Sole Trader Tax Return: A Stress-Free UK Guide for 2026

Action Accountants •26 June 2026

You've done the hard part already. You started the work, found clients, sent invoices, and got money coming in. Then tax season creeps into view and a simple question turns into several at once. Do I need to register? What records should I have kept? What goes on the form? Why is everyone warning me about Payments on Account?

That uncertainty is normal. A first sole trader tax return often feels more complicated than it is, mainly because HMRC uses formal language for what is, in practice, a series of routine admin steps. Once you know the order to tackle them in, the whole process becomes far less stressful.

This guide is written for new sole traders who want clear answers, practical habits, and a realistic view of the cash flow traps that catch people out, especially if income goes up and down during the year or you work in construction under CIS.

Table of Contents

- Start Your Journey The Right Way Registering for Self Assessment

- Your Blueprint for Financial Clarity Keeping Impeccable Records

- From Turnover to Taxable Profit A Practical Calculation Guide

- Navigating the Online Form SA100 and SA103 Explained

- Mastering Deadlines Payments and Crucial Tax Traps

- Is It Time to Hire an Accountant?

Start Your Journey The Right Way Registering for Self Assessment

You finish your first few jobs, the money starts landing in your account, and then the tax questions arrive all at once. Do you need to register now, after 5 April, or only once HMRC contacts you? New sole traders ask this every week, especially in trades and CIS work where income can start quickly and arrive irregularly.

If your gross trading income goes over £1,000 in the tax year, you usually need to register for Self Assessment. That £1,000 is the trading allowance, and it is one of the first checkpoints I use with new clients. Below that level, a tax return may not be needed. Above it, assume registration is part of the job and deal with it early.

Know when registration becomes necessary

The date that matters for registration is 5 October after the end of the tax year in which you started trading. So if you began working for yourself at any point up to 5 April 2025, HMRC expects you to register by 5 October 2025.

Many new sole traders mix that date up with 31 January. That causes trouble. January is usually the filing and payment deadline. October is the point where you get yourself set up properly, including your Unique Taxpayer Reference, or UTR.

Registering late creates practical problems before it creates tax problems. Your UTR can take time to arrive. Government Gateway access can take time to sort out. If your income is uneven, which is common in construction, freelancing, and seasonal work, a late start leaves you with less time to plan for the first tax bill and any Payments on Account that may follow.

That cash flow point matters more than many guides admit.

A sole trader who has had a strong first year can end up facing a larger January payment than expected, especially if no money has been ringfenced along the way. CIS subcontractors are often surprised by this. They may have tax deducted at source, but they still need to register, file properly, and check whether those deductions fully cover the final liability.

What registration looks like in practice

The process itself is straightforward if you do it in order.

- Confirm you are trading as a sole trader. If you are working in your own name and not through a limited company, this is usually the starting point.

- Check whether your income is over the trading allowance. Use total business income, not profit after expenses.

- Register with HMRC as self-employed. Do it as soon as the position is clear, rather than waiting for the deadline.

- Wait for your UTR. Keep that number somewhere safe because you will need it often.

- Set up your online tax account and Government Gateway access. That makes filing much easier later on.

I usually tell clients to treat registration as the first admin job that protects cash flow. Once you are registered early, you can estimate tax while the year is still in progress, set money aside monthly, and avoid the shock of a deadline-driven scramble. If you want help getting your records into shape from the start, our guide to bookkeeping for sole traders will make the next step much easier.

