Your Guide: What Is Psc Register for UK Companies in 2026

Action Accountants •14 July 2026

The UK's Persons with Significant Control register is a mandatory record that most companies must keep to identify the people who ultimately own or control them. In practice, that means recording anyone who holds more than 25% of shares or voting rights, can appoint or remove most of the board, or otherwise exercises significant control.

If you've just set up a company, this is one of those filings that often appears halfway through incorporation paperwork and immediately raises questions. You know your business. You know who invested what. But the phrase PSC register sounds more technical than it needs to be, and that's where many founders get stuck.

The confusion is understandable. A single-founder company can still need a PSC entry. A company can also have no registrable person, and leaving the register blank is not the same thing. Ownership through another company, a trust, or informal control arrangements can make things less obvious than the share split suggests.

The good news is that PSC compliance is manageable once you strip it back to the actual decisions you need to make: who counts, what details to collect, when to update the record, and what to do if nobody meets the test. If you're weighing up incorporation against staying unincorporated, this also sits alongside wider setup issues such as choosing between a limited company and sole trader structure.

Table of Contents

- An Introduction to the PSC Register

- Who Counts as a Person with Significant Control

- Your Company's Legal Obligations for the PSC Register

- Common Exemptions and Special Scenarios

- The Penalties for PSC Register Non-Compliance

- Your PSC Compliance Checklist and Next Steps

An Introduction to the PSC Register

A founder incorporates a company on Friday, starts a bank account application on Monday, and is suddenly asked for PSC details. That is usually the moment this stops feeling like routine admin. The PSC register is the company's legal record of who ultimately owns or controls it, and for many startups it needs attention from day one.

Since April 2016, most UK companies and LLPs have had to keep this record as part of the UK's corporate transparency rules. In practice, that means even a simple owner-managed business has to check the position, record it correctly, and keep it up to date. Small does not mean exempt.

For new founders, the confusion often starts earlier, at the business structure stage. If you are still deciding whether to incorporate, it helps to understand the wider compliance difference between a limited company and a sole trader. A PSC register is one of those company-only obligations that catches people by surprise after incorporation.

The practical point is straightforward. Do not rely on the ownership picture being "obvious". A company with one shareholder may have a simple PSC outcome, but it still needs the right entry on the register. A company with two or three founders often needs a closer look, especially where voting rights, investor consents, or appointment rights do not match the share split.

Founders also worry about the opposite problem. What if there is no PSC? That can be a genuine result, but only after the company has taken reasonable steps to check. The answer is not to leave the register blank. The answer is to record the correct statutory position and keep evidence of how you reached it.

That is why I treat PSC compliance as a short process, not a legal mystery. Identify the people or entities with control, confirm the details, enter the prescribed wording, and review it whenever ownership or governance changes. If your cap table includes overseas owners or nominee arrangements, it also helps to understand the overlap with beneficial ownership concepts. This guide on essential UBO and shareholder information for founders is a useful companion on that point.

Handled early, the PSC register is manageable. Left until a bank, investor, accountant, or buyer asks for it, it becomes a scramble.

Who Counts as a Person with Significant Control

A common startup scenario looks simple on paper. Two founders hold 50% each, an angel investor has veto rights over major decisions, and one founder can appoint most of the board. That company can have PSC issues that the cap table alone does not show.

