How to Register for CIS: A UK Guide for 2026

Action Accountants •6 July 2026

You've probably had the same call many people in construction get at short notice. A contractor offers you work, then adds one line that stops the conversation cold: “You'll need to be on CIS before we can pay you.”

That's usually the moment the confusion starts. People mix up CIS with Self Assessment, assume they can sort it after the first invoice, or register under the wrong role because nobody explained the difference between being paid under CIS and operating CIS for others. Those mistakes don't just create admin. They affect cash flow, payment timing, and how much tax gets held back.

If you want a practical answer to how to register for CIS, the key is to get the setup right before the first payment is due. The paperwork itself isn't usually the hard part. The hard part is knowing which route applies to your business, what HMRC expects to see, and where the usual snags appear.

Table of Contents

- The CIS Crossroads Contractor Subcontractor or Both

- Gathering Your Toolkit Before You Register

- Your Step-by-Step HMRC Registration Process

- Beyond Registration Verifying Subs and Managing Deductions

- Unlocking Cash Flow How to Get Gross Payment Status

- When to Call Your Accountant for CIS Support

The CIS Crossroads Contractor Subcontractor or Both

A builder takes on work from a main contractor all year, then wins a bigger job and brings in a bricklayer, electrician, and roofer to help finish it. Nothing about the business name changes, but the CIS position does. That is the point where registration errors start costing time and cash.

Start with the role you play

CIS follows what your business does in practice.

If another business pays you for construction work, you are usually acting as a subcontractor. If you hire and pay other trades for construction work, you are usually acting as a contractor. If both happen in the same business, you may need to deal with CIS from both sides at once.

That split matters because the admin and the cash flow consequences are different. A subcontractor needs the registration set up properly so deductions are handled correctly and, where relevant, gross payment status can be considered. A contractor has reporting and deduction duties from the moment subcontractors are brought in. Miss the role, and the problem usually shows up later as payment delays, incorrect deductions, or a scramble to fix HMRC records after work has already started.

A quick way to sort the position is to look at the payment chain.

| Situation | Likely CIS role |

|---|---|

| You invoice a main contractor for labour or construction work | Subcontractor |

| You pay another trade to complete part of a job | Contractor |

| You do both through the same business | Both |

I tell clients to write down two lists before they register. Who pays you. Who you pay. In many cases, that answers the question faster than reading pages of guidance.

Set it up for the work you are actually doing

New businesses often assume CIS status is fixed, but it changes with the jobs you take on. A sole trader can start as a subcontractor only, then become a contractor as soon as they begin paying other trades. A limited company can do exactly the same.

The common mistakes are predictable.

One is assuming small firms do not count as contractors. Size is not the test. Paying subcontractors for construction work is what brings the contractor side into play.

Another is assuming company formation, PAYE setup, or VAT registration has already covered CIS. It has not. Those registrations sit alongside CIS, not inside it.

A third problem comes from businesses that do not see themselves as construction businesses at all. Property developers, landlords with larger projects, and firms that regularly commission building work can still trigger contractor obligations. That point catches people out because the work feels incidental to them, while HMRC looks at the substance of the spend.

From an accountant's side, this is the first decision worth getting right because it affects everything that follows. Registration route, deduction handling, monthly compliance, and whether cash gets held back under CIS all depend on your role. If the business is growing and the subcontractor list is getting longer, the wider setup matters as much as the registration itself. This guide to accounting for contractors in construction gives a clearer view of how CIS fits into the day-to-day running of the business.

Gathering Your Toolkit Before You Register

Trying to register without the right details is where a simple job turns into a week of delay. HMRC's systems are straightforward when your information matches. They're much less forgiving when names, addresses, tax references, or business details don't line up.

What to have ready

Before you start, get everything into one place.

A clean registration pack usually includes:

- Legal business name: Use the exact trading identity HMRC will recognise. If you trade under a different name, keep the legal name clear.

- Current address: Tax references and confirmation letters are tied to this address.

- National Insurance number: HMRC uses it to match you to the correct individual tax record.

