How to Reduce Corporation Tax: A UK Guide for 2026

Action Accountants •13 July 2026

You finish your year, the sales look healthy, cash has been tight enough to keep you cautious, then the corporation tax figure lands and feels out of proportion to how the business feels on the ground. That's a common North West London problem, especially for owner-managed companies that are profitable on paper but still juggling payroll, supplier costs, and uneven cash flow.

The mistake is thinking the tax bill starts when the return is prepared. In practice, the tax bill is shaped all year. The businesses that reduce corporation tax legally are usually not doing anything exotic. They're claiming the right costs, timing key decisions properly, and avoiding the quiet traps that sit between “small company” tax treatment and the higher rate bands. For contractors and subcontractors, the CIS side adds another layer that standard guides often gloss over.

Table of Contents

- Beyond the Basics of Corporation Tax

- Mastering Your Allowable Business Expenses

- Strategic Timing and Accounting Choices

- Leveraging Capital Allowances and R&D Credits

- The Salary vs Dividend Marginal Relief Calculus

- Advanced Strategies and Construction Industry Rules

- Your Corporation Tax Reduction Checklist and Next Steps

Beyond the Basics of Corporation Tax

A lot of business owners still think about corporation tax as a fixed cost. It isn't. It's a liability shaped by decisions you make before the year end, not just after it. If your accountant only speaks to you once the books are closed, most of the useful planning has already passed.

That matters even more because the UK rules haven't stood still. The corporation tax rate fell from 30% in 2007 to 19% by 2017, and although the main rate increased to 25% in 2023 for larger companies, the 19% rate remained for smaller firms, creating the dual-rate system businesses now have to operate within, as discussed by the IPPR analysis on UK corporation tax policy. What worked when there was a simpler headline rate doesn't always work now.

Why the current rules need active planning

The practical issue isn't just the rate itself. It's the thresholds, the interaction with profits, and the way director decisions feed into taxable results. A founder in Colindale, Finchley, or Edgware can have a perfectly ordinary year and still drift into a less efficient position by delaying pension contributions, under-claiming expenses, or leaving salary strategy on autopilot.

Good tax planning usually looks boring from the outside. It's often just better timing, cleaner records, and fewer assumptions.

The same is true in project-led industries. Businesses that control information well tend to make better tax decisions because they spot commitments, invoices, and deadlines earlier. That's one reason process discipline matters. If your work involves complex deliverables or consultant coordination, the thinking in this piece on managing information in architectural projects is useful well beyond architecture.

The tax return is the end of the process

By the time you file your corporation tax return, the planning window is mostly closed. You can still correct errors, improve disclosure, and make sure reliefs are properly claimed, but you usually can't go back and redesign the year.

That's the mindset shift behind how to reduce corporation tax properly. You don't start with the form. You start with profit, timing, structure, and evidence.

Mastering Your Allowable Business Expenses

The fastest legitimate way to reduce taxable profit is still the oldest one. Claim every expense the business is entitled to claim, and make sure the records support it.

Most overpayments don't come from dramatic mistakes. They come from small omissions repeated all year. A subscription not coded correctly. Mileage never logged. Training paid personally and never reimbursed. Use of home ignored because the claim feels minor. Those items add up, and they reduce profit directly when they're handled properly.

The rule that matters most

For most expenses, the test is whether they were incurred wholly and exclusively for the business. That sounds simple until real life gets involved.

A staff event can be allowable. Client entertaining usually isn't. Travel to a temporary work location may be allowable. Ordinary commuting generally isn't. Software used for business is usually straightforward. Mixed personal and business use needs care and evidence.

Practical rule: if you'd struggle to explain the business purpose clearly from the invoice alone, add a note when you record it.

That habit matters more than people think. When records are weak, businesses often stop short of claiming costs they could have claimed confidently.

Expenses owners often miss

Here's where I regularly see gaps with SMEs and startups:

- Home working costs: If you run part of the business from home, don't ignore the business element of household running costs where a claim is appropriate and supported.