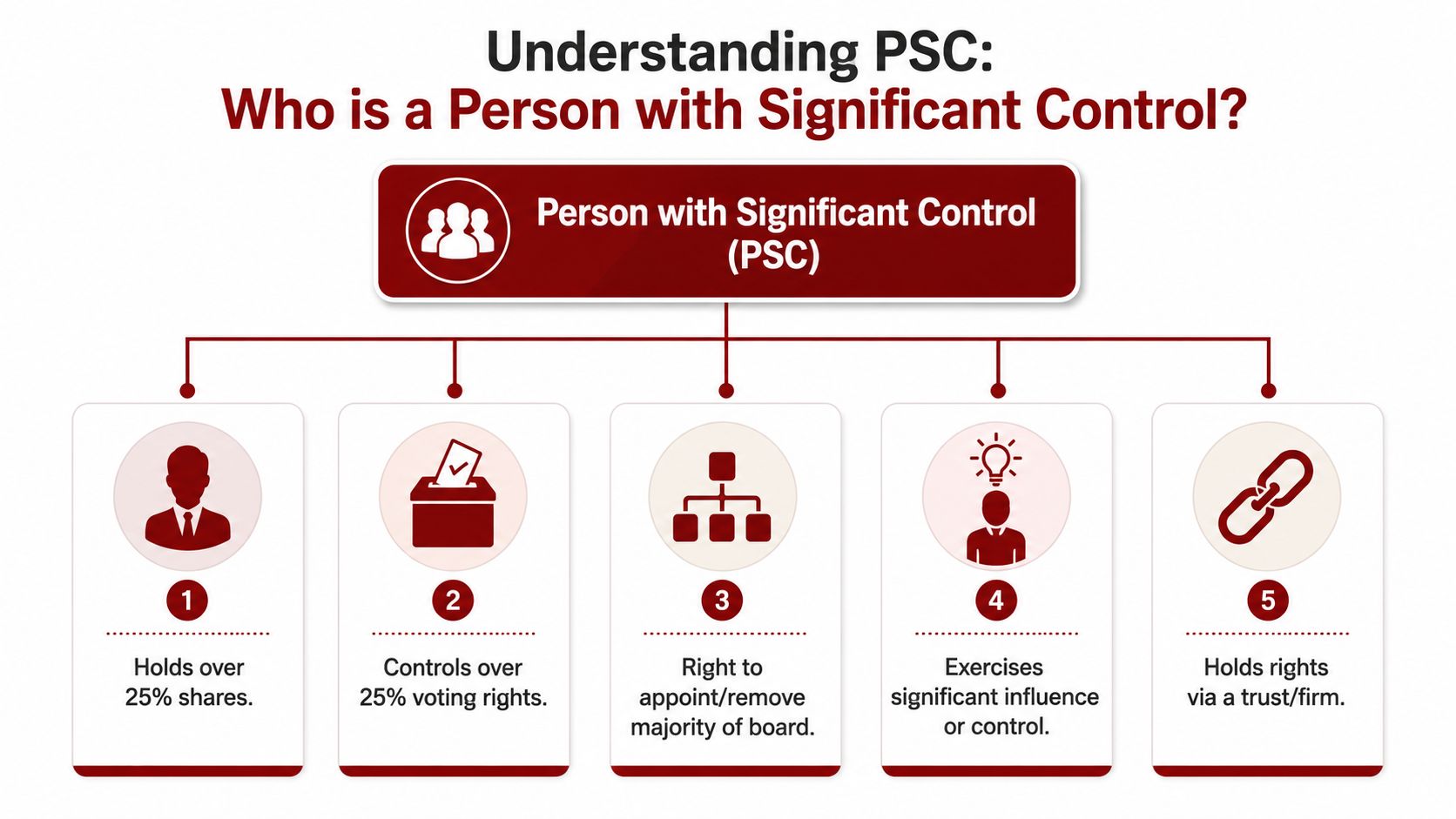

A person counts as a PSC if they meet at least one of five legal conditions for ownership or control. For most small companies, the practical job is to test each founder, investor, parent company, or trust arrangement against those conditions rather than guessing from the share certificates.

The five tests that matter

Use these five questions as a working checklist:

-

Do they hold more than 25% of the shares?

If yes, record them as a PSC, subject to the usual checks on whether an RLE should be entered instead. -

Do they control more than 25% of the voting rights?

This catches companies with different share classes, weighted voting, or side arrangements that separate voting control from economic ownership. -

Can they appoint or remove a majority of the board?

Board appointment rights often sit in shareholders' agreements or bespoke articles, so this point gets missed in early-stage companies. -

Do they exercise significant influence or control?

This is the harder judgment call. It can apply where someone has a standing right to block key decisions or routinely directs the company's affairs without holding enough shares to meet the earlier tests. -

Do they control rights through a trust or firm?

If the shares or voting rights sit inside a trust or partnership-style structure, look through that arrangement and identify who controls those rights.

The practical mistake is stopping after question one.

Direct control, indirect control, and RLEs

Direct control is straightforward. An individual personally holds the shares or voting rights and meets one of the tests.

Indirect control needs a closer review. If a company owns the shares in your trading company, the correct register entry may be a Relevant Legal Entity, or RLE, rather than an individual name at that stage. Founders often miss this and assume every PSC register must list a natural person. It can list an RLE where the legal conditions are met.

