What Is CIS Deduction? a Contractor’s Guide for 2026

Action Accountants •11 July 2026

CIS deduction is a mandatory advance tax payment system for the UK construction industry. Contractors deduct 20% for verified subcontractors, 30% for unverified or unregistered subcontractors, and 0% for subcontractors with Gross Payment Status.

If you've just taken on your first subcontractor, this is usually the point where the uncertainty starts. The work is done, the invoice lands, and suddenly you're asking a very practical question. What is CIS deduction, and what exactly am I meant to take off, report, and pay over to HMRC?

The simplest way to think about it is this. CIS works a lot like PAYE in principle, but for construction subcontractors rather than employees. The contractor withholds part of the payment and sends it to HMRC as an advance against the subcontractor's tax and National Insurance, so the money isn't treated as a separate tax in its own right.

That sounds straightforward until real invoices get involved. Materials are on the bill. VAT is included. The subcontractor says they're registered. HMRC talks about verification. Then monthly returns come into the picture. Most mistakes happen in those small details, and those mistakes affect cash flow fast.

This guide deals with the parts that usually trip people up. In particular, the difference between being registered and being verified, and the right way to calculate CIS on labour-only costs so you don't over-deduct.

Table of Contents

- What Is CIS and Why It's Critical for Your Construction Business

- The Core CIS Framework Explained

- Understanding Your CIS Deduction Rate

- How to Calculate and Report CIS Deductions Correctly

- Worked Examples of CIS Deductions in Action

- Reclaiming CIS How Subcontractors Get Their Money Back

- Avoid CIS Pitfalls and Take Control with Action Accountants

What Is CIS and Why It's Critical for Your Construction Business

A typical CIS mistake starts on a Friday afternoon. The job is done, the invoice is in, the subcontractor wants paying, and someone in the office asks a simple question. Do we pay this in full, or do we make a deduction?

If you guess, you can create two problems at once. HMRC can treat the payment as wrong, and the subcontractor can lose cash because too much was held back. In practice, the expensive errors are rarely about the existence of CIS. They come from getting the status check wrong and taking deductions from the wrong part of the invoice.

CIS requires contractors to deduct money from certain payments to subcontractors and send that amount to HMRC as advance tax. For a new contractor, the practical point is straightforward. CIS changes how you pay, how you check subcontractors before payment, and how you read an invoice that mixes labour, materials, and other charges.

That matters because construction businesses often lose money through over-deductions, not just underpayments to HMRC. I see this a lot with labour-heavy invoices. Someone applies the rate to the whole bill instead of the labour element that falls within CIS. The subcontractor is then paid short, the records need correcting, and the month-end return becomes harder than it needed to be.

Another point catches businesses by surprise. CIS is not limited to firms that see themselves as building contractors. Some businesses trigger contractor obligations because of the level of construction spending, even when construction is not their main trade. That is one reason owners often realise they should have set up CIS only after they have already started paying subcontractors.

The other trap is confusing registered with verified. Those are not the same thing, and the difference affects the deduction rate you use. Getting that wrong is one of the most common causes of avoidable cost.

If you have not set things up yet, sort that before the next payment run. Start with this guide on how to register for CIS, then make sure your team has a clear process for checking subcontractor status and isolating labour-only costs before any money goes out.

