Self Assessment Deadline UK 2026: Key Dates & Penalties

Action Accountants •29 June 2026

You've done the work. The job's finished, the client's happy, the invoice is out, and your bank balance still looks wrong. Payroll is due on Friday. VAT is sitting in the background like a silent threat. Your supplier wants paying now, not when your client eventually gets round to it. If you're a contractor in Kingsbury, a café owner in Finchley, or running a small team in Colindale, that situation isn't unusual. It's ordinary business life in North West London.

The problem is that too many owners treat cash flow stress as bad luck. It usually isn't. It's a system problem. Weak invoicing, poor timing, sloppy forecasting, and tax money mixed into the main account will drain a business faster than most owners realise.

Table of Contents

- The Hidden Drain on Your Business Growth

- First Diagnose Your Cash Flow Leaks

- Build a Rolling Forecast That Actually Works

- Master Your Invoicing and Credit Control

- Align UK Tax and Supplier Payments Strategically

- Choose the Right Short-Term Funding Bridge

- Make Proactive Cash Flow Your Superpower

The Hidden Drain on Your Business Growth

A builder in Kingsbury lands a decent job. Materials go out, labour gets paid, fuel costs mount up, and the client says payment will follow “once accounts signs it off”. Meanwhile, rent, wages, software, insurance, and HMRC keep moving on schedule. That's how businesses get trapped. Not because they aren't selling, but because cash arrives too late.

A café in Finchley can look busy all week and still feel squeezed at month-end. A design studio in Colindale can show profit on paper while the director is moving money around just to keep the account steady. Profit and cash are not the same thing. Owners who ignore that usually learn the lesson the hard way.

The wider picture backs that up. Approximately 57% of UK small business owners have experienced cash flow problems, losing an average of £26,000 by forgoing projects due to insufficient access to capital, according to this summary of The State of Small Business Cash Flow. That's not a fringe issue. It affects nearly 6 in 10 SMEs.

Cash flow problems don't just create stress. They stop you taking on work you were capable of delivering.

That's why this matters. When cash is tight, you turn down jobs, delay hiring, postpone stock purchases, and make frightened decisions. Growth doesn't stall because demand disappears. It stalls because timing breaks the business.

If you've been firefighting for months, start by facing one uncomfortable point. Your cash position is probably being weakened by habits you've accepted as normal. Late invoicing. Loose terms. Tax money sitting in the trading account. Supplier payments sent too early. Those are the same sort of mistakes that sit behind the issues covered in these financial traps that quietly undermine small business owners.

First Diagnose Your Cash Flow Leaks

Don't start with a funding application. Start with your statements.

Most owners looking up how to improve cash flow jump straight to “how do I get more money in?” Fair question, wrong starting point. First find out where cash is already leaking. You can't fix what you haven't named.

Review the last three months properly

Pull the last three months of:

- Business bank statements

- Business credit card statements

- Merchant account reports

- Accounting software transaction lists from Xero, QuickBooks, or FreeAgent

- Any direct debit schedule you've ignored because it renews automatically

Print them or export them. Then mark every outgoing payment under simple headings.

| Category | What to include |

|---|---|

| Core operating costs | Rent, wages, utilities, essential software, insurance |

| Supplier spend | Materials, stock, subcontractors, outsourced services |

| Finance and tax | Loan repayments, VAT, PAYE, Corporation Tax set-asides |

| Admin drift | Bank charges, card fees, duplicated software, old subscriptions |

| Owner withdrawals | Dividends, drawings, ad hoc personal spending |

That last one matters more than people like to admit.

Look for the silent killers

Cash problems often come from small repeated drains, not one dramatic mistake. I regularly see businesses paying for tools nobody uses, software that overlaps, phone contracts on dead handsets, and supplier arrangements that no longer make sense.

Check for these first:

- Forgotten subscriptions. Old job management tools, design apps, booking software, unused Microsoft or Google licences.

- Poor supplier terms. You may be paying key suppliers in a week while your clients take a month.

- Avoidable bank and card fees. These can add up when nobody reviews merchant arrangements.

- Small recurring owner spend. Personal bits run through the company soon become a pattern.

- Underused stock or materials. Especially in retail, hospitality, and trades.