Use this as a quick guide:

| Situation | Register approach |

|---|---|

| Individual directly holds the relevant rights | Record the individual PSC |

| Qualifying company or other legal entity holds the rights | Check whether it should be recorded as a registrable RLE |

| Trust or firm arrangement sits in the chain | Review who controls the rights behind that structure |

The phrase "significant influence or control" causes the most hesitation in practice. I tell founders to start with the formal documents. Review the articles, shareholders' agreement, reserved matters, and any investor consent rights. Then compare that paperwork with how decisions are made. If one person can consistently force or block major decisions, that deserves a proper PSC analysis.

The "no PSC" outcome can also be correct. Some companies have no registrable PSC because no individual or RLE crosses the legal thresholds. In that case, the answer is not to leave the register empty. The answer is to record the proper statutory statement and keep a file note showing the checks you carried out.

If you're trying to separate legal ownership from beneficial influence, this guide to essential UBO and shareholder information for founders helps clarify where founders often mix up PSC and beneficial ownership concepts.

For owner-managed companies, the same person may be a director, shareholder, and PSC, but those are different legal roles with different filing duties. If you want a clearer picture of the wider admin position, this guide to National Insurance for directors is a useful companion.

Your Company's Legal Obligations for the PSC Register

A common startup mistake goes like this. The founders sort the cap table, file the incorporation paperwork, then assume PSC can wait until the next Confirmation Statement. By the time an investor comes in or shares move between founders, the register is already out of date.

That is avoidable if you treat PSC work as part of your normal company admin, not a once-a-year clean-up.

