligibility is rarely the hardest part. Proving it cleanly is.

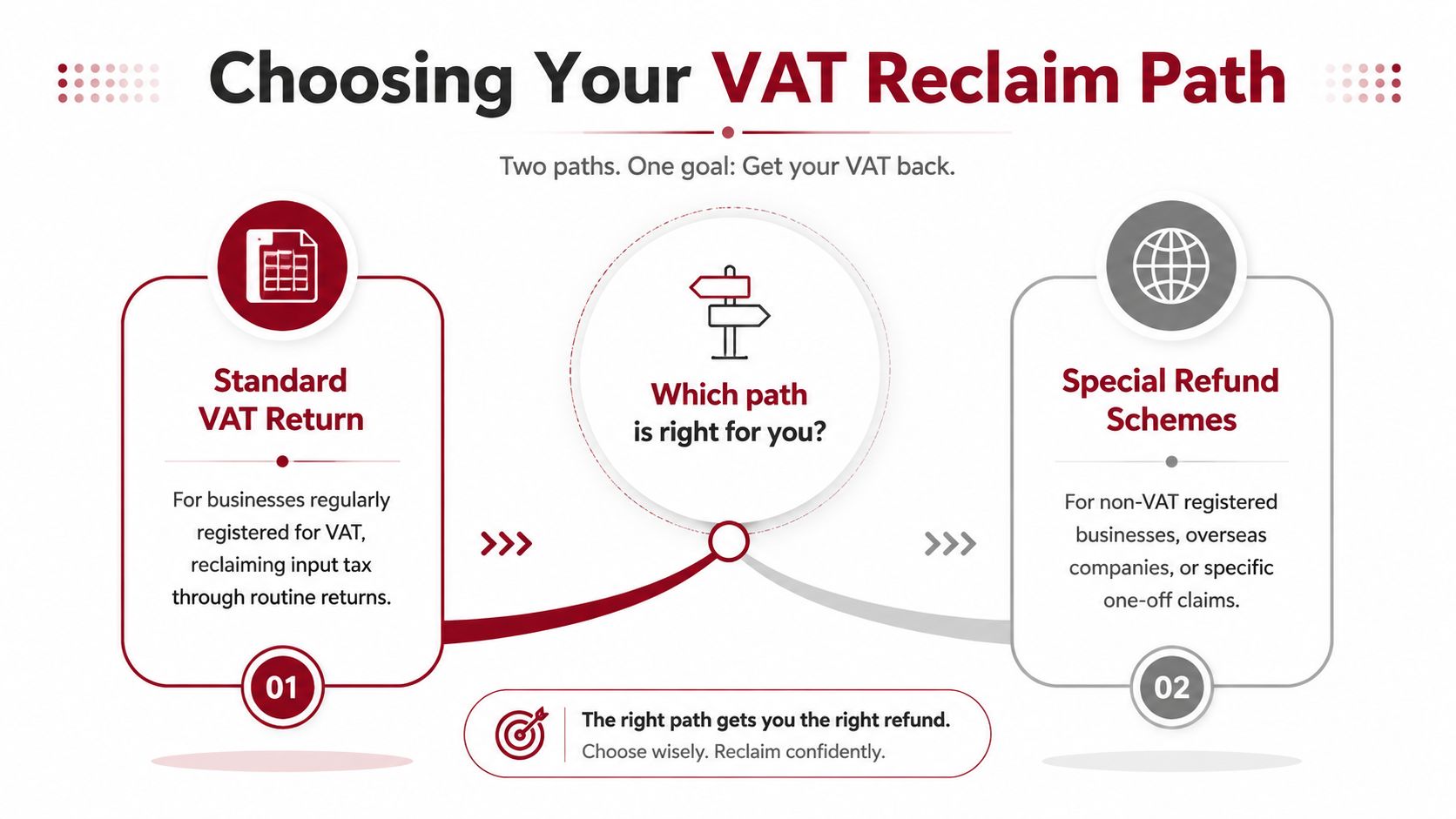

Choosing Your VAT Reclaim Path

Not every VAT reclaim follows the same route. That's where businesses waste time. They read guidance that applies to a different claimant, gather the wrong evidence, or submit to the wrong process.