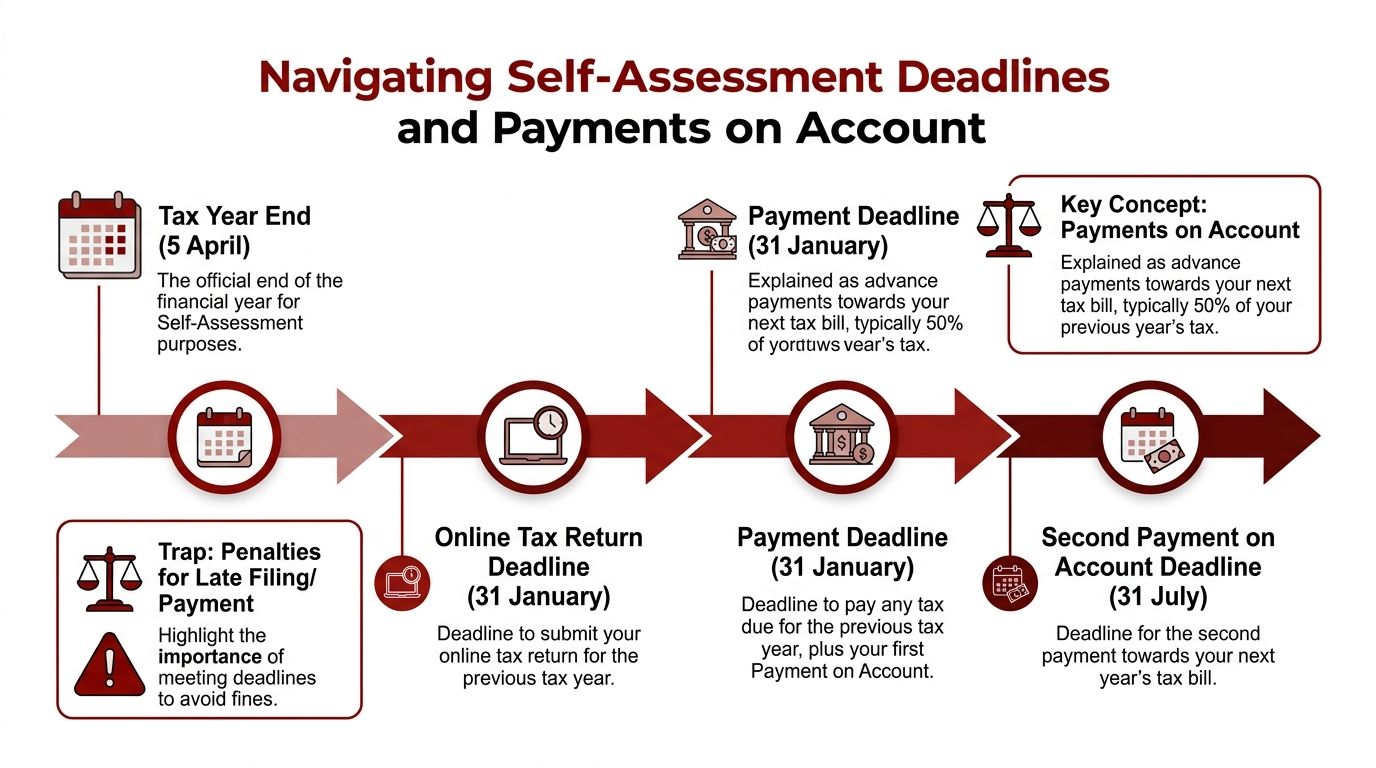

The tax year runs from 6 April to 5 April. Online returns are due by 31 January, and paper returns are due earlier, on 31 October. HMRC sets out the main Self Assessment deadlines on its official guidance, and if you also want a broader plain-English explanation of standards and reporting, this guide on what is financial compliance for 2026 gives useful context.

Write down four dates now. 5 April. 5 October. 31 October. 31 January.

That simple habit prevents a lot of expensive mistakes later.

Your Blueprint for Financial Clarity Keeping Impeccable Records

A sole trader can earn well and still get caught short in January. I see it all the time. The problem is rarely the tax return itself. The problem is weak records that hide what the business is making, what can be claimed, and how much cash should already have been set aside for tax.

Good records do two jobs. They support the figures on the return, and they show whether your cash flow can cope with the tax bill that is building in the background. That matters even more if your income jumps around during the year, because Payments on Account can land at exactly the wrong moment if you have been judging things by bank balance alone.

What to keep and how to keep it

HMRC requires sole traders to keep records of business income and expenses for at least five years after the submission deadline. That is the compliance side. The practical side is simpler. Keep records well enough that, if I ask how much you invoiced in November or what that tool purchase was for, you can answer in minutes rather than spending a Saturday searching emails.