- UTR: This is the key identifier for Self Assessment and CIS.

- VAT number if applicable: If your business is VAT-registered, missing this can create mismatch issues.

- Business type: Sole trader, partnership, or limited company changes the route and the records HMRC expects.

- Contact details: Use an email and phone number you monitor.

- Bank details for your own records: You may need them alongside the wider setup, even if they're not the main sticking point in registration.

- Government Gateway access: If you've lost the login, sort that before you sit down to register.

The critical point is the UTR. Without it, many people freeze halfway through the process or start trying to register under the wrong service.

The UTR bottleneck that delays registration

One of the most common practical problems is timing. If you're new to self-employment, you may need to register for Self Assessment first so HMRC can issue your UTR. According to Cavendish Professionals' CIS and UTR guide, HMRC typically sends the UTR by post within 10 working days. That's why subcontractors are advised to register at least 2–3 weeks before their first expected CIS payment, so they don't end up under the 30% deduction rate instead of the verified 20% rate.

That waiting period is where people get caught. They start work straight away, assume the tax side can be tidied up later, and then discover the contractor can only process them at the higher deduction rate until the status is sorted.

Get the tax identifiers in place before the first invoice goes near the payment run. It's much easier to start clean than to unwind avoidable deductions afterwards.

If you're asking how to register for CIS because a job has just landed, don't leave the admin until the end of the week. In practice, the setup works best when you treat it like site prep. Get the groundwork in first, then start the job.