Practical rule: If a cost doesn't help you win work, deliver work, or stay compliant, challenge it.

Rank the problems in order

Don't produce a lovely spreadsheet and then do nothing with it. Pick the top three leaks and deal with them first.

Use this simple test:

- What leaves the account every month without scrutiny

- What's being paid earlier than necessary

- What would improve cash fastest if changed this week

One business in Edgware might find the problem is over-ordering stock. A subcontractor in Queensbury might discover the actual issue is client terms versus supplier timing. A consultant in Hendon might realise they're invoicing too late and tolerating nonsense from late payers.

Turn observations into actions

By the end of the audit, you should have a short list like this:

- Cancel or downgrade duplicate subscriptions

- Move non-urgent supplier payments closer to due date

- Separate tax money from daily trading cash

- Tighten payment terms for new clients

- Stop ad hoc withdrawals that blur business and personal spending

That's your baseline. Without it, every cash flow discussion turns into guesswork.

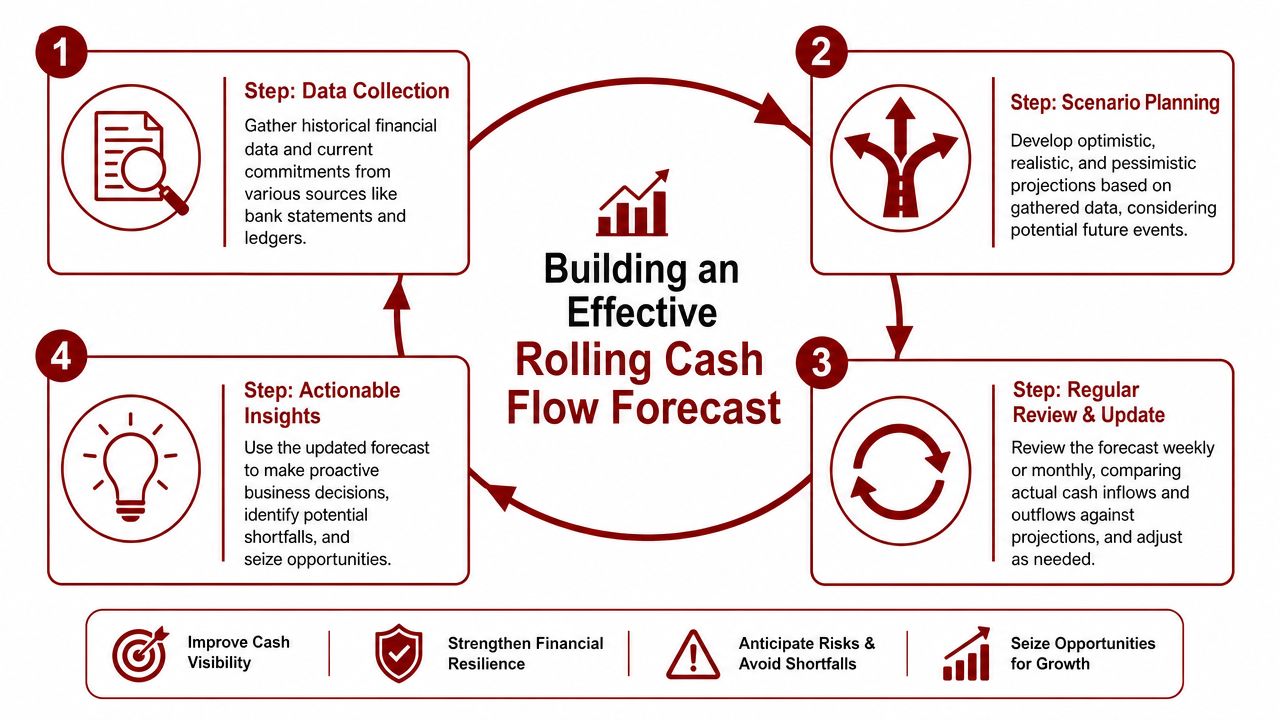

Build a Rolling Forecast That Actually Works

If you don't forecast cash weekly, you're driving by looking in the rear-view mirror. Annual budgets are fine for planning. They're useless for spotting a cash crunch two Tuesdays from now.