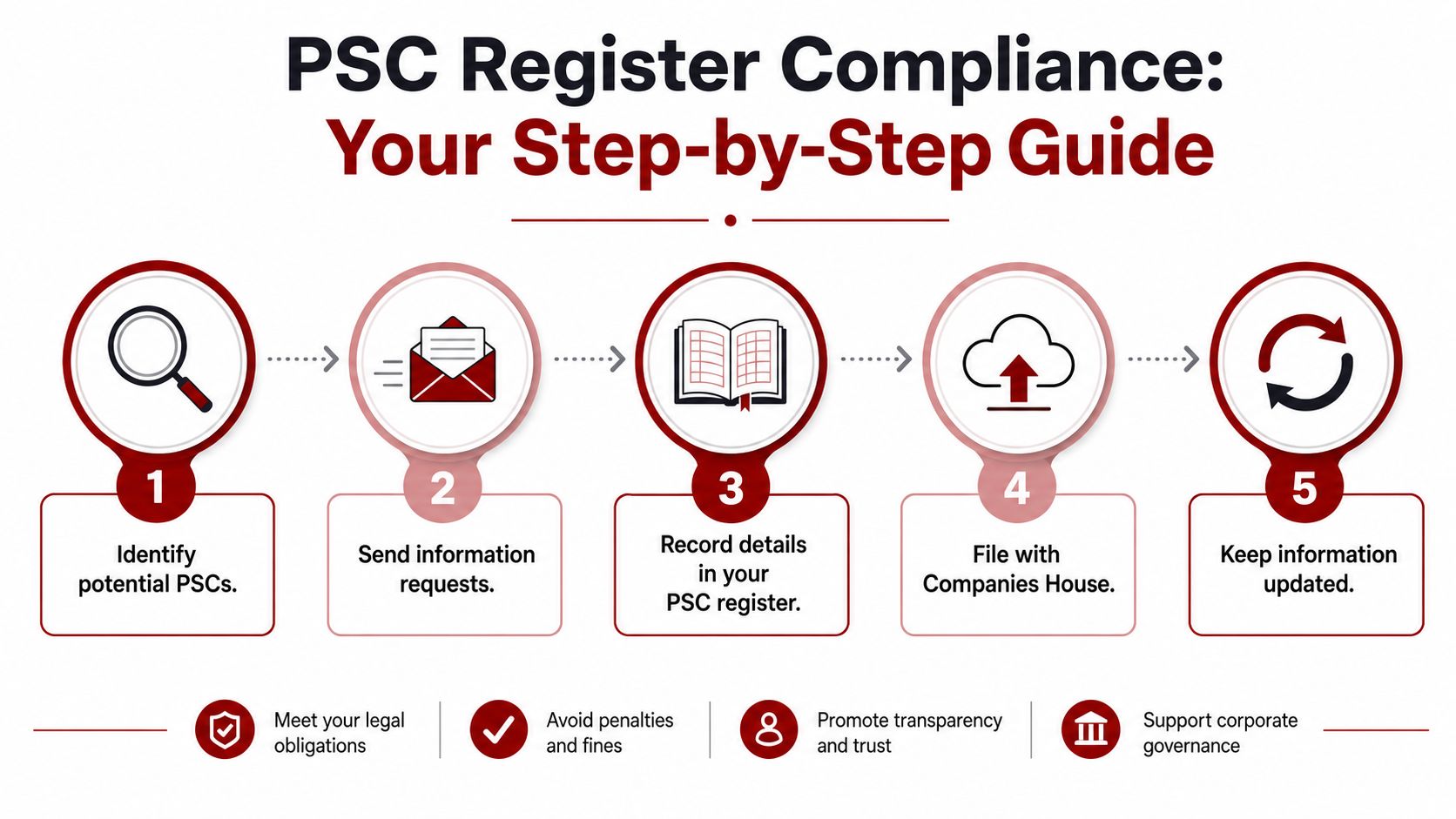

A workable compliance process

Use a simple operating checklist.

-

Review the current control position. Check the share register, voting rights, articles, shareholders' agreement, investment documents, and any side letters that affect board appointments or reserved matters.

-

List each possible PSC or RLE. Start with the obvious shareholders, then test whether a company, trust arrangement, or contractual right changes who controls the business.

-

Take reasonable steps to confirm the facts. If the position is unclear, contact the relevant person and ask for the information you need before you update the register.

-

Update the PSC register promptly. Record the confirmed details, or enter the correct statutory statement if the company has no registrable PSC or is still investigating.

-

File the Companies House update within the deadline. In practice, founders should work on the 14 day internal update period, followed by the further 14 days to notify Companies House. Waiting for the annual Confirmation Statement is the mistake that causes trouble.

That last point matters. PSC changes are event-driven. A share allotment, a transfer, a new investor consent right, or amended articles can all trigger a review straight away.

If you want a short explainer before dealing with the filing process, this video is a useful starting point.

What information must be recorded

The register needs specific particulars, not a loose description. For an individual PSC, that usually includes their name, service address, country or state of usual residence, nationality, date of birth, usual residential address, the date they became registrable, and the nature of their control.

For example, writing “founder and owner” is not enough. The entry needs to state the legal basis of control, such as holding shares or voting rights within the relevant band, or having the right to appoint or remove a majority of the board.

The no PSC scenario also needs proper handling. Do not leave the register blank because no one appears to meet the tests. Enter the correct statutory wording and keep a file note showing what you checked, when you checked it, and why you reached that conclusion. That paper trail helps if Companies House, a bank, an investor, or a buyer asks questions later.

A practical internal process usually works best:

- Keep one evidence file: Store share allotments, stock transfer forms, shareholder resolutions, articles updates, and investor documents together.

- Tie each PSC entry to a document: If someone is recorded because of shares, keep the allotment or transfer evidence with the register note.

- Create review triggers: New funding, founder exits, share reorganisations, new veto rights, and changes to board appointment rights should all trigger a PSC check.

- Give one person ownership: One named director, founder, or admin lead should monitor deadlines and make sure filings are completed.

Fast-growing companies often find that PSC work exposes a wider governance gap. In those cases, it helps to understand the role of a company secretary and related compliance support, even if the company does not appoint one formally.

Common Exemptions and Special Scenarios

Many online guides often become too thin here. They explain the five conditions, then stop just before the awkward situations founders struggle with.

Who may be exempt

Some entities are exempt, but the exemption is narrower than many people assume. Broadly, exemption is tied to certain companies whose voting shares are admitted to trading on regulated markets. By contrast, companies listed on UK secondary markets such as AIM and NEX have had to maintain a PSC register since 24 July 2017, as noted in this explanation of PSC rules and listed company treatment.

For startups and SMEs, the practical takeaway is simple. Don't assume you're exempt because you have investors, a holding company, or outside advisers. Most private companies are within scope.

How to handle a genuine no PSC outcome

The no PSC scenario is real, and it deserves more attention than it gets.

Some companies, after taking reasonable steps, accurately conclude that there is no registrable person or registrable relevant legal entity. UK law requires that position to be recorded formally. Leaving the register blank is a compliance failure, as explained in this practical note on PSC registers and no registrable person wording.