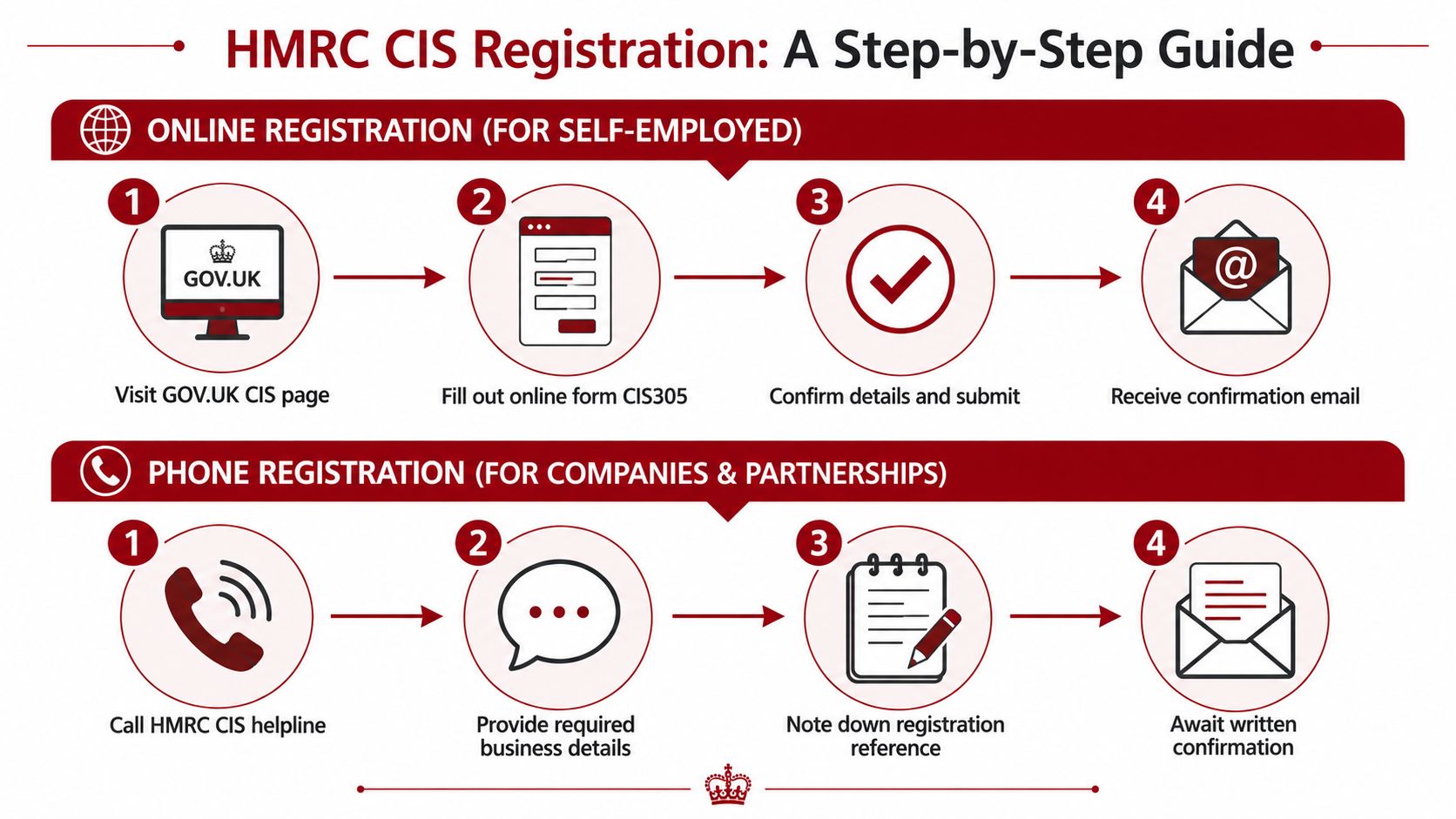

Your Step-by-Step HMRC Registration Process

A lot of CIS registration problems start the same way. The job is ready, the invoice is drafted, and then someone realises HMRC setup is still incomplete. That is when payments get delayed, deduction rates go wrong, and cash flow takes an avoidable hit.

###

The right registration route depends on what you are doing in the chain. Some businesses only need to register as subcontractors. Others need contractor registration because they are paying subs. Quite a few growing firms end up needing both, and that is where I often see people register for one side and assume the other is covered.

If you are registering as a subcontractor

For a sole trader or partner who wants to be paid under CIS, the cleanest route is usually the online HMRC process. HMRC's guidance on registering as a CIS subcontractor explains that if you register for Self Assessment and choose the option showing you are working as a subcontractor, HMRC can set up both at the same time.

That matters because the registration choice affects how quickly a contractor can process you and what deduction treatment applies from the start. If you want a practical walkthrough of the tax setup behind that, our guide to CIS for self-employed subcontractors covers the common points people miss.

Use this sequence:

- Sign in to Government Gateway. Create access first if you do not already have it.

- Start the Self Assessment registration. Read each option carefully rather than clicking through on autopilot.

- Choose the subcontractor option. That is the point that connects your tax registration to CIS.

- Enter your details exactly as HMRC is likely to hold them. Name variations, old addresses, and inconsistent trading details often slow things down.

- Submit the application and save the confirmation. Keep screenshots or emails in one place.

- Wait for HMRC to issue or confirm your UTR if needed.

- Pass the correct details to the contractor so they can verify you before payment.

The trade-off is straightforward. Online registration is faster if your records line up. If your identity details are inconsistent, you save more time by fixing that first than by rushing an application that later needs untangling.

Here's a short explainer if you prefer to see the process discussed before doing it yourself:

If you are registering as a contractor

Contractor registration is operational, not just administrative. You are not setting up how tax is taken from your own payments. You are setting up how your business verifies subcontractors, applies deductions, issues statements, and reports to HMRC each month.

If you are about to pay your first subcontractor, register before that first payment run. Leaving CIS until invoices are already on the desk is how businesses end up making payments they then have to correct.

In practice, contractor setup usually means:

- Registering the business for CIS with HMRC

- Deciding who owns subcontractor verification

- Setting up a process for deduction statements

- Making sure monthly returns are diarised and not left to memory

Internal control matters. In a small business, that may be one director and one bookkeeper. In a limited company with several people handling payroll, purchasing, and accounts, CIS slips through the cracks unless one person clearly owns it.