- Training and subscriptions: Professional development, industry courses, and trade subscriptions can be missed because they feel personal. If they're for the existing business activity, they may be relevant.

- Business travel: Rail, parking, hotel stays, and mileage often sit in personal bank accounts or card statements instead of the bookkeeping.

- Software and small recurring tools: Xero add-ons, design platforms, trade apps, cloud storage, quoting tools, and CRM subscriptions are easy to overlook because each individual payment looks small.

- Director reimbursements: If you paid a legitimate business cost personally, the company shouldn't lose the deduction just because the receipt didn't pass through the company card first.

A clean expense process helps more than any year-end scramble. If you need a practical system for capturing costs consistently, Senki's guide for small businesses is a useful reference for building better habits.

What to separate clearly

Some expenses cause confusion because they feel commercially sensible but aren't treated the same way for tax.

| Cost type | Typical tax treatment |

|---|---|

| Staff welfare or staff events | Often allowable if structured properly |

| Client entertaining | Commonly disallowed |

| Business software | Usually allowable |

| Personal purchases through the company | Usually not allowable |

| Travel for business duties | Can be allowable with records |

| Everyday commuting | Commonly restricted |

The bookkeeping detail matters here. If you post everything into a generic “expenses” code, you make review harder and increase the chance of either missing relief or claiming something weakly.

For growing firms, that's where finance discipline becomes part of profitability, not just compliance. Better categorisation, approval, and evidence usually lead to better tax outcomes, and the wider commercial side of that is covered well in this piece on spend smart and grow fast.