A rolling forecast is what gives you control. Not control in theory. Control over whether you can pay wages, whether a VAT bill will sting, and whether you can say yes to new work without creating a mess.

A good starting point is cash flow forecasting for small businesses, but the key is keeping it simple enough that you'll maintain it.

Use a 13 week view, not a yearly wish list

I prefer a 13-week rolling view because it's close enough to be real and long enough to show danger early. That also matches the practical recommendation in this UK SME cash flow guide, which says implementing a rolling 12-week cash flow forecast, updated weekly, allows UK SMEs to reduce average collection periods by 15–20% and prevent 30% of liquidity shortfalls. The same source notes that 60% of businesses improving forecasts also adopt automated invoice chasers.

The principle matters more than the exact layout. Keep the window short, update it every week, and work from real payment behaviour.

What goes into the sheet

Use Excel or Google Sheets if that's what you know. You do not need an elaborate finance system to start.

Your columns should be weeks. Your rows should include:

- Opening bank balance

- Expected customer receipts

- VAT refunds or other confirmed inflows

- Payroll

- Rent and regular overheads

- Supplier payments

- Tax payments

- Loan or finance repayments

- Owner drawings or dividends

- Closing bank balance

The important part is how you enter receipts. Don't put money in on invoice due date if that client always pays late. Use the actual pattern. If a customer says 30 days and usually pays in 40, forecast 40. If one main contractor pays in batches at odd times, reflect that reality.

The weekly discipline that makes it useful

Every week, update three things:

- What came in

- What went out

- What changed in the next 13 weeks

That means if a client delays approval, you move the receipt. If you win a job, add the likely inflow and the immediate cost attached to it. If your energy bill jumps or a tax date is approaching, plug it in now.

Forecasts fail when owners fill them in once, feel pleased, and never touch them again.

Keep separate bank accounts for operating cash, tax, and reserve cash. That way, your forecast reflects what's genuinely available to spend. If all the money sits in one account, people make bad decisions because the balance looks healthier than it is.

Here's a workable structure:

| Line item | Week 1 | Week 2 | Week 3 |

|---|---|---|---|

| Opening balance | |||

| Customer receipts | |||

| Other inflows | |||

| Payroll | |||

| Supplier payments | |||

| VAT and HMRC | |||

| Overheads | |||

| Net movement | |||

| Closing balance |

If you want to know how to improve cash flow in a practical way, start not with optimism, but with a live, ugly, honest forecast.