How to know it has been done properly

Good CIS registration feels uneventful. Your payer can verify the details, the right deduction status is applied, and nobody is chasing HMRC while payments are on hold.

Run this check straight after registration:

| Check | What good looks like |

|---|---|

| Registration status | You know whether you are set up as a subcontractor, contractor, or both |

| UTR | It is recorded correctly and ready to give to the payer if needed |

| HMRC access | You can get into Government Gateway without a reset |

| Payment setup | The contractor has the details needed to verify you |

| Records | Confirmation emails, screenshots, and reference numbers are saved |

CIS registration is only finished when the next payment can go through correctly, first time.

That is the practical test.

Beyond Registration Verifying Subs and Managing Deductions

Registration gets you through the HMRC door. Day-to-day CIS compliance starts when the first subcontractor invoice lands and someone in the business has to decide whether to pay it in full, deduct 20%, or stop and verify first.

That decision affects tax, cash flow, and rework.

Verification comes before payment

Every new subcontractor should be verified with HMRC before the first payment run. The point is simple. You need HMRC's confirmation of the deduction rate before money leaves the bank, not after.

Contractors usually see one of three outcomes:

| Verification outcome | What it means for payment |

|---|---|

| Gross payment status | You pay the subcontractor in full, with no CIS deduction |

| Standard verified status | You deduct 20% from payments |

| Unverified or not registered | You deduct 30% from payments |

The avoidable mistake is relying on what the subcontractor says, or on the fact they worked for another contractor last month. Your business still needs its own verification record. If HMRC later challenges the deduction treatment, “they told us they were on CIS” does not solve the problem.

Verify first. Pay second. That order saves a lot of cleanup.

If you're on the subcontractor side and want to understand why contractors ask for certain details, this guide to CIS for self-employed subcontractors explains what they are checking and why it matters.

Managing deductions properly each month

Once a subcontractor is set up correctly, the work becomes routine. Routine work is where small errors creep in. A missed verification, the wrong deduction rate, or a late statement can turn one invoice into a month of corrections.

A contractor process that holds up under pressure usually includes:

- Pre-payment verification: Check every new subcontractor before the first payment.

- Accurate deduction handling: Apply gross, 20%, or 30% exactly as HMRC confirms.

- Clear payment split: Record labour and CIS deductions clearly so the figures can be supported later.

- Deduction statements: Issue them promptly so subcontractors can reconcile their own records.

- Monthly return control: File the CIS300 on time, including nil returns where required.

I see the same pressure point repeatedly. The business gets busy, invoices are approved quickly, and CIS is treated like a back-office tidy-up for later. That usually ends with someone rebuilding payment records from bank entries and supplier folders, which is slow, expensive, and far less reliable than doing it properly at the point of payment.

Good CIS control is really a finance process. Someone needs to own the checks, someone needs to review exceptions, and the filing date needs to sit in the same calendar discipline as payroll and VAT.

The contractors who stay out of trouble are rarely doing anything clever. They verify before paying, keep clean records, issue the paperwork on time, and treat CIS as a monthly compliance job rather than an admin task to catch up on at year-end.