For most UK businesses, reclaim happens through the regular VAT return. For some others, especially non-UK businesses recovering UK VAT, the claim sits in a separate refund process.

Most UK businesses use the standard return

This is the familiar route for a VAT-registered UK business. You collect VAT on sales, track VAT on purchases, and offset one against the other on the return. If your reclaimable input VAT is higher than output VAT for the period, a repayment may be due.

This route is generally part of routine bookkeeping. That's why method matters more than drama. If purchase coding is wrong all quarter, the final return is only repeating bad records.

Some businesses also choose different VAT accounting approaches for commercial reasons, and scheme choice can affect how day-to-day admin feels even when the reclaim principle stays the same. If you're comparing options, this overview of the VAT Flat Rate Scheme can help frame the trade-offs.

Some claims sit in a separate refund route

The non-UK refund route is much more document-driven. According to HMRC guidance on refunds of UK VAT for non-UK businesses or EU VAT for UK businesses, non-UK businesses claiming UK VAT refunds must submit the VAT65A form electronically with a typed Schedule 9, plus a Certificate of Status (VAT66A Form) that is valid for 12 months from the home country's tax authority. HMRC also requires original VAT invoices showing the VAT amount, and imported goods claims need the VAT copy of the import entry or customs documents. HMRC's benchmark processing timeline is approximately six months.

That's a very different exercise from a domestic VAT return. The wrong schedule format, an expired status certificate, or incomplete import papers can stop an otherwise valid claim.

Overseas refund claims often fail on administration, not entitlement.

VAT reclaim routes compared

| Attribute | Standard VAT Return | VAT Refund Scheme (e.g. VAT65A) |

|---|---|---|

| Typical claimant | UK VAT-registered business | Non-UK business seeking UK VAT refund |

| Where claim sits | Routine VAT return | Separate refund application |

| Core records | Purchase invoices and bookkeeping records | Original VAT invoices, import documents where relevant, status certificate |

| Key formality | Correct VAT posting in the return | VAT65A with typed Schedule 9 |

| Timing feel | Ongoing compliance cycle | Slower, more formal claim route |

| Processing expectation | Linked to normal return handling | HMRC benchmark is approximately six months |

For VAT reclaim UK work, the first decision isn't what expense to claim. It's which lane you're in. Get that right first, and the rest becomes far easier.