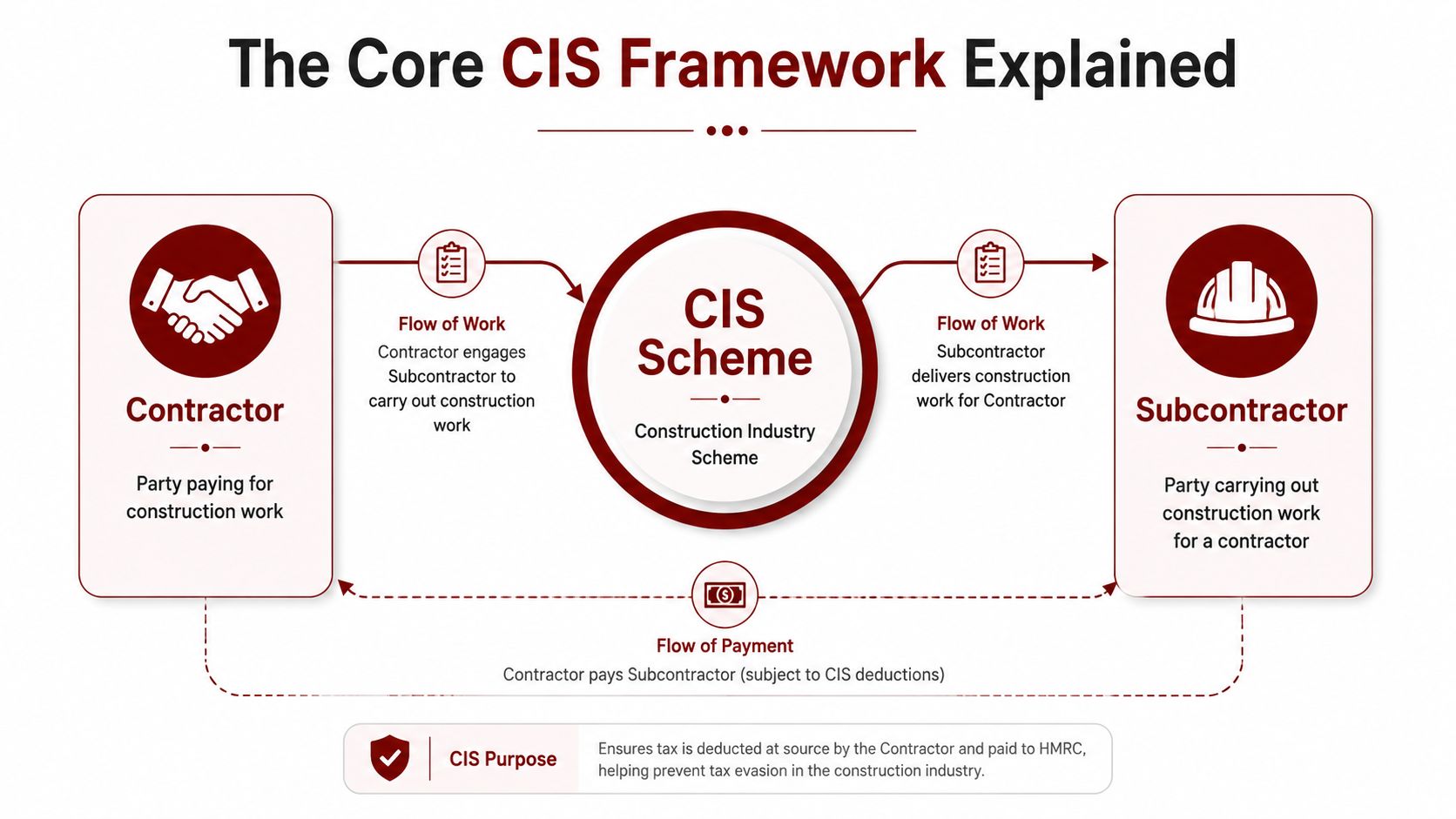

The Core CIS Framework Explained

CIS makes more sense once you stop treating the words as jargon and look at the roles.

A contractor is the party paying for construction work. A subcontractor is the party carrying out that work for the contractor. In real life, one business can be both at the same time. A company might act as a subcontractor on one site and hire its own subcontractors on another.

This is the mental model that usually helps. PAYE deals with employees. CIS deals with subcontractors in construction. In both cases, money is withheld before the person receiving payment settles their final tax position.

Who HMRC sees when money moves

When HMRC looks at a CIS payment chain, it wants to know three things:

- Who is paying: the contractor making payment for construction work.