This matters especially for founders who have recently incorporated after trading on their own. A sole trader may assume, “I own the business, so I must automatically be the PSC.” Sometimes that will be right once the limited company is formed. Sometimes the legal position is more complicated because control sits in a different arrangement than the founder expects, or because the company structure no longer mirrors the old sole trader reality.

What works is evidence. Keep a short internal note of the steps taken:

- Review the cap table: Confirm who holds shares and voting rights.

- Check constitutional documents: Articles and agreements may create control rights beyond simple ownership.

- Consider indirect influence: Ask whether anyone can direct major decisions even without formal share control.

- Record the conclusion: If there is no registrable person, enter the required official position rather than leaving silence.

“No PSC” is a conclusion you reach after checking the facts. It's not a shortcut to avoid a difficult analysis.

A final nuance matters for future planning. From 18 November 2025, Companies House is stated to maintain the central PSC register exclusively and local registers are no longer required, with identity verification obligations applying to PSCs and RLEs under the changes described in the same Equiniti guidance linked above. If you refer to this point in planning, treat it as a rule change effective from that date rather than something that applied before it.

The Penalties for PSC Register Non-Compliance

A common startup scenario goes like this. The company is incorporated on Monday, the bank account is opened by Friday, and six months later an investor or bank asks for PSC records that nobody has properly dealt with. That is usually when founders realise this is a live compliance duty, not an admin task to leave until year end.

Failing to deal with the PSC regime can expose both the company and its officers to criminal penalties. In practice, the first damage is often commercial. Due diligence slows down, banks ask more questions, and advisers spend time fixing records that should have been right from the start. If you are already working with an accountant who supports small business compliance and growth, ask them to flag ownership changes early so the legal record stays aligned with the finance record.

Where founders usually get caught out

The mistakes are usually routine:

- No PSC record was made at all: The directors assumed the Companies House filing was enough.

- The position changed and nobody updated it: A share issue, transfer, or investment round altered control.

- The analysis stopped at the cap table: Someone had appointment rights, veto rights, or another form of control that was missed.

- The company left the register blank: The directors had not completed the analysis needed to confirm there was no registrable PSC.

These problems tend to surface at the worst time. A funding round, a sale process, a regulated customer onboarding check, or a bank review will usually expose weak PSC records very quickly.

There is another risk point. If the company sends notices to a person it believes is a PSC, or knows that person could be a PSC, failing to follow up properly creates its own compliance problem. Equally, a recipient who ignores a valid notice can face consequences. The practical answer is simple. Ask the questions promptly, keep a written trail, and record the outcome clearly.

Good PSC compliance is not complicated. It is evidence-based, kept up to date, and easy to produce when someone asks for it.

Your PSC Compliance Checklist and Next Steps

Founders don't need a lecture here. They need a list they can use this week.