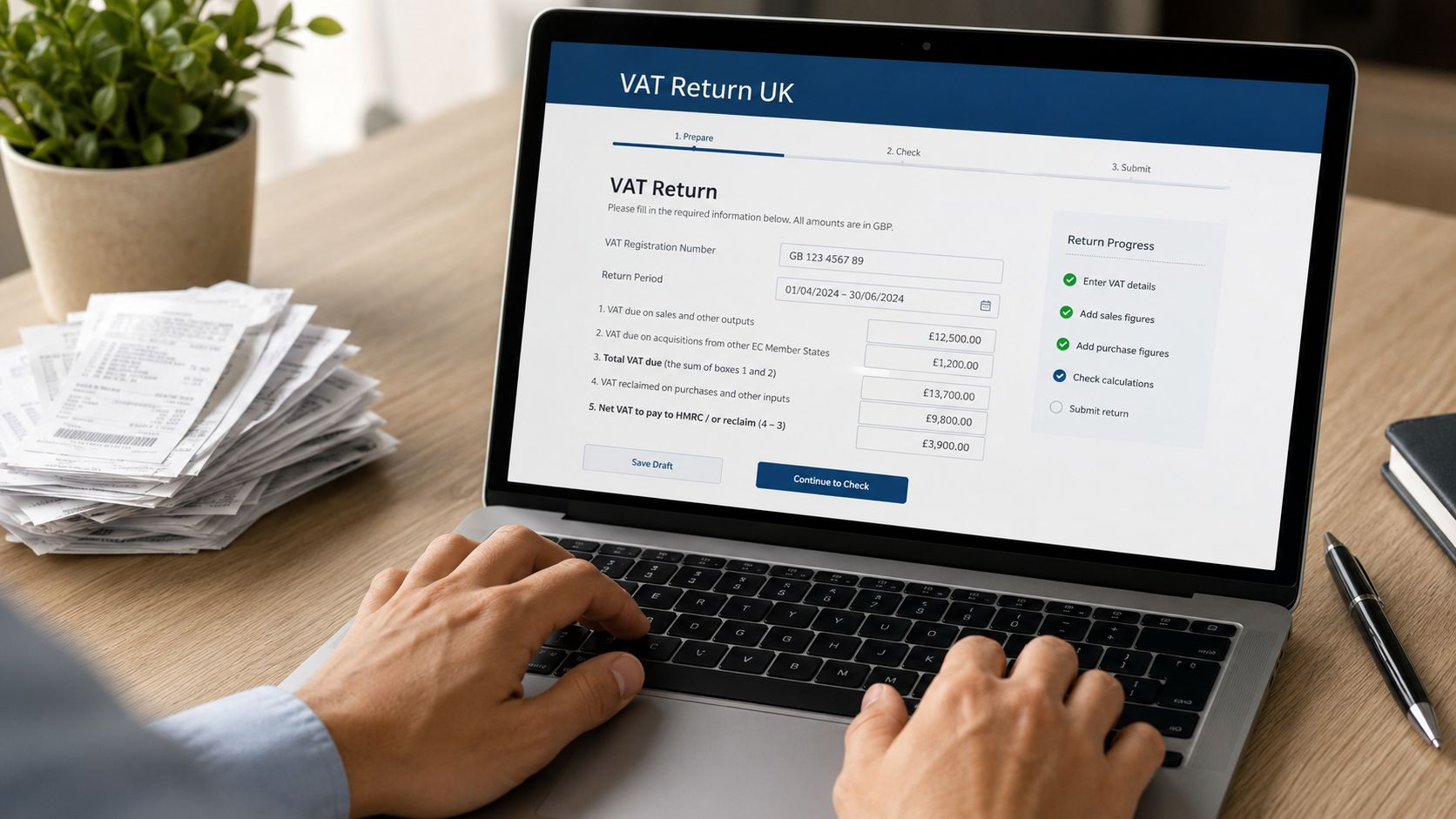

Your VAT Return Reclaim Process Step by Step

For a standard UK VAT-registered business, reclaim starts long before the return is filed. It starts when the purchase happens and someone decides what to keep.

The most reliable process is boring in the best possible way. Buy the item. Get the correct invoice. Match it to the payment. Post it accurately. Keep the record where someone else can find it later.

Start with the invoice, not the bank payment

Many owners begin with the bank feed because that's what they can see quickly in Xero, QuickBooks, Sage, or similar software. That's useful for bookkeeping, but it is not your VAT evidence.

The key rule is set out clearly in Stripe's guide to reclaiming UK VAT. The UK VAT reclaim methodology requires tracking input VAT to populate Box 4 on the digital VAT return. It also states that HMRC rejects pro forma invoices, quotes, and order confirmations for reclaim purposes. HMRC requires a valid VAT invoice showing the supplier's VAT number, the date, and the specific VAT charged. The same guidance notes that records should be kept for at least 6 years, and that claims for past errors are generally allowable up to 4 years prior. For standard registered businesses, a refund arises only when Box 4 exceeds Box 1.

That one paragraph explains a large share of real-world VAT disputes. The spend was genuine, but the file contains the wrong document.