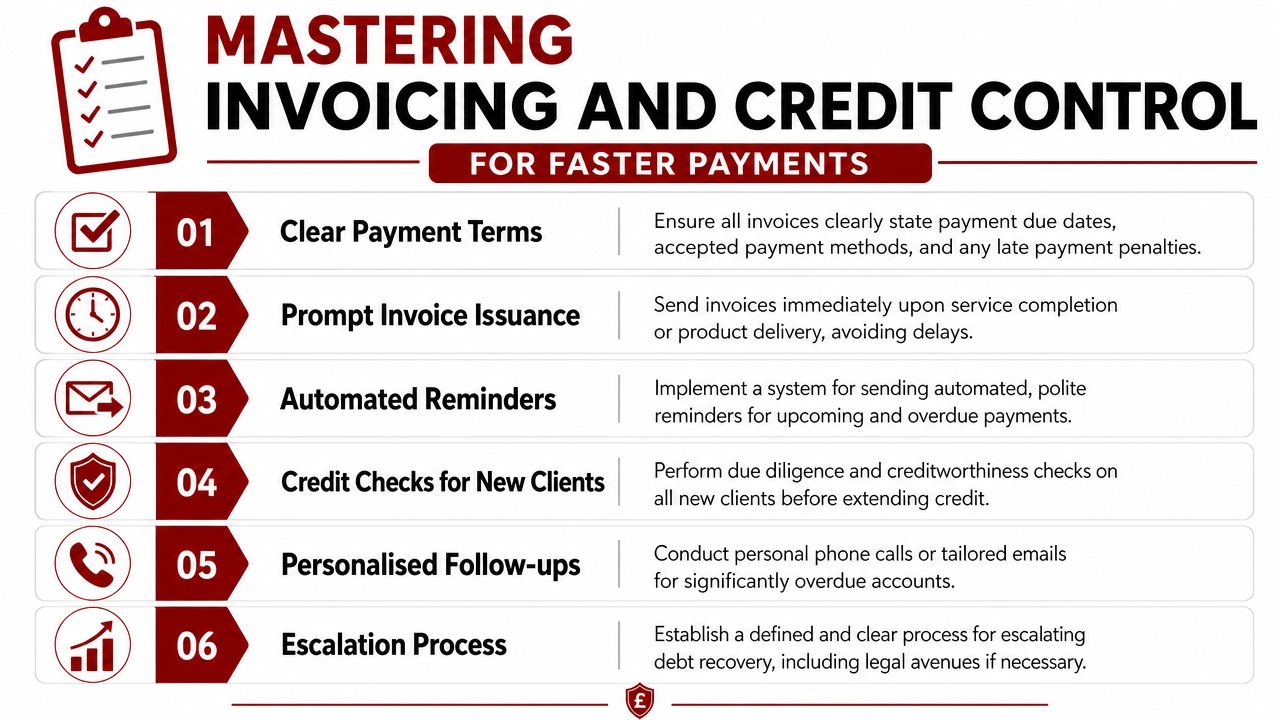

Master Your Invoicing and Credit Control

Most late payment problems are self-inflicted. Not all, but most.

Businesses finish the job, wait a few days, tweak the invoice, forget to attach a purchase order number, and then act surprised when payment drifts. That's not credit control. That's inviting delay.

Stop acting like a free lender

The rule is simple. Invoice immediately when the work is delivered, and don't offer longer terms unless there's a commercial reason you've thought through.

According to this guide on business cash flow strategy, strict credit control, including invoicing immediately upon delivery and demanding 30-day maximum terms, shortens receivables cycles by 18%. The same source says SMEs using automated reminder systems see success rates of 70%.

That should tell you something. Speed and discipline matter.

Use clear invoice wording. Include:

- The due date

- Accepted payment methods

- The purchase order reference if required

- A plain description of completed work

- Your bank details

- Who to contact about billing questions

If your admin is still patchy, proper software will help simplify your business invoicing and cut out the avoidable errors that slow payment.

A reminder sequence that works

Don't send one weak chase email on day 37 and hope for the best. Set a sequence.

A practical sequence looks like this:

- Before due date. Send a polite reminder that the invoice is due shortly, with the invoice attached again.

- On due date. Confirm payment is due today and ask for any issues to be flagged immediately.

- A few days overdue. Send a firmer note. Ask for a payment date, not a vague update.

- Further overdue. Pick up the phone. Speak to accounts, not just your contact on site or in marketing.

- Persistent delay. Escalate. Stop new work if needed. You're running a business, not a charity.

Here's a useful primer on the wider issue of late payments and process discipline:

Fix the process, not just the wording

A Colindale agency owner once told me the problem was “clients are slow”. Usually that's incomplete. Clients can be slow, but many businesses also make it easy for clients to pay late.

Check your internal process against this list:

- Job completion trigger. Who sends the invoice, and how soon after delivery?

- Approval bottlenecks. Is someone waiting for the director to review every invoice?

- Client onboarding. Did you confirm billing contact, PO rules, and terms before work started?

- Aged debt review. Does anyone check overdue accounts every week?

- Credit checks. Are you extending credit without judging risk first?

The strongest credit control system is boring. It runs on time, every time, without emotion.

If a customer regularly pushes payment past agreed terms, change the terms for future work. Deposit up front. Stage billing. Shorter intervals. No business owner in North West London should be financing bigger clients out of their own working capital.