- Who is being paid: the subcontractor receiving payment for labour and any other invoiced items.

- What has been withheld: the deduction taken from the part of the invoice that qualifies.

That last point matters because CIS is about withholding and reporting, not inventing a new tax bill. The deduction sits on account with HMRC until the subcontractor's wider tax position is worked out later.

Why the framework matters in day-to-day bookkeeping

Plenty of bookkeeping issues start because businesses mix CIS with payroll or ordinary purchase ledger processing. They're not the same thing.

Use a separate workflow for CIS subcontractor payments. Check status before paying. Record the labour element clearly. Keep the deduction statement aligned to the invoice. When those pieces are loose, reconciling the month becomes much harder than it needs to be.

If your payment process doesn't identify contractor, subcontractor and labour value clearly, the CIS problem starts before the invoice is approved.

Understanding Your CIS Deduction Rate

A common CIS mistake starts like this. A contractor gets told, “I'm registered,” pays the invoice, and assumes 20% applies. HMRC later says the subcontractor was never verified for that payment, so the wrong rate was used and the contractor is left cleaning it up.

The rate comes from HMRC status, not from what appears on the invoice or what the subcontractor says over the phone.

The three rates in plain English

Use this as the working rule.

| Deduction Rate | Subcontractor Status | What It Means |

|---|---|---|

| 20% | Verified subcontractor | Standard CIS deduction taken on account of tax and National Insurance |

| 30% | Unverified subcontractor | Higher deduction used where HMRC verification has not confirmed the standard rate |

| 0% | Gross Payment Status holder | No CIS deduction is taken, but the payment still sits within CIS reporting rules |

HMRC sets these rates. The contractor applies the one returned through the subcontractor check or supported by current Gross Payment Status. HMRC's CIS guidance and subcontractor verification rules set that framework clearly, including when the higher rate must be used and when gross payment can apply (HMRC CIS guidance and HMRC verification guidance).

Registered is not the same as verified

This is the point that costs contractors and subcontractors real money.

A subcontractor can be registered with HMRC for CIS and still not be verified by you for this contract. Until you run that check, you do not have the rate you can safely apply. In practice, that means a contractor who assumes “registered” automatically means 20% can end up making the wrong deduction or exposing the business to a compliance problem.

The safe process is simple. Verify before the first payment. Keep the result. Match it to the subcontractor record in your accounts system, not to somebody's memory.

A UTR on a quote is not verification. A text message saying “I'm on CIS” is not verification. A previous job for another contractor is not verification either.

Gross Payment Status and the practical trade-off

Gross Payment Status gives the best cash flow because nothing is withheld under CIS. For established subcontractors with steady profits and good compliance records, that can make a real difference to working capital.

It also comes with conditions. HMRC expects the business to meet compliance tests and turnover tests before gross payment is granted, and it can withdraw that status if the business slips on returns or payments (HMRC Gross Payment Status guidance).

For some businesses, chasing gross status too early is the wrong priority. If invoices are inconsistent, materials are not separated from labour, or verification records are patchy, fix those first. A clean CIS process usually saves more money than rushing into an application the business is not ready to support.

If you want outside help checking status, records, and deduction setup, it can help to find tax consultancy solutions before small CIS errors turn into expensive ones.