For most sole traders, that means keeping:

- Sales records. Invoices, till records, payment confirmations, and notes of any cash taken.

- Expense evidence. Receipts, supplier invoices, subscription confirmations, and a note of the business purpose.

- Bank records. Statements from a separate business account make life much easier.

- Other business income. Grants, refunds, interest linked to the business, or insurance payouts.

- Private use notes. Any spending that was partly personal, plus goods or stock taken for personal use.

- CIS paperwork if you work in construction. Monthly CIS statements, contractor deductions, and a record of which invoices were paid under CIS.

That last point is often missed. For construction subcontractors, poor CIS records can mean tax deducted at source never gets properly credited on the return. I have seen subcontractors pay more than they should because the monthly statements were not kept together.

If you want a practical setup you can stick to, our guide to bookkeeping for sole traders shows a simple way to organise records before the paperwork starts piling up.

Good records protect cash flow because they show the tax position early, while there is still time to put money aside.

Why this matters beyond compliance

A spreadsheet updated once in January usually gives a false sense of control. It might be enough to file. It is rarely enough to plan.

The difference shows up when income is uneven. A designer might have a strong autumn and a quiet spring. A CIS subcontractor might have three busy site contracts, then a gap. On paper, the annual profit can still be healthy. In the bank, the cash may already have been used for materials, fuel, van costs, or household bills. Without current records, the first proper estimate of tax arrives too late.

That is where monthly bookkeeping earns its keep. Not because HMRC likes tidy records, but because you can spot the likely tax bill while there is still time to ringfence part of each payment. You can also see whether Payments on Account are likely next time, which is one of the biggest cash flow shocks for newer sole traders.

A monthly routine that works

Keep it boring and repeatable. The best systems are the ones you will use.

| Task | What to do |

|---|---|

| Review income | Match invoices and sales to money received |

| Review spending | Put expenses into clear categories while they are still fresh |

| Check missing items | Chase receipts, CIS statements, and unclear bank transactions |

| Store records | Save copies by month in folders or software |

| Estimate tax | Check profit to date and move money aside for tax and National Insurance |

That final step is the one many sole traders skip. It is also the one that prevents trouble later.

Keep the system simple from day one

You do not need expensive software if the business is still small. A separate bank account, a clean spreadsheet or bookkeeping app, and a half hour each month is enough for many people at the start. What matters is consistency and a clear split between business and personal spending.

If you are trying to understand the wider compliance picture, this practical explainer on what is financial compliance for 2026 gives useful context for why businesses are being pushed towards better record systems and more structured reporting.

Messy records create three predictable problems. Expenses get missed. Income gets guessed. Tax payments arrive before the cash is ready.

Clean records fix all three.