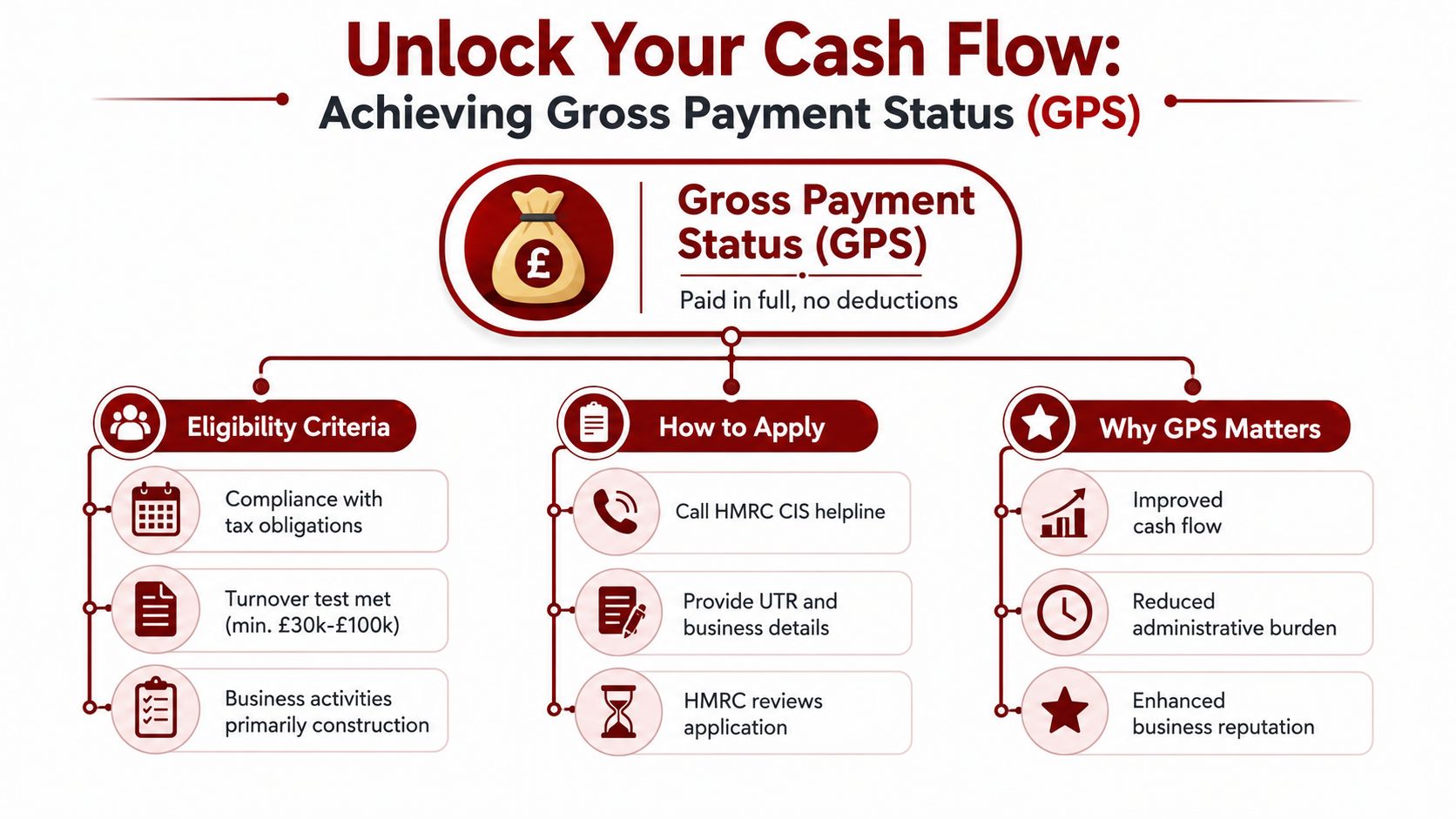

Unlocking Cash Flow How to Get Gross Payment Status

For subcontractors, gross payment status is usually the point where CIS stops feeling like something that happens to you and starts working with your business instead of against it.

Why gross payment status matters

Under standard CIS treatment, contractors deduct tax from your payments before the money reaches you. That may be manageable for some businesses. For others, it tightens working capital at exactly the wrong point. Labour has to be covered, materials still need buying, and fuel, insurance, and overheads don't wait.

Gross payment status changes that by allowing you to be paid in full without CIS deductions. It's one of the biggest cash flow improvements available inside the scheme, which is why it deserves more thought than a quick tick-box application.

If your business is growing and cash is always tight between payment dates, it's worth understanding how stronger payment timing affects the wider business. This guide on improving cash flow fits well alongside CIS planning.

The three tests that decide the outcome

Gross payment status is hard to get because HMRC applies a strict eligibility test. The version referenced in Audit Consulting Group's CIS registration page highlights three parts:

- Business test: You need to show genuine construction business activity, described there as 200+ days of construction work in the past year.