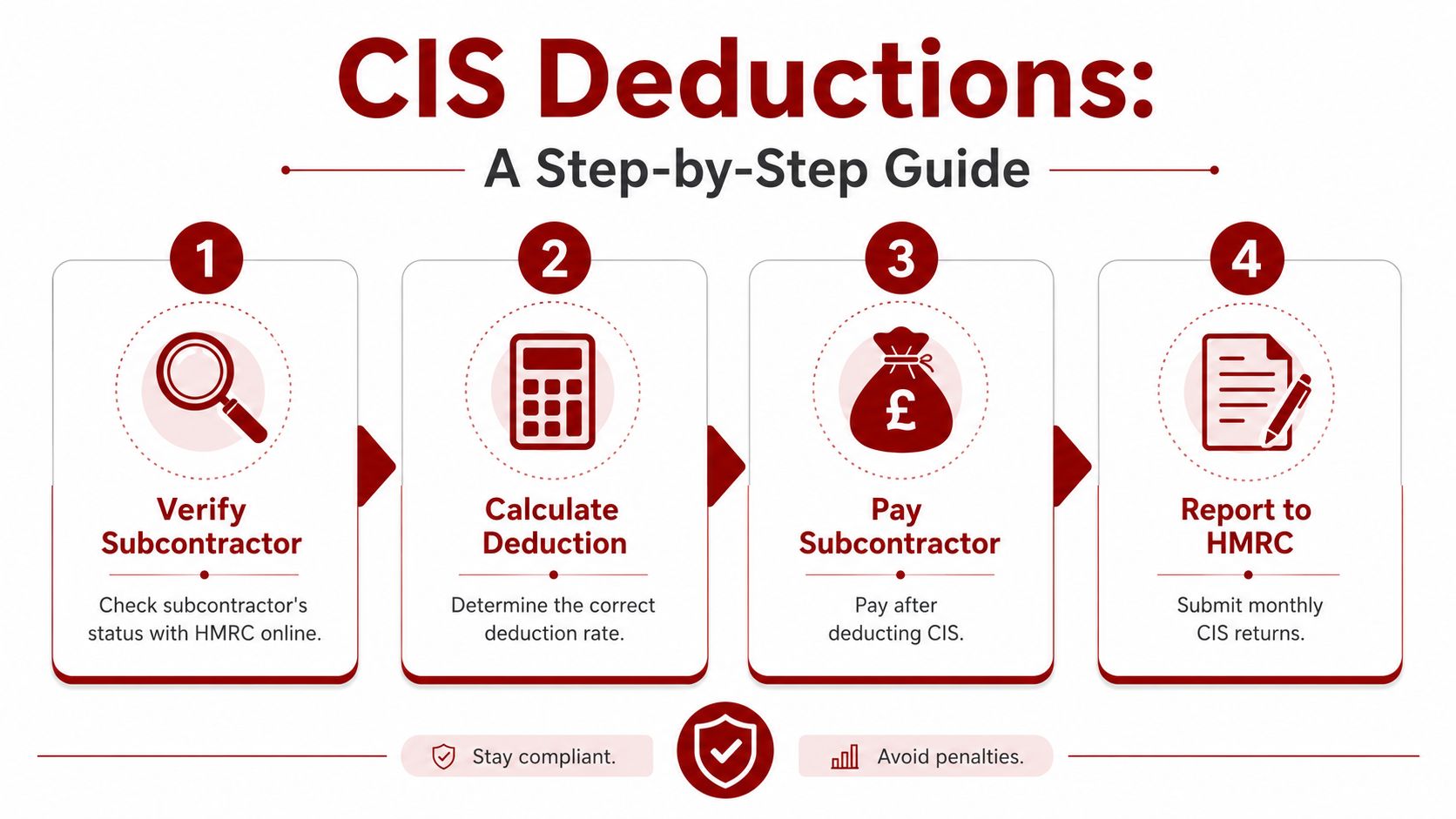

How to Calculate and Report CIS Deductions Correctly

A common site office mistake goes like this. The invoice comes in on Friday, someone pays the full labour and materials total into the software, and CIS is deducted from everything because no one stopped to check the breakdown. The subcontractor is then underpaid, the contractor's records are wrong, and month-end turns into a repair job.

The clean process is straightforward if the order is right.

The order that works in practice

Start with status. Use the subcontractor record that came back from HMRC and make sure the rate in your accounts system matches it. Contractors often get caught out by mixing up "registered" with "verified". A subcontractor may tell you they are registered for CIS, but your deduction rate depends on the verification result you hold for your own business relationship with them.