From Turnover to Taxable Profit A Practical Calculation Guide

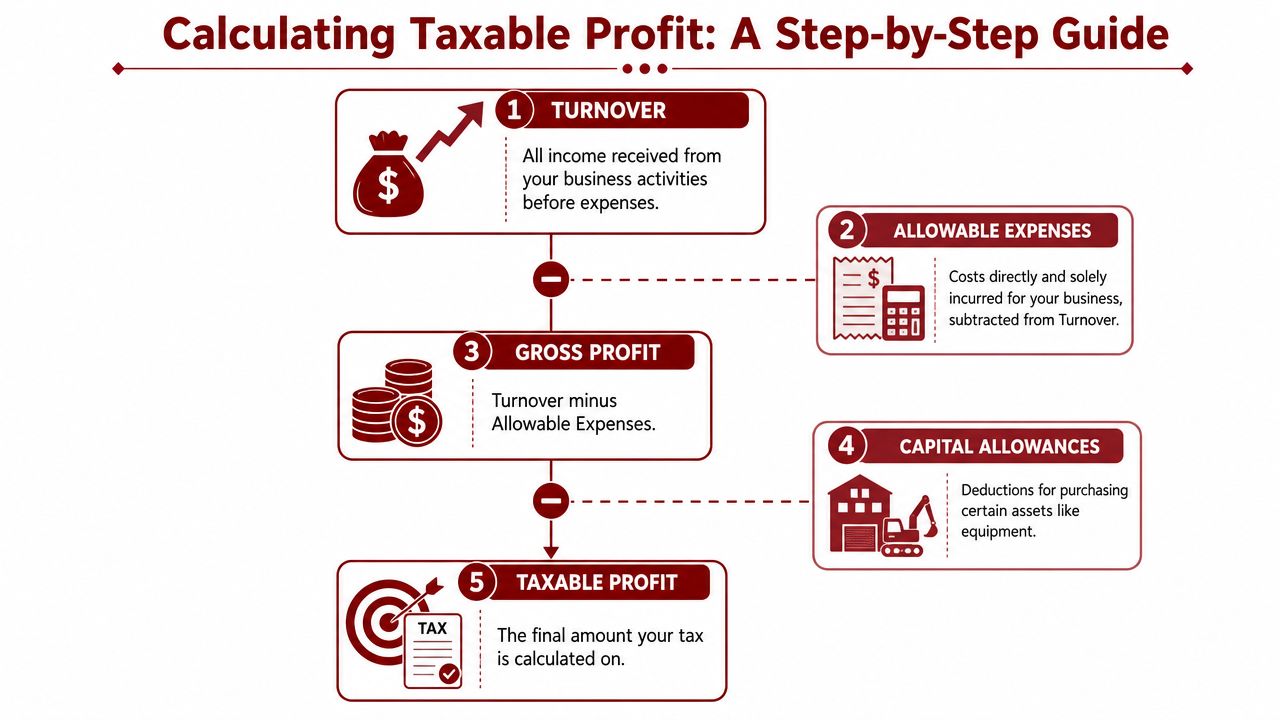

The phrase “how much tax will I pay?” is usually asked too early. The first question is simpler. What was your taxable profit?

That figure sits at the centre of a sole trader tax return. To get there, you start with everything the business brought in, then subtract the expenses that count.

Start with turnover not profit

Turnover means your total business income before expenses. For a sole trader, that generally includes sales and other business receipts. The figure needs to be complete before you think about deductions.

The common error is using what's left in the bank account as a shortcut. That doesn't work. Bank balance and taxable profit are not the same thing. Money may have come in late, gone out on equipment, or been transferred in a way that needs proper classification.

If you're visual and want a quick overview before reading further, this short video gives a helpful primer on the process:

Work out allowable expenses carefully

This is the area where people either miss legitimate deductions or push too far and create problems. The test is whether the cost was incurred for business purposes.

Common examples include:

- Tradesperson costs. Materials, small tools, protective clothing where appropriate, and vehicle running costs where business use is properly recorded.

- Freelancer costs. Software subscriptions, domain renewals, design tools, and professional subscriptions tied to the work.

- Home-based business costs. A fair business proportion of certain running costs where home is used for work.

- Admin costs. Printing, postage, office supplies, and phone costs related to business use.

- Professional support. Bookkeeping, accountancy, and tax support connected to the business.

A builder buying materials for a job is straightforward. A graphic designer paying for Adobe software used for client work is straightforward. A meal with a friend that turns into a business chat usually isn't.

For a fuller breakdown of categories that often apply, this guide to tax-deductible expenses for self-employed people is useful to keep beside your records.

Common mistake: claiming based on what feels business-related rather than what you can actually support with records and a clear business purpose.

Turn the figures into a tax-ready number

The working formula is simple:

Turnover minus allowable expenses equals taxable profit

That's the figure used as the basis for Income Tax and National Insurance calculations on a sole trader tax return. Keep the logic clean. Total up all business income. Total up all allowable expenses. Reconcile both against your records. Then review anything unusual before filing.

Where people go wrong isn't usually the arithmetic. It's the classification. They miss income that hit a personal account, forget a receipt sitting in an email folder, or include personal spending because they paid for it on the same card as business items.

