VAT Flat Rate Scheme: Is It Right for Your Business?

Action Accountants •25 June 2026

You're probably in one of two camps right now.

Either you're staring at a VAT return and wondering why you're wasting hours sorting receipts, checking rates, and trying to remember what you can reclaim. Or you've heard the VAT Flat Rate Scheme is “simpler” and you're asking the sensible question: simpler for who, and at what cost?

That's the right question.

For some small businesses, the VAT Flat Rate Scheme cuts admin and gives you predictable VAT bills. For others, especially startups buying kit and North West London contractors buying materials, it can quietly cost more than standard VAT accounting. The problem is most guides stop at “it saves time” and never show you where it stops making financial sense.

Table of Contents

- VAT Paperwork Overwhelming You There Might Be a Simpler Way

- What Is the VAT Flat Rate Scheme

- Calculating Your Payments Under the Scheme

- The Real Pros and Cons You Must Consider

- A Special Warning for Limited Cost Businesses

- How to Join Leave and Avoid Common Pitfalls

- Is the Flat Rate Scheme Right for You A Partnered Approach

VAT Paperwork Overwhelming You There Might Be a Simpler Way

A lot of business owners hit the same wall after registering for VAT. The sales are coming in, but the bookkeeping suddenly gets heavier. Every fuel receipt, software bill, supplier invoice, and tool purchase becomes another thing to track properly.

For a startup founder, that usually means evenings lost inside Xero or QuickBooks instead of working on sales. For a contractor, it often means a box of paperwork in the van, a pile of WhatsApp invoices, and a last-minute rush before the VAT deadline.

Standard VAT accounting isn't hard because the maths is advanced. It's hard because it's relentless. You have to separate what you charged from what you paid, keep evidence, spot errors early, and stay organised every quarter.

That's exactly why HMRC created the Flat Rate Scheme. It gives smaller businesses a shortcut. Instead of reclaiming input VAT on most purchases and calculating the usual difference, you apply one fixed percentage to your VAT-inclusive turnover and pay that amount.

Practical rule: If VAT admin is draining your time, the Flat Rate Scheme is worth reviewing. If your costs are high, it needs stress-testing before you sign up.

The appeal is obvious:

- Less record chasing: You still need records, but you don't have to build every return around reclaiming VAT on routine purchases.

- Cleaner forecasting: One rate applied to turnover is easier to budget for than a changing reclaim position.

- Fewer moving parts: That matters when you're growing fast or juggling site work, payroll, and supplier issues.

But don't confuse easier with better. Plenty of businesses join because an online guide tells them they can “keep the difference”. Then they realise the difference wasn't profit at all. It was the VAT they gave up reclaiming on materials, equipment, and business spending.

What Is the VAT Flat Rate Scheme

The VAT Flat Rate Scheme is a simplified way for a small VAT-registered business to work out what it pays HMRC. Instead of calculating output VAT minus input VAT on most day-to-day costs, you charge VAT to customers as normal and then pay HMRC a fixed percentage of your VAT-inclusive turnover.

It's comparable to an all-inclusive price instead of itemising every single line. You're trading detailed VAT recovery for a simpler method.

Why HMRC created it

The scheme was introduced in 2002 to reduce the administrative burden on smaller businesses. It's aimed at businesses with expected annual VAT-taxable turnover of £150,000 or less excluding VAT, and you can usually stay in until total income exceeds £230,000. HMRC set it up as a simpler alternative to standard VAT accounting, and it continues to be widely used by small businesses according to HMRC guidance on the Flat Rate Scheme and industry summaries.

If you want a broader primer on how VAT works before you decide on a scheme, this guide to VAT for small businesses is a useful starting point.

How it works in plain English

You still issue invoices with VAT in the normal way. What changes is the calculation on the VAT return.

The scheme works like this:

- You charge VAT as normal on your sales.

- You total your VAT-inclusive turnover for the VAT period.

- You apply your flat rate percentage based on your business sector.

- You pay that amount to HMRC.

There are a few important catches.

- Your sector matters: HMRC assigns different flat rates to different types of business.

- Your turnover must fit the entry rules: This isn't open-ended.

- You usually can't reclaim VAT on purchases: That's the trade-off, except for certain capital assets costing £2,000 or more including VAT.