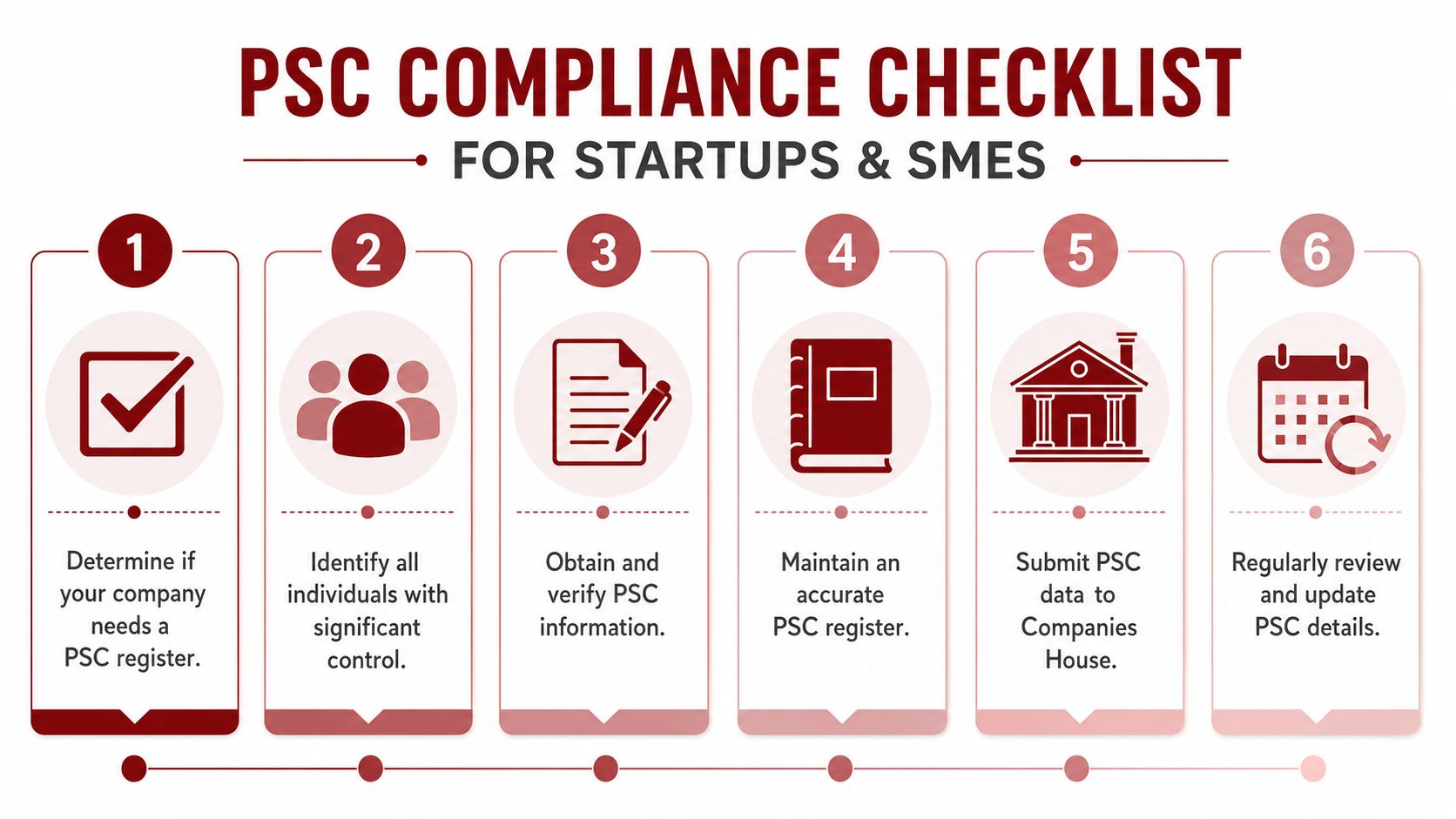

A founder-friendly checklist

Use this as a practical audit.

- Confirm scope: Check whether your company is one of the entities that must keep PSC information. For most private companies and LLPs, the answer will be yes.

- Map control properly: Review shares, voting rights, board appointment rights, and any arrangements that give someone significant influence.

- Identify individuals and RLEs: Don't assume the answer must be a natural person.

- Collect the required particulars: Make sure the details are complete and match the legal basis for control.

- Create the record immediately: Don't wait for the first annual filing cycle.

- Diary changes: Treat investment rounds, shareholder changes, and amendments to governance documents as review triggers.

- File changes promptly: Build the filing deadlines into your compliance calendar.

- Record no PSC if appropriate: If no registrable person exists after reasonable steps, state that formally.

- Review alongside the Confirmation Statement: Use the annual confirmation process as a secondary check, not the only check.

- Keep evidence together: Store the register, notices, shareholder documents, and board records in one accessible file.

What usually works best

For very small companies, a simple digital compliance file can be enough if one person owns the process and updates it promptly.

For growing SMEs, what works better is discipline: one owner for filings, one source of truth for share and control records, and a standing review whenever the ownership picture changes. What doesn't work is assuming the accountant, lawyer, founder, and co-director have all handled it between them.

PSC compliance also sits within a wider set of finance and governance tasks. If you're tightening up your admin generally, this guide on ways an accountant can help your small business is worth reading because founders rarely struggle with PSCs in isolation. It usually appears alongside payroll, VAT, confirmation statements, and record-keeping.

If you searched for what is PSC register, the plain answer is this: it's your company's formal record of who ultimately owns or controls it, and your job is to make sure that record is accurate, current, and supportable. Once you treat it as a routine governance process rather than a mysterious legal form, it becomes much easier to manage well.

If you want help getting the PSC position right from the start, Action Accountants Limited can support you with company formation, company secretarial work, statutory compliance, and the practical record-keeping that founders often don't have time to build themselves. For startups, SMEs, contractors, and growing owner-managed businesses, that means clear advice, accurate filings, and a cleaner compliance process from day one.