Then read the invoice line by line. CIS is charged on the part of the payment that covers construction labour. If the invoice bundles everything into one total, stop and get it corrected before you pay. A vague invoice is where over-deductions usually begin.

Once the invoice is clear, calculate the deduction on the labour element only. Exclude VAT. Exclude the cost of materials paid for by the subcontractor. Exclude qualifying plant hire charges where they are shown separately. Keep a note of exactly how you reached the CIS figure, because that note is what saves time when HMRC asks questions later.

After that, make the net payment, issue the payment and deduction statement, and feed the same figures into the monthly CIS return.

What goes into the deduction and what stays out

The practical test is simple. Ask what you are paying for.

If you are paying for the subcontractor's work, that amount is usually within CIS. If you are reimbursing materials, paying VAT, or paying separately identified non-labour costs, those amounts are usually outside the deduction calculation.

The expensive mistake is deducting CIS from the gross invoice total. It happens all the time on labour-and-materials invoices, especially when admin staff are working quickly and the invoice layout is poor. The result is predictable. The subcontractor loses cash flow, your records need correcting, and the relationship sours over what should have been a routine payment.

Use this working method every time:

- Start with the invoice total

- Remove VAT

- Remove materials clearly paid for by the subcontractor

- Remove separately identifiable non-labour items where they fall outside the CIS calculation

- Apply the CIS rate to the remaining labour amount

That single habit prevents a lot of avoidable overpayments and arguments. It also helps you improve construction cash flow controls because the right deduction means fewer disputes, fewer reversals, and fewer surprise shortfalls for both sides.

If your team needs specialist help around treatment, workflow, or more complex tax interactions across construction businesses, it can help to find tax consultancy solutions with sector experience rather than relying on generic bookkeeping advice.

Monthly reporting and records

Paying the subcontractor is only half the job. The return still has to match what you did in that tax month.

Submit the CIS return by the 19th of the following month and keep the support behind every figure you report. If no payments were made, check whether a nil return or an inactivity arrangement applies to your position with HMRC before you assume nothing needs filing. Rules in this area do change, so contractors should work from current HMRC guidance rather than old habits.

Keep these records together in one place:

- Verification result from HMRC

- Invoice showing the split between labour and non-labour items

- Calculation showing the deduction basis and rate used

- Payment and deduction statement issued to the subcontractor

- Return support for the CIS300 submission

Trying to rebuild all of that from bank transactions at month-end is where mistakes multiply. Good CIS control comes from getting the invoice right on the day you approve it, then carrying the same figures through to the return without rekeying or guesswork.

Worked Examples of CIS Deductions in Action

The maths becomes clearer when you see the same invoice handled two different ways.