If you work in construction, this section needs one extra layer of care. CIS deductions affect cash received, but they don't change the need to calculate turnover and expenses correctly. The deduction side has to be handled properly on the return too, which matters when you come to the filing stage.

Navigating the Online Form SA100 and SA103 Explained

A lot of sole traders expect the online return to be the hard part. Usually, it isn't. The pressure point is entering the right figures in the right boxes, especially if your income moves around month to month and you need the final tax calculation to be reliable for cash flow planning.

The online return has two main parts here. SA100 is your personal tax return. SA103 is the self-employment section where you report the business side of your sole trader work.

For most clients, I explain it like this. SA100 tells HMRC who you are and what else affects your tax position. SA103 tells HMRC how the business performed.

What goes where

The SA100 covers your personal details and any other income or claims that apply to you. The SA103 is where you enter business turnover, allowable expenses, and the resulting profit.

If you work under CIS, take extra care at this stage. Your sales still go in at full turnover, not just the money that landed in your bank after deductions. CIS tax taken by contractors is dealt with separately on the return. Get that wrong and the tax calculation can be badly distorted.

That matters for one reason above all. The number HMRC produces from this return does not just affect what you owe now. It can also affect next year's advance payments. If your income is uneven, read our guide to Payments on Account for sole traders with changing profits before you submit, so the result does not catch you off guard later.

A practical way to complete it

Treat the form as a transfer exercise, not a thinking exercise.

Use the figures from your records and work through the return in order:

| Part of the return | What to check before entering it |

|---|---|

| Personal details on SA100 | Name, address, UTR, date of birth, and anything else HMRC already holds |

| Self-employment pages on SA103 | Turnover, expenses, accounting dates, and business description |

| Tax deducted under CIS | Statements from contractors match what you are claiming |

| Final review | Figures agree to your records and anything unusual has an explanation |

The mistakes I see most often are basic but expensive. A trader copies net CIS income instead of gross income. Someone guesses an expense total because the receipt trail is incomplete. A client rushes through the review screen and misses a wrong digit that changes the whole liability.

Avoid problems before you click submit

Check personal details against HMRC records first. Then check the business figures against your bookkeeping. After that, review anything unusual, such as large motor costs, home office claims, or subcontractor deductions.

If someone else approves the return for you, use a secure process to ensure legal document signing. That is especially useful where approval happens remotely and you want a clear record of what was agreed and filed.

Save a copy of the submitted return and the tax calculation. That sounds obvious, but it becomes very useful later if you are applying for a mortgage, checking Payments on Account, or querying a CIS credit that has not flowed through properly.

Once the figures are prepared properly, the online form is usually just the final admin step.

Mastering Deadlines Payments and Crucial Tax Traps

A common January conversation goes like this. A sole trader has finished the return, checked the tax bill, and thinks they can just about cover it. Then they spot a second figure on the calculation. That extra amount is often what creates significant pressure.

For many sole traders, the return is manageable. Paying it without raiding working cash is the harder part. That is even more true if income rises and falls through the year, which is exactly why tax planning needs to follow cash flow, not just filing dates.

The deadline that matters most

A key date in the tax calendar is 31 January. It is the online filing deadline for the previous tax year, and it is also the deadline to pay any tax due.

That combination matters more than the tax rates on paper. If the books are still being sorted in January, two problems land at once. There is admin pressure to finish the return and cash pressure to fund the payment.

Miss the deadline and the costs start quickly. File late, pay late, or do both, and HMRC can add penalties and interest. I tell clients to treat January as the finish line for work done much earlier, not the month to start pulling everything together.

Why Payments on Account catch people out

Payments on Account are advance payments towards the next tax year, based mainly on the previous year's bill. They make sense if profits are steady. They can be awkward if income is lumpy.

This is the point many new sole traders do not expect. A strong year can create a large January bill and a demand for advance payments towards the following year, even if current work has already slowed down. I see it a lot with traders who had one unusually good contract, a busy run of seasonal work, or a short spell of high-margin jobs.

That is why tax is a cash flow issue first and a compliance issue second.