- Turnover test: The same source refers to a minimum annual turnover threshold, including £30,000 for sole traders and £100,000 for companies.

- Compliance test: Your filing and tax history need to be clean, with no relevant tax violations in the past year.

The headline figures in that source are a useful reality check. It states that only 12% of UK subcontractors who applied for gross payment status in 2024 were approved, with 78% of failures due to insufficient turnover and 14% due to incomplete business records.

Those numbers tell you two things. First, gross status matters enough that many people apply. Second, most applications fail because the evidence isn't there.

Gross payment status rewards preparation, not optimism.

A practical pre-application check

Before you apply, test your position accurately.

Ask yourself:

- Turnover evidence: Can you prove the required level from proper records, not rough estimates?

- Business activity: Does your paperwork show real construction trading over the period HMRC will consider?

- Tax compliance: Are your returns up to date and your tax affairs tidy?

- Business records: If HMRC asks follow-up questions, can you answer them with documents rather than explanations?

What works is building the application from records already in order. What doesn't work is applying first and planning to sort the records out if HMRC asks. By then, you're on the back foot.

If you don't meet the tests yet, that isn't a dead end. It usually means you need a stronger bookkeeping trail, better filing discipline, or more time trading before the application stands up properly. In many cases, waiting until the evidence is solid is better than submitting a weak application and hoping it slides through.

When to Call Your Accountant for CIS Support

A lot of CIS problems start the same way. Work picks up, a second subcontractor comes on site, invoices are flying out, and the tax admin gets pushed to Friday afternoon. That is usually the point where small mistakes stop being small.

The question is not whether you can fill in a form yourself. The key question is whether your setup will still hold together once deductions, monthly returns, payment verification, payroll, and year-end accounts start crossing over.

An accountant earns their keep at the trigger points where CIS affects cash flow or creates cleanup work that costs more than early advice.

The points where outside help usually pays for itself

You should get advice if any of these apply:

- You act as both contractor and subcontractor: Records get muddled. Money deducted from your own income is one issue. Deductions you make from others and report to HMRC are a separate one.

- You have taken on your first subcontractor: Registration is only the start. Verification, deduction rates, payment statements, and monthly returns all need to line up from month one.

- You want gross payment status: A weak application wastes time and can leave cash tied up through deductions you might have avoided with better preparation.

- You have missed CIS returns or cannot match deductions to payments: Once several months are wrong, the repair job usually involves rebuilding records from bank entries, invoices, and contractor statements.

- You moved from sole trader to limited company: CIS does not automatically follow the trade into the new structure. The company needs its own setup checked properly.

- A contractor is deducting at a higher rate than expected: That often points to a failed verification, mismatched details, or a registration problem that needs fixing before more payments go through.

The main value of good advice is not form filling. It is getting the whole chain right. Registration, bookkeeping, payroll, VAT, subcontractor checks, and tax repayments all affect each other. If one part is wrong, the problem often shows up somewhere else first, usually in cash flow.

I see this a lot with growing firms in London. They come in asking one narrow question about CIS, but the main issue is that the finance process has not kept pace with the business. A specialist contractor accountant in London can review the setup as a whole and fix the weak points before HMRC, or your bank balance, exposes them for you.

What to say when you ask for help

You do not need to diagnose the problem perfectly before speaking to an accountant.

Plain wording is enough:

“I've started construction work and need to register correctly for CIS. I'm not sure if I'm a subcontractor, a contractor, or both.”

Or:

“I'm already trading, but I need someone to check whether my CIS deductions, returns, and registration are actually right.”

That gives an accountant enough to spot the risk areas quickly.

If you want clear help with CIS registration, contractor setup, monthly compliance, or a gross payment status review, Action Accountants Limited supports construction businesses with practical, hands-on advice. The team works with contractors, subcontractors, startups, and growing firms that need clean systems, reliable filings, and straightforward guidance that protects cash flow as well as compliance.