What a disciplined purchase review looks like

When checking purchases, work in this order:

-

Confirm the supplier document

Make sure you have the final VAT invoice, not the quote, estimate, order acknowledgement, delivery note, or pro forma. -

Check the key details

The supplier's VAT number, invoice date, and the VAT charged need to be present. -

Match the commercial story

The invoice should make sense against the business activity. If the description is vague, ask for a clearer version. -

Tie it to payment

Keep proof of payment with the invoice. That could be your bookkeeping entry plus the bank transaction trail.

A clean bank payment without a valid VAT invoice doesn't rescue the claim.

Post the VAT correctly and keep the audit trail

Once the invoice passes review, record the input VAT in your accounting software so it flows into the correct return position. For standard reclaim work, that means feeding the purchase VAT into Box 4.

Founders and small teams often underinvest in process. They rely on memory. They let one person post bills one month and another person do it differently the next. They attach files inconsistently. Then quarter end turns into detective work.

Mixed-use costs need extra discipline. If the item isn't wholly business-related, don't force a full claim. Mobile phones are the classic example. If there's private use, calculate and record the business-use proportion rather than reclaiming the lot.

Submit with digital records that make sense

Digital filing has made speed easier, but it hasn't made weak evidence acceptable. Keep records in one place and name them in a way another person can follow. “Invoice.pdf” is not a filing system. “Supplier name, date, invoice number” is far better.

Businesses preparing for digital compliance should also understand the wider filing framework. This guide to Making Tax Digital for VAT in 2026 compliance is a practical companion if your records still depend too heavily on spreadsheets and inbox searches.

A short walkthrough can also help if you want to see the filing process in action before tightening your own workflow.

A process that survives scrutiny

The strongest reclaim systems have a few habits in common:

- One source of truth: Invoices are stored inside the bookkeeping record or in a single linked document system.

- Fast review: Purchases are checked when they arrive, not months later.

- Clear ownership: Someone is responsible for chasing corrected invoices from suppliers.

- Common sense over optimism: If the record is weak, the claim waits until the evidence is fixed.

The practical difference between a smooth reclaim and a rejected one is often not tax knowledge. It's document discipline.