A sensible approach is:

- Set aside tax money every month. The business account balance is not the same thing as available cash.

- Recheck profit during the year. One estimate in spring is rarely enough if income swings.

- Remember the July payment. The second instalment often arrives before the cash from newer work has settled.

- Reduce Payments on Account carefully if income is falling. The claim has to be realistic. Cut it too far and you can create interest charges later.

If you want the mechanics set out clearly, our guide to how Payments on Account work for sole traders explains when they apply, how the dates work, and when a reduction may be sensible.

Tax trouble usually starts with poor reserving, not with the tax return itself.

One related admin job is keeping signed records in order. If you approve returns, engagement letters, subcontractor paperwork, or client documents remotely, it helps to understand how to ensure legal document signing so the paperwork is properly evidenced later.

Special note for CIS subcontractors

Construction subcontractors often get caught by generic advice that ignores how CIS works in practice. Tax may already have been deducted by contractors, but the return still needs to show the right income and the right CIS tax suffered. If either figure is wrong, the credit can be missed or understated.

The usual trouble spots are familiar:

- Missing CIS statements. Without them, it is harder to prove what has already been deducted.

- Using the wrong income figure. The return needs the correct gross income, not just the net amount received after deductions.

- Messy site spending. Tools, materials, fuel, travel, and personal purchases can get mixed together very quickly.

CIS also creates its own cash flow pattern. Money is deducted before you see it, refunds can be delayed if the return is wrong, and workload can change fast from one contractor to the next. In practice, that means construction workers need tighter record-keeping and a more deliberate tax reserve than many general guides suggest.

Is It Time to Hire an Accountant?

Some sole traders can handle their own tax return perfectly well. Others spend far too long trying to save money on fees and end up paying in stress, lost time, or avoidable mistakes.

The right question isn't “Can I submit the form myself?” It's “Am I getting this right, and am I running the business better because I'm doing it myself?”

When DIY still works

Doing your own sole trader tax return is usually manageable when your affairs are straightforward and your records are tidy all year. You invoice clients clearly, keep expenses organised, understand what belongs in the business, and don't leave decisions until the deadline is close.

It also helps if you're comfortable reading HMRC prompts without second-guessing every line. Some people are. Many aren't.

DIY tends to work best when:

- Your income stream is simple. A small number of clients and a clear service line.

- Your records are current. Not reconstructed in a panic.

- You understand your expenses. You know what's allowable and what isn't.

- You're prepared for tax cash flow. January and July won't blindside you.

When expert help usually pays for itself

The case for hiring an accountant gets stronger when the business becomes less linear. Construction workers under CIS are an obvious example. Landlords with self-employment income are another. Anyone moving towards more complex compliance usually benefits from someone who can see the whole picture, not just the return itself.

An accountant often becomes worthwhile if:

- You work in construction under CIS. Sector-specific handling matters.

- Your income varies sharply. Payments on Account become harder to judge alone.

- You're approaching digital reporting changes. Systems matter more now than they used to.

- You want tax efficiency, not just compliance. Filing correctly is only the baseline.

- You've fallen behind on bookkeeping. Catch-up work is harder without a method.

There's also a broader business reason. A good accountant doesn't just file figures. They help you separate personal and business spending, improve your records, spot weak admin processes, and make tax less reactive.

If you're weighing up that decision, this piece on 8 ways an accountant can help your small business is a practical place to start. For a wider industry view, Solo AI's perspective on accountants is also interesting because it frames the accountant's role as part compliance support, part decision support.

The best time to hire an accountant is usually before you feel overwhelmed, not after.

A sole trader tax return is rarely difficult because the rules are impossible. It becomes difficult when registration was late, records are incomplete, cash has already been spent, or specialist issues like CIS are handled too casually. That's when professional input stops being a luxury and starts being the sensible option.

If you want straightforward help with your sole trader tax return, bookkeeping, CIS matters, or practical tax planning, Action Accountants Limited offers clear, responsive support for self-employed people, contractors, landlords, and growing businesses across North West London and the wider UK.