The scheme is for businesses that want simpler VAT accounting. It is not automatically the cheapest option.

That last point is where many businesses go wrong. On paper, the Flat Rate Scheme looks neat. In practice, whether it helps depends on what you buy, how fast you're growing, and whether HMRC treats you as a limited cost business.

Calculating Your Payments Under the Scheme

This is the part you need to get right. The scheme only works if you calculate it on the correct base and use the right rate.

The basic formula

Under the Flat Rate Scheme, the amount you pay is:

VAT-inclusive turnover × flat rate percentage

That percentage depends on your business sector. According to Stripe's explanation of the UK Flat Rate Scheme, IT consultants use 14.5%, advertising firms use 11%, and businesses in their first year of VAT registration get a 1% discount.

If you're also reviewing what counts as recoverable VAT outside the scheme, this guide on how to claim VAT back helps clarify what businesses often miss.

Example for a London service business

Let's keep this simple.

Say you run an IT consultancy in Kingsbury. Your flat rate is 14.5%. During the quarter, your VAT-inclusive turnover is £24,000.

Your Flat Rate VAT calculation is:

£24,000 × 14.5% = £3,480

If you're still in your first year of VAT registration, the 1% discount applies, so your effective rate would be 13.5% for that period.

Then the calculation becomes:

£24,000 × 13.5% = £3,240

That's the appeal. The method is fast, predictable, and easy to repeat. But it only tells half the story. It doesn't show the VAT you've given up reclaiming on your purchases.

Common sector rates at a glance

Here are some rates that matter to the kind of businesses we see most often:

| Business type | Flat rate |

|---|---|

| IT consultancy and data processing | 14.5% |

| Advertising | 11% |

| Catering services | 12.5% |

| Retailing food and children's clothing | 4% |

| Limited cost traders | 16.5% |

A few points matter more than the table itself:

- Use the correct business category: If your main activity changes, your rate may need to change too.

- Apply it to VAT-inclusive turnover: Using net sales is a common mistake.

- Check your first-year discount carefully: It applies from your date of VAT registration, not from whenever you decided to join later.

If you pick the wrong rate or apply it to the wrong turnover figure, the scheme stops being simple very quickly.

For service businesses with low spending, the maths often looks attractive. For startups buying hardware or contractors buying materials, the flat rate number on its own can be dangerously misleading.

The Real Pros and Cons You Must Consider

The Flat Rate Scheme has real benefits. I'd never tell a small business to ignore it. But I would tell you not to trust the sales pitch version of it.