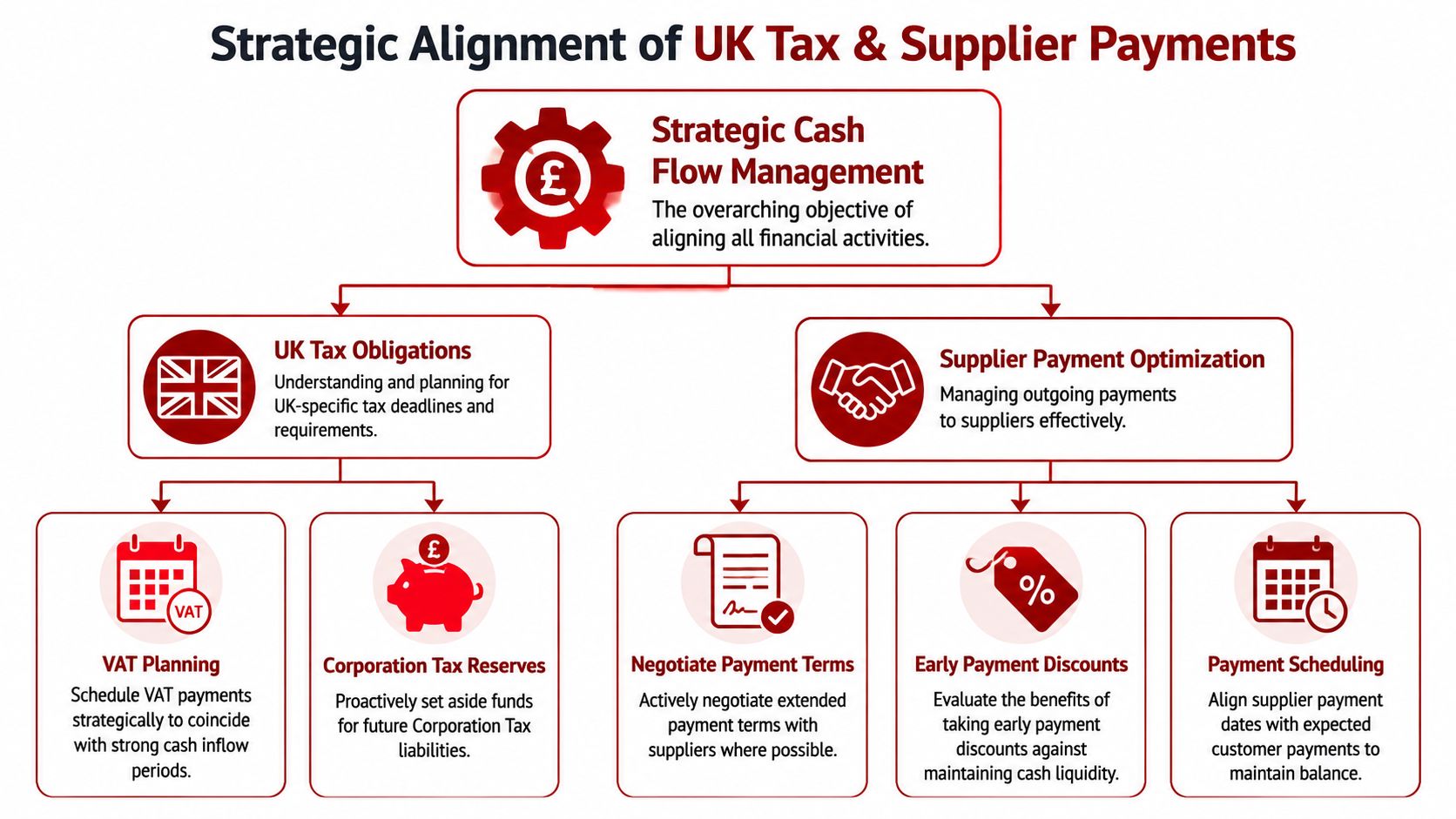

Align UK Tax and Supplier Payments Strategically

The typical advice in generic articles often proves insufficient. They tell you to “manage expenses better” and “plan for taxes” as if that's enough. It isn't. In the UK, timing around VAT, CIS, and supplier payments can create a predictable cash crunch if you don't build around it.

If you haven't already reviewed how HMRC scheduling affects working capital, it also helps to understand payments on account and their effect on tax timing.

Separate tax reality from trading cash

VAT is not your money. Neither is PAYE. Corporation Tax isn't a surprise either. Yet plenty of businesses leave all receipts in one current account, spend freely during busy months, and then panic when the quarter ends.

Do this instead:

- Open a separate tax account

- Move VAT and payroll tax amounts out of trading cash as receipts land

- Record HMRC due dates in the same weekly forecast as wages and rent

- Treat tax reserves as unavailable for day-to-day spending

That one change stops a lot of false confidence. Your bank balance may look lower, but it will be honest.