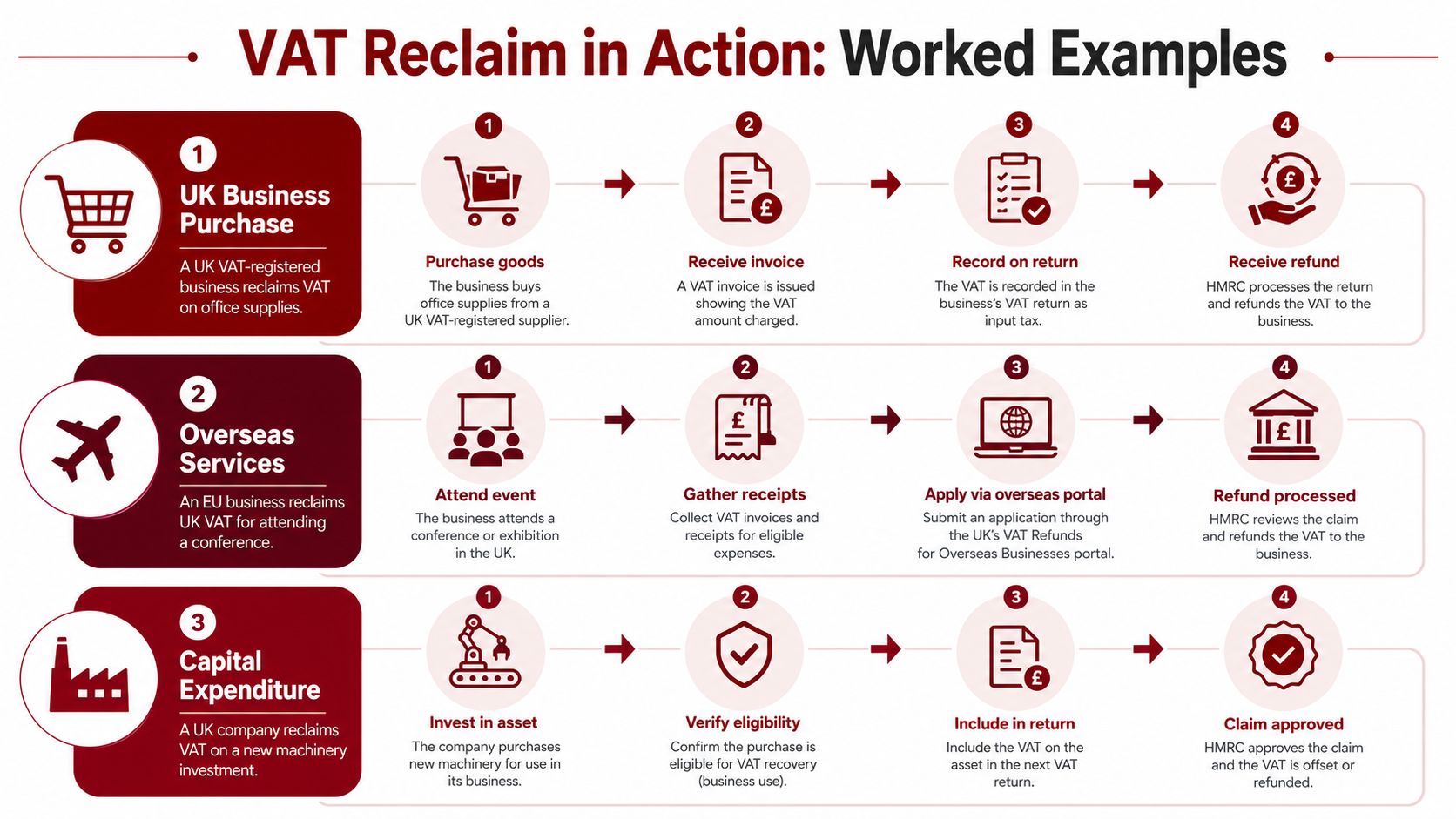

VAT Reclaim in Action Worked Examples

Rules become easier to apply when you can see the paperwork behind them. These three examples reflect the kinds of situations that come up repeatedly in real businesses.

Startup setup costs

A new company buys laptops, desks, and office chairs before trading settles into a normal rhythm. The founder pays some costs directly, suppliers send documents to different email addresses, and the bookkeeper later receives a bundle of forwards with inconsistent attachments.

The reclaim position depends less on excitement about launching and more on whether each purchase has the proper VAT invoice in the company's records. Laptops and office furniture may be valid business purchases, but only the correctly documented items should be included. If one supplier only sent a quote and no proper VAT invoice followed, that line should be chased and corrected before it goes into the reclaim.

A practical startup habit is to create one purchasing inbox from day one and insist that every supplier invoice lands there.

Small business mixed-use phone bill

An owner-managed business pays a monthly mobile phone bill used for both work and personal calls. The mistake here is easy to spot. The business claims all the VAT because the phone is “mainly for work”.

That's not a safe approach when the cost is mixed use. The better method is to identify a reasonable business-use proportion and reclaim only that portion. The same principle applies to similar expenses where personal use exists. The exact method should be sensible, consistent, and documented so it can be explained later if asked.

Where there's mixed use, the strongest answer is rarely “claim all of it and hope”.

Useful evidence might include the billing account, who uses the phone, and a short internal note explaining how the business proportion was reached.

Construction contractor paperwork discipline

Construction businesses often have a different problem. The purchase itself is rarely mysterious. Materials were bought for a site. Plant hire was needed. Subcontractor admin and supplier invoices arrived while the team was focused on delivery.