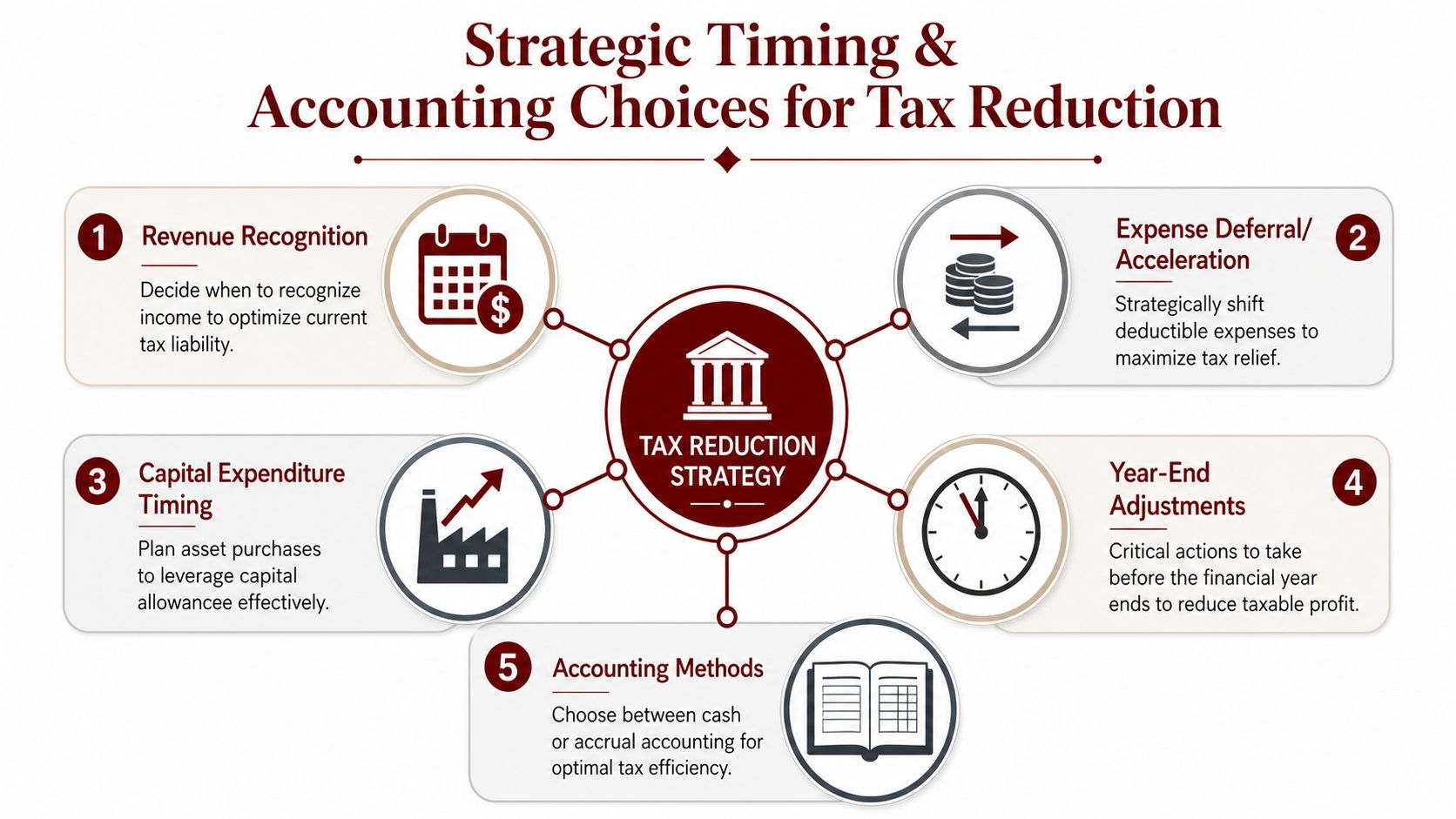

Strategic Timing and Accounting Choices

Timing changes tax. Not in a gimmicky sense. In a direct mathematical sense.

For the financial year beginning 1 April 2026, the main corporation tax rate is 25% for profits over £250,000, while 19% applies to profits under £50,000, and companies between those thresholds fall into the marginal relief range, according to PwC's summary of UK corporate income tax rules. That means the date you incur a cost, make a pension contribution, or complete a purchase can affect which part of the regime you land in.

Timing beats hindsight

A lot of owners focus on whether something is deductible. The sharper question is often when the deduction lands.

If your projected profit is close to a threshold, timing decisions become especially valuable. Bringing forward a legitimate business expense before the year end can produce a very different outcome from paying the same cost shortly after. The same logic applies to employer pension contributions and some asset purchases.

Five decisions that often move the number

-

Revenue cut-off

If work spans the year end, make sure income is recognised correctly. Don't pull income forward casually just because cash arrived, and don't defer it without support. The accounting treatment has to match the facts.

-

Expense acceleration

If you already know a genuine business cost is due, paying it in the current period can sometimes be more useful than delaying it. That isn't about inventing costs. It's about bringing forward real ones.

-

Capital expenditure timing

Equipment, tools, and other qualifying assets can change the tax position depending on when the business commits and when the accounting period closes.

-

Director pension contributions

These are often left until too late. For some companies near a threshold, acting before the year end can make the difference between staying in a lower band or drifting upward.

-

Accounting date choice

Your year end shouldn't be chosen once and then forgotten forever. Retail, construction, consultancy, and project-led businesses all have different cash and billing cycles.

If your profit estimate changes sharply in the final quarter, your original year-end plan may no longer be the best one.

The practical review to do before year end

Use a short pre-year-end checklist rather than waiting for the accounts to be drafted:

- Review projected profit: Don't rely on last quarter's estimate.

- List committed spending: Include software renewals, equipment, pension contributions, and overdue reimbursements.

- Check invoice timing: Make sure sales and costs sit in the right period.

- Revisit the year end: If the current date creates repeated pressure or poor visibility, reassess it.

A solid year-end accounts checklist helps turn those decisions into a routine instead of a last-minute scramble.

Leveraging Capital Allowances and R&D Credits

Some reliefs get ignored because owners assume they're only relevant to larger companies. That costs money.

Capital allowances matter to many SMEs because buying equipment, machinery, tools, and certain other assets isn't treated the same way as ordinary day-to-day spending. If the business is investing to grow, move premises, improve systems, or equip staff properly, this area deserves attention early rather than as an afterthought.