Where the scheme genuinely helps

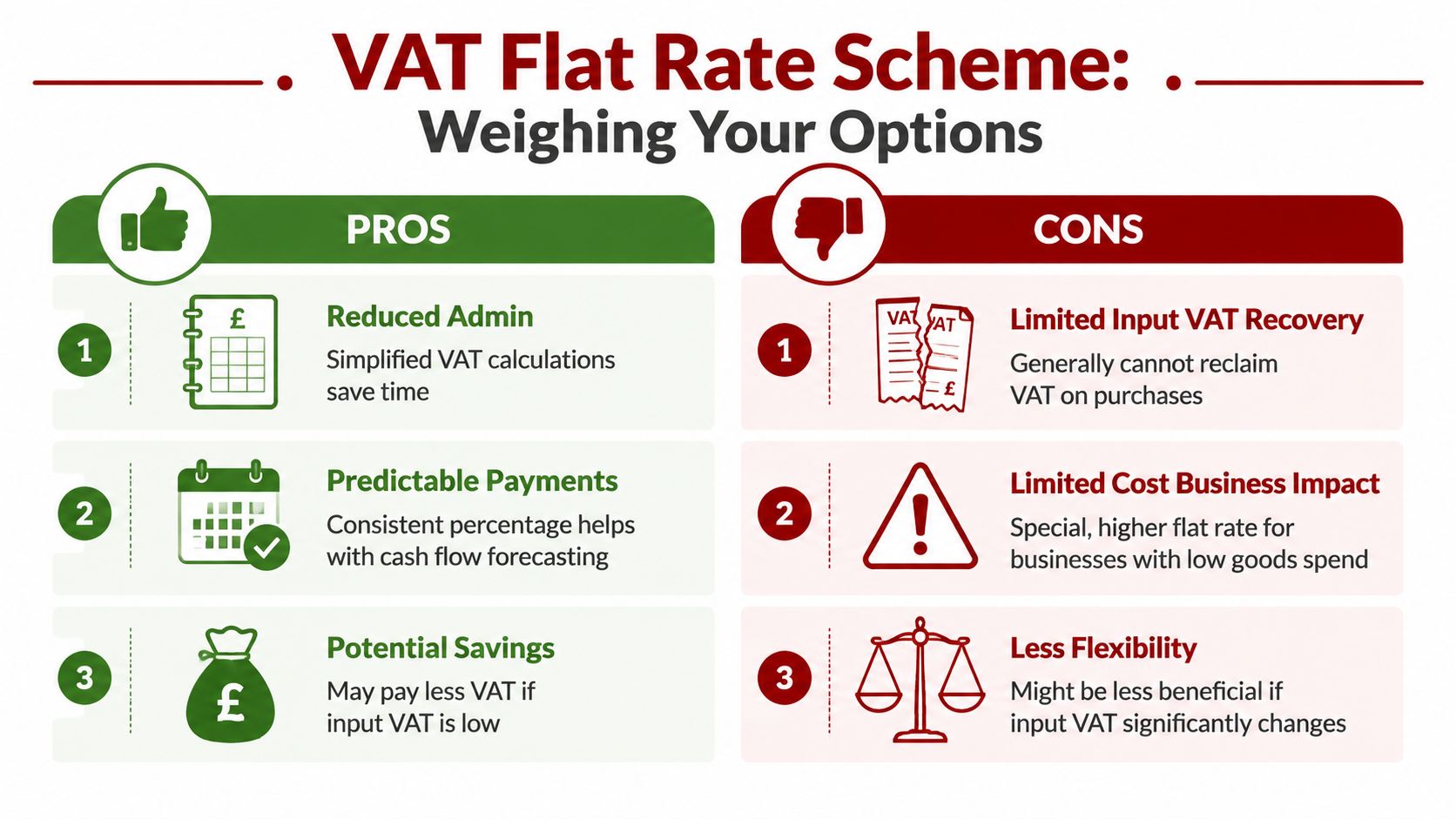

For the right business, the advantages are practical, not theoretical.

- Admin is lighter: You spend less time analysing every routine purchase for reclaim.

- Cash flow is easier to predict: A fixed percentage gives you cleaner forecasting each quarter.

- It can work well when input VAT is low: If you don't buy many VAT-heavy goods, the scheme may leave you better off than standard accounting.

That's why plenty of solo consultants, some early-stage service firms, and owner-managed businesses like it. They don't want VAT to become a weekly admin project.

There's also a psychological benefit. Simpler systems get used properly. Complicated systems get delayed, guessed, or cleaned up in a panic before deadlines.

The hidden cost trap most owners miss

Now the blunt part. The Flat Rate Scheme can cost more than standard VAT accounting. Not occasionally. Not theoretically. Regularly.

The biggest trap is this: once you stop reclaiming VAT on most purchases, the scheme starts punishing businesses that spend heavily on VATable goods. Internal analysis shows that for businesses spending over 20% to 25% of turnover on VAT-eligible goods, the inability to reclaim input VAT can mean losing 15% to 30% more in total compared with standard accounting, especially in sectors like construction. That same analysis is also why many firms need to review VAT reverse charge rules in construction alongside the Flat Rate decision, because the wrong setup can damage cash flow from both sides.

Here's where owners get caught:

- Contractors buying materials: Timber, fixings, parts, site supplies, and other goods can make standard VAT more efficient.

- Startups buying equipment: Laptops, hardware, fit-out items, and launch spending can make the “simple” option more expensive.

- Businesses with changing cost patterns: One quiet quarter doesn't tell you whether the scheme works over a full year.

A lot of generic advice focuses on the difference between what you charge customers and what you pay HMRC. That framing is incomplete. A more accurate comparison is between:

- what you'd pay under the Flat Rate Scheme, and

- what you'd pay under standard VAT after reclaiming eligible input VAT.

That's the comparison that matters.

If your business buys real goods regularly, don't choose the Flat Rate Scheme for convenience until you've tested the annual cost.