Construction firms need a CIS specific system

Construction businesses need tighter controls than most because the 20% CIS deduction directly affects what lands in the bank. According to this UK cash flow guidance for businesses, for UK construction firms, segmenting suppliers based on CIS obligations is critical, and mismanaging the 20% CIS deduction by failing to align it with client payment cycles is a leading cause of unexpected liquidity shortfalls.

A subcontractor in Queensbury might issue an invoice expecting one figure and then forget the practical effect of CIS deductions on real cash received. If supplier payments, fuel, wages, and materials are scheduled as though the gross amount will arrive, trouble follows.

For contractors, cash planning must reflect what clears the bank, not what sits on the invoice.

That means forecasting net inflows after CIS effect, not just contract value.

Segment suppliers instead of paying everyone the same way

Not every supplier deserves the same payment treatment.

Split them into groups:

| Supplier type | How to handle them |

|---|---|

| Critical suppliers | Protect relationship, negotiate consistent terms, avoid ad hoc promises |

| Flexible suppliers | Ask for longer terms where possible |

| One-off suppliers | Don't rush payment unless there's a clear benefit |

| Compliance-sensitive suppliers | Double check paperwork and invoice accuracy to avoid delays |

For a contractor, that might mean plant hire, materials, labour agencies, and one-off merchants all sit in different buckets. For a café, it might be coffee supplier, perishables, cleaning, and card terminal provider.

Negotiate from a position of organisation, not panic. If you're reliable and clear, many suppliers will work with you. The aim is simple. Don't let your business pay out in seven days while it collects in thirty or later.