Capital allowances are practical, not technical fluff

I often see owners record an asset purchase correctly in the bookkeeping but never connect that purchase to the tax planning conversation. That's the gap.

If you're replacing plant, buying office equipment, investing in workshop tools, fitting out operational space, or upgrading hardware for a growing team, the tax treatment should be reviewed alongside the commercial decision. Waiting until year end narrows your options and increases the chance that useful detail goes missing.

A simple internal rule helps: whenever the business buys something substantial that will be used over time, flag it for tax review rather than assuming it sits with everyday expenses.

R&D is broader than most founders think

The term puts people off. They hear “research and development” and imagine white coats, patents, or a dedicated lab. In reality, many qualifying conversations start with a failed prototype, a software problem, a new internal system, or a technical obstacle your team had to work through.

If your company is building custom software, improving a production process, solving engineering uncertainty, or creating a new technical method to deliver work, it may be worth assessing whether the activity falls into the R&D relief space. Construction-adjacent firms, specialist manufacturers, software businesses, and product-led startups often dismiss this too quickly.

A project doesn't need to look groundbreaking in marketing terms to involve genuine technical uncertainty.

For a plain-English overview of criteria and common misconceptions, this resource on R&D tax incentive eligibility is a sensible starting point.

What works and what doesn't

What works is keeping contemporaneous evidence. Project notes, iterations, technical obstacles, failed attempts, design revisions, and staff time records all help support the position.

What doesn't work is trying to relabel ordinary commercial activity as innovation after the fact. A website refresh isn't automatically R&D. Routine service work isn't automatically R&D. General ambition to improve the business isn't enough on its own.

If you want to know how to reduce corporation tax without drifting into weak claims, this is the right approach. Review asset purchases as they happen, and assess innovation work while the detail is still fresh.

The Salary vs Dividend Marginal Relief Calculus

At this point, many director-shareholders leave money on the table.

The standard advice is familiar: keep salary low, take the rest as dividends. Sometimes that works. Sometimes it's lazy advice that ignores the company's actual profit position. The problem becomes sharper when profits sit just above the lower threshold.

According to Hargreaves Lansdown's discussion of limited company tax planning, many guides don't quantify the “cliff edge” risk for companies with profits just over £50,000. Their example notes that a £1,000 increase in allowable salary expense could reduce company profits below £50,000, which can trigger the 19% rate on the whole amount rather than leaving the company above the threshold.

Why the usual advice can fail

Low salary and high dividends often feels efficient because dividends aren't a corporation tax deduction, while salary is. But that's exactly why the calculation matters. If a modest increase in director salary reduces taxable profits enough to change the company's corporation tax position, the “obvious” dividend-heavy route may no longer be the better one overall.

This is especially relevant for startups and owner-managed companies in London where profits can cluster around the threshold without the owner realising the tax impact until after year end.

A worked example framework

Use this as a decision model, not as a complete personal tax computation. The point is to test whether a higher deductible salary creates a better overall outcome once the company's corporation tax position changes.

| Metric | Scenario A: Low Salary (£12,570) | Scenario B: Strategic Salary (£17,570) |

|---|---|---|

| Starting company profit before extra salary decision | £55,000 | £55,000 |

| Additional salary deducted | £0 | £5,000 |

| Taxable profit after salary decision | £55,000 | £50,000 |

| Corporation tax position | Above lower threshold, marginal relief range | At lower threshold |

| Key planning effect | Company stays above the lower limit | Company may access the lower 19% treatment |

That table is deliberately simple because most directors need the decision logic first.

How to run the calculation properly

Work through it in this order:

-

Start with updated management figures

Don't use old bookkeeping. Use current numbers with accruals, payroll, and known costs reflected.

-

Identify your true pre-planning profit

That's the profit before changing salary, pension contributions, or timing decisions.

-

Test one change at a time

Increase salary. Then model the revised company profit. Separately test pension contributions and other deductible items.