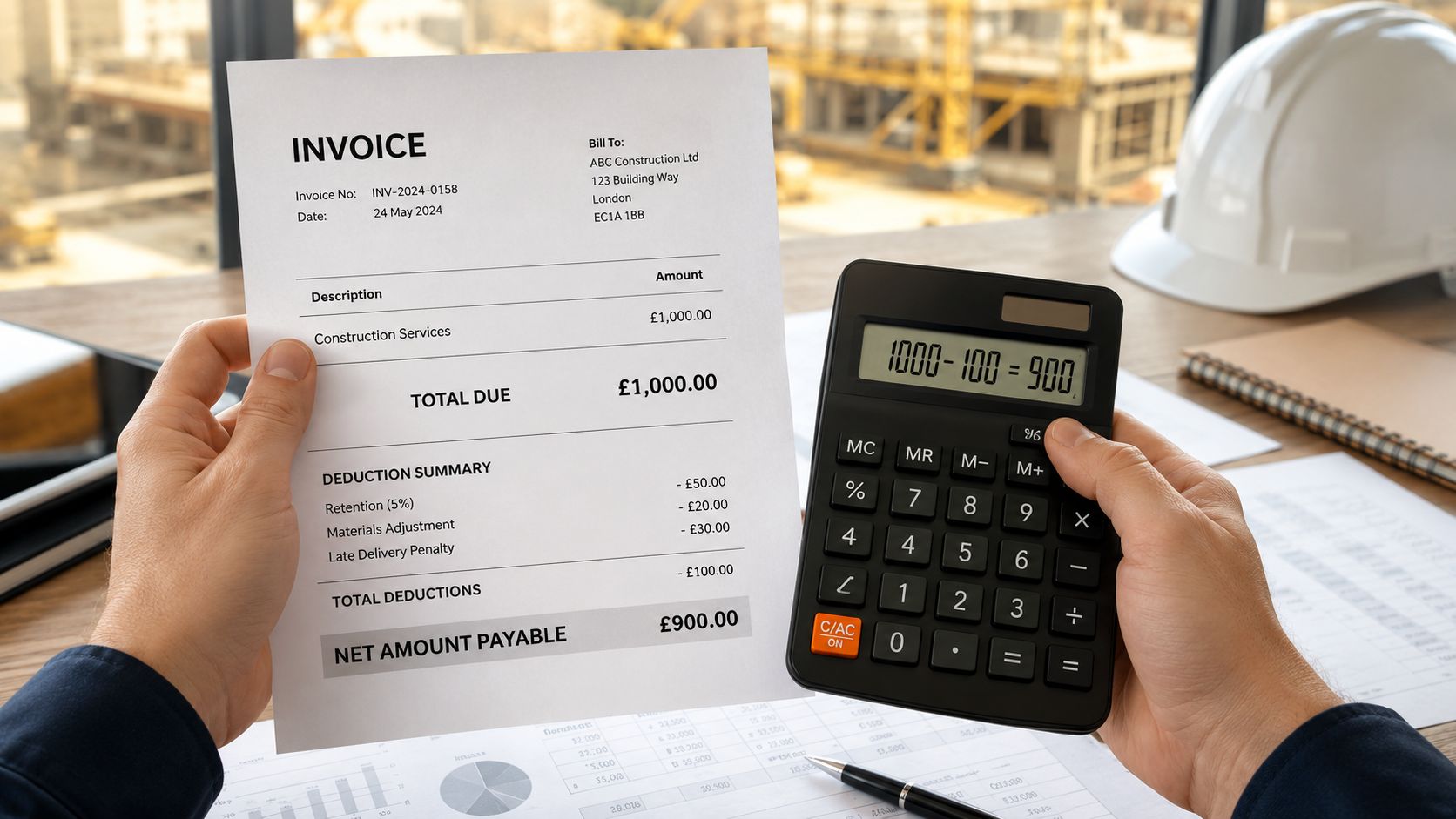

1. Correct calculation on labour only

A subcontractor sends an invoice for £1,000 made up of £600 labour and £400 materials. The subcontractor is on the 20% rate.

The contractor should calculate CIS on the £600 labour only.

- Labour subject to CIS: £600

- CIS rate: 20%

- Deduction: £120

- Payment to subcontractor: £880

That result is fair and compliant. The subcontractor still gets paid in full for materials, and only the labour portion is used for the deduction.

2. Incorrect calculation on the gross invoice

Now take the same invoice. Same labour. Same materials. Same subcontractor status.

The contractor makes the common mistake and applies 20% to the full £1,000 invoice total.

- Incorrect CIS base: £1,000

- CIS rate: 20%

- Incorrect deduction: £200

- Payment to subcontractor: £800

The immediate loss to the subcontractor is £80 compared with the correct treatment. That may not look huge on one invoice, but over a run of payments it puts avoidable pressure on working cash, fuel, wages, and supplier accounts.

The right invoice breakdown protects both sides. The contractor avoids a reporting mess. The subcontractor avoids funding HMRC with money that shouldn't have been withheld.

If cash movement is already tight, improving timing and payment controls matters just as much as getting the tax treatment right. This guide on how to improve cash flow is worth reading alongside your CIS process.