The pressure point is paperwork flow. A contractor may hold site paperwork, email approvals, delivery notes, and bank payments, but still miss the final VAT invoice in a reclaim file. Materials generally need the same careful invoice review as any other business purchase. If a claim later depends on a quote, statement, or order confirmation, it is exposed.

For contractors, the practical answer is to make document collection part of site controls:

- At order stage: Record which supplier is expected to issue the VAT invoice.

- At receipt stage: Keep delivery evidence, but don't mistake it for VAT evidence.

- At posting stage: Attach the supplier invoice to the bookkeeping entry before the period closes.

- At review stage: Check that site urgency hasn't allowed admin shortcuts into the return.

Construction firms that get this right usually don't have more time than anyone else. They decide that invoice quality is part of cost control.

Common Pitfalls and When to Get Expert Help

A startup founder sends over a tidy folder and says the VAT claim should be straightforward. The spend is real. The business purpose is clear. Then the problem appears. Half the file is made up of pro formas, order confirmations, card receipts, and supplier statements instead of valid VAT invoices. The claim may be commercially genuine, but HMRC looks at the document first.

That is the point many businesses miss. In VAT reclaim work, the wrong paperwork can sink the right claim.

The mistakes that trigger trouble

The first and most common issue is document failure. I see this with startups buying software, small businesses paying suppliers in a hurry, and construction firms trying to piece together site costs after the month end. A quote is not enough. A delivery note is not enough. A bank payment is not enough. If the file does not contain a valid VAT invoice, the reclaim is exposed even where the cost itself was clearly for the business.

The second issue is timing drift. Once records are left for too long, the context disappears. Staff change. Inbox trails go missing. Nobody remembers why a purchase was coded a certain way. HMRC does allow some past errors to be corrected within the relevant time limits mentioned earlier, but late clean-up is always harder because the business has to reconstruct facts it should have recorded at the time.

Then there is mixed-use confusion. This catches owner-managed businesses more than they expect. Mobile phones, broadband, vehicles, home office costs, and subscription services often have a genuine business element, but that does not automatically support a full reclaim. The practical question is not "was this useful to the business?" It is "what part of this VAT can the business support with records and a reasonable method?"

A further problem is weak supplier checks. If an invoice looks inconsistent, carries the wrong details, or comes from a supplier you have only dealt with once, check it before reclaiming. That is why it helps to build a habit around safeguarding your business with VAT checks when onboarding suppliers or reviewing questionable paperwork.

Bad VAT habits waste time twice. First when the claim is submitted badly, then again when someone has to rebuild the file under pressure.

When in-house is fine and when it is not

Keeping VAT reclaim in-house can work well where purchases are routine, invoice collection is controlled, and one person reviews entries consistently before the return is filed. Retailers with stable supplier lists often manage this well. Some service businesses do too, especially where nearly every cost comes through one finance inbox with proper invoices attached.

Expert help tends to pay for itself where the facts are less tidy and judgement matters. Get advice when:

- Records are split across too many places: WhatsApp messages, staff inboxes, paper folders, apps, and accounting software do not form a reliable VAT file by themselves.

- Your sector creates document risk: Construction contractors, trades, and project-led businesses often have proof that work happened, but not the VAT invoice HMRC expects.

- You are dealing with mixed-use costs: These claims need a defensible method, not a rough estimate.

- Supplier paperwork is inconsistent: One wrong invoice format can invalidate a claim that would otherwise have been allowed.

- HMRC has started asking questions: Repeated queries usually point to a weak process, not random bad luck.

- You need to correct older periods: Historic claims are often recoverable, but they need cleaner evidence and more careful review.

A good adviser does more than submit figures. They help you set rules for what your team collects, what accounting staff reject, and what gets reviewed before it ever reaches a VAT return.

If your VAT records are messy, your claims feel uncertain, or you want a second pair of eyes before submitting, Action Accountants Limited can help you sort the paperwork, strengthen your controls, and reclaim VAT with far more confidence.