-

Look at the company and the director together

A lower corporation tax bill doesn't automatically mean a better overall result if the personal side worsens too much. The best answer is the combined answer.

-

Watch associated company issues

If you operate through multiple companies, the lower and upper limits can be divided across active group companies worldwide. That changes the planning entirely.

The right salary isn't the one that sounds tax-efficient in conversation. It's the one that works after you model the company profit properly.

Where directors usually go wrong

The common error is choosing the salary once, usually at the start of the year, and never revisiting it. But profits move. Staffing changes. A good trading quarter can push the company into a different range. By then, the original salary plan may be out of date.

This is one of the clearest examples of how to reduce corporation tax through calculation rather than rule-of-thumb advice. If your profits are anywhere near that lower threshold, the numbers need to be tested rather than guessed.

Advanced Strategies and Construction Industry Rules

Some planning areas sit beyond everyday expenses and timing. Loss relief and group relief can matter, particularly where one period is weak and another is strong, or where activities are split across connected companies. These aren't DIY topics. The rules are technical, and the benefit depends on the exact structure and timing.

For many North West London contractors, though, the more urgent issue is simpler. CIS and corporation tax are often recorded badly together, which leads to overpaying.

The CIS trap subcontractors miss

A common compliance trap is failing to claim the gross amount of CIS-settled income correctly for corporation tax purposes, as explained in this guide on ways to reduce corporation tax for CIS-affected businesses. Standard expense lists rarely explain the reconciliation properly, and that's where subcontractors can end up effectively taxed twice.

CIS deductions are not the same thing as an ordinary business expense. They are generally a tax deducted at source from payments made to you. If the bookkeeping only reflects the net cash received and ignores the gross income position, the company accounts can understate turnover and distort the tax calculation.

The clean way to account for it

For subcontractors, the practical logic is:

- Record the gross income: Use the full value of the work done, not just the cash that hit the bank.

- Track the CIS deduction separately: Treat it as a tax credit or prepayment position, not as if it were just another overhead.

- Reconcile contractor statements: Don't rely on bank entries alone.

- Review before filing: CIS suffered needs to match the supporting records.

Sector-specific bookkeeping matters. A contractor with multiple sites, irregular payment notices, and labour-heavy invoicing can't afford vague coding.

If you operate in construction, accounting support for contractors and construction businesses should include CIS-aware bookkeeping, statement reconciliation, and a year-end review of how those deductions flow into the corporation tax position.

Other advanced points worth reviewing

- Loss utilisation: If the business has had a weaker period, losses may be usable in a way that reduces future tax pressure.

- Group structures: Connected companies can create both opportunities and complications.

- Evidence quality: Advanced reliefs fail most often because the records don't support the claim cleanly.

Construction businesses don't usually overpay because they lack effort. They overpay because standard bookkeeping processes don't reflect how CIS works.

Your Corporation Tax Reduction Checklist and Next Steps

Before you do anything else, review the basics with fresh eyes. Most savings come from a handful of decisions made consistently, not from one dramatic tactic.

Use this checklist against your latest figures:

- Expenses reviewed: Have you claimed all legitimate business costs, including director-paid items and recurring software?

- Year-end timing checked: Are any real costs, pension contributions, or asset purchases better dealt with before the period closes?

- Salary and dividends tested: Have you modelled the company profit impact instead of relying on a standard split?

- Capital and innovation reviewed: Have you assessed asset purchases and any technically challenging development work?

- CIS reconciled properly: If you're in construction, are gross income and CIS deductions recorded correctly?

- Structure reconsidered: If you have associated companies or uneven profits, have you tested whether the current setup still makes sense?

A short walkthrough can help if you want a visual overview before acting:

The businesses that reduce corporation tax well usually have one thing in common. They review profit before the year closes, not after the return is due. That gives you room to choose, rather than report.

If you want a specific plan for your business, speak to Action Accountants Limited. We help North West London SMEs, startups, and construction businesses review profit, expenses, CIS records, and year-end decisions so the corporation tax position is legally efficient and properly supported.