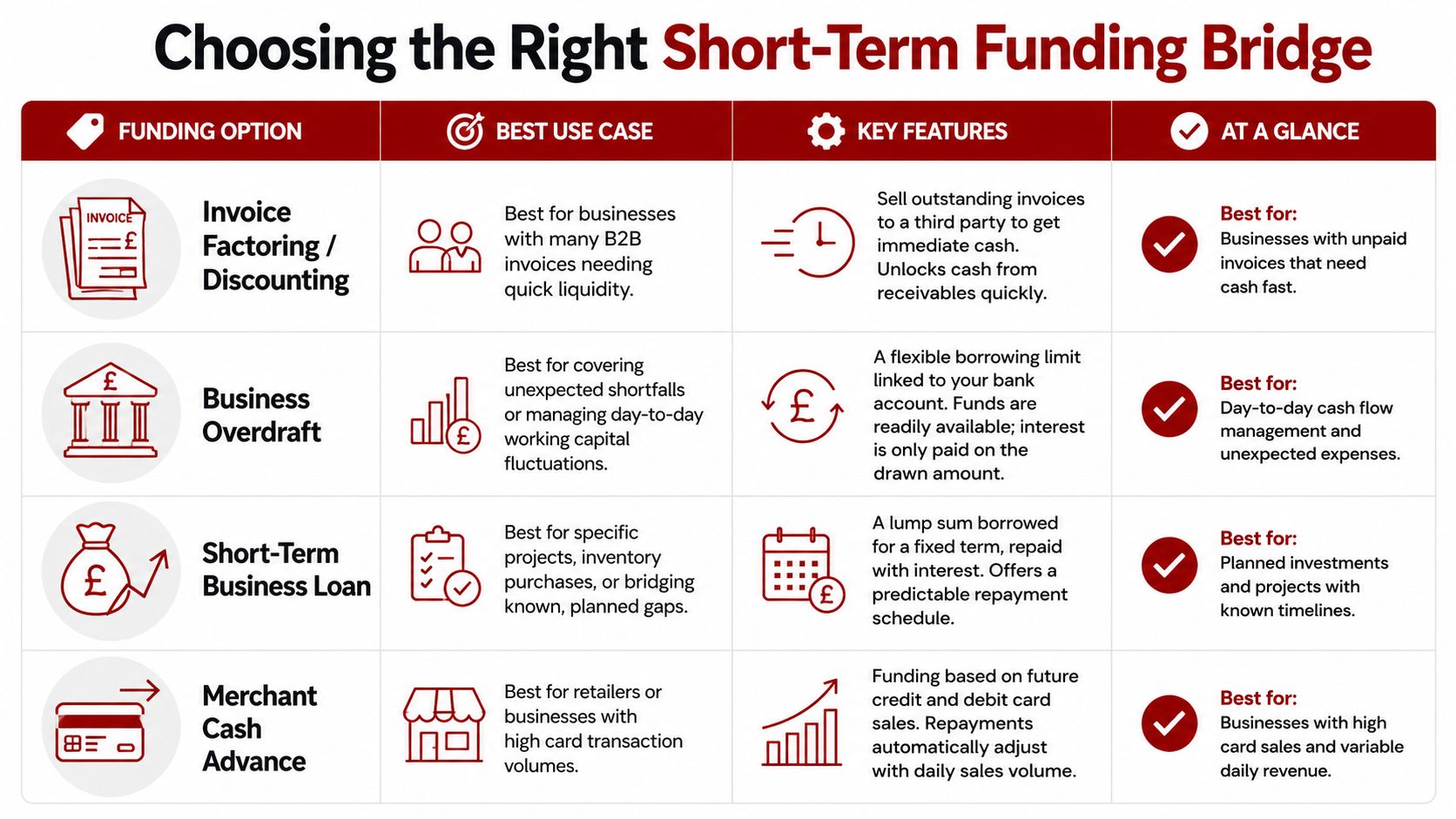

Choose the Right Short-Term Funding Bridge

Funding should bridge a gap you understand. It should not cover up a system you refuse to fix.

That distinction matters because, according to these UK SME finance figures, 41% of UK SMEs had recently used external finance by mid-2024, while many still prioritised other growth goals over operational efficiency. Too many firms borrow to patch messy internal processes instead of sorting collections, timing, and controls first.

When funding helps and when it makes things worse

Funding makes sense when:

- You have a temporary timing gap

- You're taking on profitable work and need short-term working capital

- You know how repayment will happen

- Your forecast shows the pinch point clearly

Funding makes things worse when:

- You can't explain where cash keeps going

- Your invoicing is still slow

- You're using debt to fund basic losses

- You're mixing business pressures with personal withdrawals

For newer businesses without much credit history, the practical challenge is access. The discussion in this article about bridging the cash flow gap is useful because it highlights how startups often struggle to access non-dilutive options like invoice-based finance when they lack collateral or trading record.

Which option suits which situation

Here's the blunt version.

| Option | Best use | Main caution |

|---|---|---|

| Invoice factoring or discounting | B2B firms with good invoices and slow-paying customers | Check control, fees, and client communication |

| Business overdraft | Short, uneven cash dips | Easy to lean on for too long |

| Business credit card | Small operating purchases and short float | Dangerous if balances roll month to month |

| Short-term loan | Planned gap or defined project need | Fixed repayments can strain weak cash flow |

If you're a director taking money in and out casually, sort that out before adding borrowing. A messy director's loan account and its implications can create extra problems you don't need.

The right funding tool supports a good system. It doesn't replace one.

Make Proactive Cash Flow Your Superpower

The businesses that stay calm aren't always the ones with the biggest turnover. They're the ones with better habits.

If you want to know how to improve cash flow, keep it disciplined. Diagnose the leaks. Build the rolling forecast. Tighten invoicing. Align tax and supplier timing. Use funding only when it bridges a planned gap. Do that consistently and cash flow stops feeling like a weekly ambush.

North West London businesses have enough to deal with already. Labour costs move, customers delay, HMRC deadlines don't care, and admin piles up quickly. You need systems that reduce surprises.

One overlooked fix is response speed. Missed calls often turn into delayed quotes, slower approvals, and slower cash. For contractor-led businesses in particular, tools like Mercateer's AI receptionist for contractors can help keep enquiries and client communication moving while you're on site or tied up elsewhere.

Good cash flow is not luck. It's the result of small controls done on time, every week.

If you build that discipline properly, cash becomes a tool. Not a constant source of stress.

If you want direct help building a cash flow system that fits your business, speak to Action Accountants Limited. They support startups, SMEs, contractors, landlords, and self-employed business owners across Colindale, Kingsbury, Queensbury, Edgware, Finchley, and the wider UK with practical accounting, forecasting, VAT, CIS, and advisory support that keeps cash under control.