Reclaiming CIS How Subcontractors Get Their Money Back

Friday afternoon is when this usually lands. A subcontractor looks at months of CIS statements, sees money taken off every payment, and assumes it has gone for good. It has not. In practice, those deductions are advance payments against the tax and National Insurance bill that gets worked out later.

The refund process happens through the tax return. HMRC does not repay each deduction one by one just because a statement shows tax withheld. The subcontractor adds up the CIS deducted during the year, includes it on the Self Assessment return, and HMRC sets that credit against the final liability. If the deductions are higher than the bill, the balance can be refunded. This guide for CIS self-employed tax returns and refunds explains the route in more detail.

The trade-off is timing. A reclaim can fix the tax position, but it does not solve the cash squeeze caused by deductions that were too high in the first place.

That is why good records matter so much. If a contractor deducted CIS from materials, VAT, or other non-labour costs, the subcontractor may still recover the overpayment at year end, but only if the paperwork supports the claim. I have seen refunds delayed for a simple reason. The figures on the tax return did not tie back to the deduction statements.

Keep the process tight:

- Keep every CIS deduction statement. These are the starting point for the reclaim.

- Match statements to invoices and bank receipts. Check that the amount withheld fits the labour element, not the full invoice.

- Total deductions from actual records, not estimates. Guesswork causes amendments and delays.

- Raise errors early. If a contractor has used the wrong basis or the wrong status, sort it while the job is still current.

One point catches people out. Being registered for CIS is not the same as being handled correctly by the contractor. If the contractor gets verification or payment treatment wrong, the subcontractor can end up carrying an unnecessary cash shortfall until the reclaim is processed. That is one of the most expensive admin mistakes in construction because the tax may come back later, but wages, fuel, and suppliers need paying now.

The same discipline helps across specialist trades. For firms reviewing accounting for your plumbing business, CIS records should sit alongside job costing, materials tracking, and year-end tax files, not in a separate pile that only gets attention in January.

Avoid CIS Pitfalls and Take Control with Action Accountants

Most CIS trouble comes from a short list of avoidable habits. Payments are made before verification. Invoice totals are used instead of labour figures. Monthly filing is treated as admin that can wait. Then the business discovers the mistake when cash is tight or HMRC starts asking questions.

There's a wider cost too. Some subcontractors are pushed onto the wrong rate because contractor verification wasn't done properly. Others lose cash because deductions were taken from materials or VAT. Across the sector, unclaimed refunds and preventable overpayments still leave a lot of money sitting in the wrong place.

What good CIS support looks like

Good support isn't just someone filing forms after the event. It means putting a usable process in place:

- Verification built into onboarding

- Invoices reviewed for labour and non-labour split

- Deductions checked before payment leaves the bank

- Monthly CIS reporting prepared from clean records

- Year-end figures lined up so subcontractors reclaim what they're owed

That kind of setup matters whether you're a builder, electrician, groundworker, developer, or a trade business branching into new services. If you operate across related trades, practical guides on areas like accounting for your plumbing business can also help you tighten the wider financial controls around project work and subcontractor costs.

Why specialist construction accounting matters

Construction accounting is full of edge cases. One month you're hiring labour. The next month you're being paid as a subcontractor yourself. A generic accountant may understand tax in broad terms but still miss the operational reality of CIS.

For contractors and subcontractors who want sector-specific help with bookkeeping, compliance, and practical controls, construction accounting support is usually more useful than general business advice. The value is in reducing friction before mistakes become expensive.

If you're asking what is CIS deduction, the answer isn't just a percentage on an invoice. It's a process. When that process is right, payments run smoothly, monthly reporting stays manageable, and subcontractors don't end up funding avoidable overpayments.

If you want clear, practical help with CIS, speak to Action Accountants Limited. They support contractors and subcontractors in Colindale, North West London, and across the UK with CIS registration, bookkeeping, monthly returns, tax compliance, and reclaim work, so your systems stay compliant and your cash flow stays under control.