The scheme also has a behavioural trap. Owners stay in too long because it feels tidy. They like the easier process, so they ignore the margin erosion. That's a mistake. Simplicity is useful, but it isn't worth paying extra for quarter after quarter if the numbers have moved against you.

A Special Warning for Limited Cost Businesses

This is the rule that commonly impacts various businesses, especially service businesses and labour-heavy contractors.

If HMRC sees you as a limited cost trader, you don't use your normal sector percentage. You use 16.5% instead. That category applies where the cost of goods purchased is less than 2% of turnover or under £1,000 per year, and the rule was introduced in 2017 to tackle perceived abuse of the scheme according to HMRC guidance and official summaries of Flat Rate Scheme rules.

Why many contractors get caught

A North West London contractor can look, at first glance, like the perfect Flat Rate Scheme candidate. Lots of labour income. Straightforward invoicing. Limited back-office support.

Then the limited cost rule bites.

Why? Because not all spending helps you here. Service-heavy costs don't rescue you. Professional fees don't rescue you. Many regular overheads don't rescue you. A business can feel expensive to run and still fail the limited cost test because the wrong type of spending dominates.

That's why labour-only trades, consultants, freelancers, and some subcontractors often get pushed onto the highest rate.

The result is simple. A scheme sold as easier can become the most expensive VAT option available to you.

What to check before you assume the scheme is worth it

Ask these questions before joining or staying in:

- Do you buy enough qualifying goods? If the answer is no, the limited cost rate may apply.

- Is your spend mostly labour and services? That's where trouble starts.

- Are you relying on rough assumptions? You need proper bookkeeping categories, not guesswork.

A quick explainer can help if this rule still feels murky:

Many businesses don't lose money on the Flat Rate Scheme because the maths is hard. They lose money because they never checked whether the limited cost rule applied.

If you're a startup with low goods spend, or a contractor whose work is mainly labour with modest materials, assume nothing. Check the classification first.

How to Join Leave and Avoid Common Pitfalls

The procedure is straightforward. The timing decisions aren't.

Joining and leaving the right way

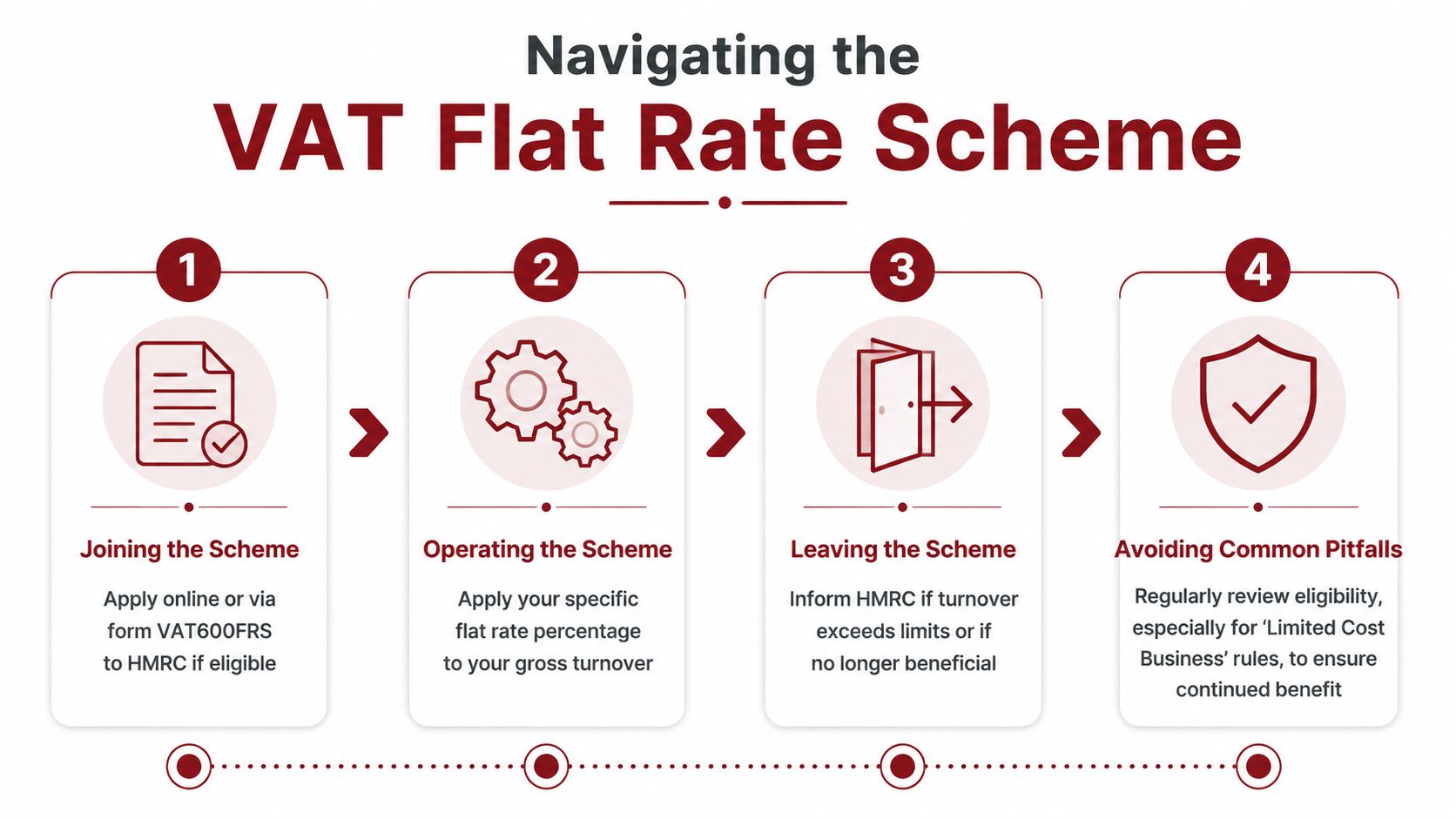

You join the scheme through HMRC, either during VAT registration or afterwards. The application route commonly used is form VAT600FRS or the online process. It can't be backdated.

Once you're in, monitor turnover and eligibility properly. If your business outgrows the scheme or the numbers stop working, don't leave it on autopilot. Review it.

If you're also tightening your VAT systems for digital filing, this guide to Making Tax Digital for VAT compliance is worth reading alongside your scheme decision.

The timing mistake that hurts cash flow

Here's the risk most guides barely mention. Once you leave the scheme, there's a 12-month wait to rejoin according to internal analysis of the rule and its practical impact.

That matters more than people think.

Say you leave because standard VAT looks better today. Then a later period swings the other way. Maybe your costs drop. Maybe projects change. Maybe your purchasing pattern moves. You can't hop back in next quarter because it suits you.

That's why timing matters:

- Leaving just before a high-spend period can help

- Leaving just before a low-spend period can backfire

- Exiting without forecasting upcoming work is careless

Owners often make the decision based on the last quarter alone. That's too narrow. Construction and startup spending can be lumpy. One quarter may include equipment purchases, fit-out costs, or materials. Another may be mostly labour and sales.

Watch this closely: The best time to review whether to exit is before a major change in purchasing pattern, not after the VAT return lands.

You also need to keep an eye on turnover changes. Once a business grows quickly, the admin simplicity can disappear at exactly the point when the business needs tighter controls anyway. If your income is volatile, review the scheme proactively rather than waiting for HMRC to force the change.

Is the Flat Rate Scheme Right for You A Partnered Approach

Here's my view. The VAT Flat Rate Scheme is good for a narrow group of businesses and a poor fit for many others.

If you run a lean service business with low goods spend, stable turnover, and a clear sector rate, it may suit you well. If you're a startup buying equipment, or a contractor whose material spend changes from job to job, don't join just because it sounds easier. Run the numbers first.

The decision usually comes down to three things:

- What you spend money on

- Whether the limited cost rule applies

- How your turnover and purchasing pattern will change over the year

Most bad VAT decisions aren't caused by bad intentions. They happen because the business owner made a quick choice based on a simplified online article or copied what a friend in another trade was doing.

You need a proper comparison, not a guess.

If you want a clear answer for your business, speak to Action Accountants Limited. We help startups and contractors in Colindale, Kingsbury, Queensbury, Edgware, Finchley, and across North West London work out whether the Flat Rate Scheme saves money or damages margins. We'll look at your sector, your spending pattern, your growth plans, and your VAT setup, then give you a straight recommendation you can act on.