Rental Income Allowable Expenses: Your 2026 HMRC Guide

Action Accountants •27 June 2026

January is when many landlords finally open the folder they've ignored all year. Bank statements are spread across the table. Invoices sit in email threads. A boiler was repaired, a window was replaced, the agent took fees, and there were a few trips to the property that never made it into a log. The question is always the same. What can be claimed against rental income, and what will HMRC push back on?

That's where most tax mistakes start. Not with aggressive planning, but with uncertainty. A landlord guesses that a payment “sounds business-related”, includes it, and only later discovers that HMRC treats repairs, replacements, finance costs, and improvements very differently.

Done properly, rental income allowable expenses are one of the simplest ways to improve the tax position of a property business while staying fully compliant. Done badly, they create avoidable tax, avoidable penalties, and a paper trail that doesn't stand up when HMRC asks questions.

Table of Contents

- Your Guide to Maximising Landlord Tax Deductions

- The Golden Rule Wholly and Exclusively

- A Complete List of Allowable Rental Expenses

- Navigating Mortgage Interest and Travel Costs

- Common Pitfalls and The Modern Equivalent Trap

- Flawless Recordkeeping and Worked Examples

- When to Partner with a Property Accountant

Your Guide to Maximising Landlord Tax Deductions

A familiar pattern plays out every tax season. A landlord remembers the obvious costs, rent collection fees, insurance, repairs. Then they hesitate over the messy items. Was the emergency plumber definitely revenue? Does mileage count if the trip included a stop at home? Was that replacement appliance still a repair once the new model had extra features?

Those grey areas matter far more than most landlords realise. Tax efficiency in a rental business usually isn't about exotic planning. It's about classifying ordinary spending correctly, keeping proof, and knowing when HMRC sees a cost as maintenance, replacement, private spending, or capital investment.

What good expense management looks like

Landlords who get this right tend to do three things consistently:

- They separate spending by type. Repairs, compliance costs, finance costs, travel, and larger property works don't belong in one undifferentiated list.

- They decide early whether to claim actual expenses or the property allowance. Waiting until filing week often leads to rushed choices.

- They keep support as they go. A receipt found months later is useful. A receipt matched to a bank payment and property note is far better.

If you're reviewing your wider strategy for how to boost property profit in 2026, expense discipline is usually one of the first areas worth tightening. For landlords building through refinancing and reinvestment, the operational side matters just as much as the deal itself, especially if you're following a growth model like the BRRRR property blueprint.

Practical rule: Don't start with “Can I claim this?” Start with “Why did the rental business pay for this?” That question usually gets you to the right answer faster.

The Golden Rule Wholly and Exclusively

The legal test sits at the centre of all rental expense claims. In the UK, a landlord can deduct costs from rental income only if they are wholly and exclusively for the purpose of the rental business under Section 34 of ITTOIA 2005, applied to property businesses via Section 272, as explained in this guide to allowable landlord expenses and the wholly and exclusively rule.

That phrase sounds technical, but the working principle is straightforward. If the expense exists because of the property business, it may be allowable. If it has a private purpose, or it improves the asset rather than maintaining it, the position changes quickly.

How the test works in real life

Take a simple analogy. Servicing a car keeps it running in its current state. Replacing the engine with a higher-performance one changes the asset. HMRC applies a similar line to rental property spending.

A letting agent fee exists because you let the property. That's a business cost. Insurance for the rental property protects the business asset. That's a business cost too. But if you install something materially better for reasons beyond ordinary replacement, you may have crossed into capital expenditure.

Mixed-use costs are another common issue. If your mobile phone is used partly for tenant calls and partly for personal use, you can only claim the business element. HMRC expects a fair and sensible apportionment, not a guess.

Revenue costs and capital costs

It helps to sort costs into two broad camps.

- Revenue expenses are day-to-day running costs tied to letting and management. These are the items landlords most often claim against rental income.

- Capital expenditure relates to improving, adding to, or substantially upgrading the property. These costs don't qualify as direct deductions from rental income under the normal expense rules.

A few examples make the distinction clearer:

- Repairing a leaking pipe usually points to revenue.

- Replacing worn roof tiles with matching materials often stays on the revenue side.

- Adding a new bathroom where there wasn't one before points to capital.

- Upgrading a basic finish purely for appearance and uplift often points to capital as well.

Later in this guide, the replacement issue becomes more nuanced. That's where many landlords slip. The basic rule, though, is simple enough to remember.

If the spending preserves the property for letting, it is often revenue. If it improves or enhances the asset, it is often capital.

For landlords, that single distinction often matters more than any checklist.

A short explainer can help if you want a visual walkthrough before classifying your own costs:

A Complete List of Allowable Rental Expenses

A landlord replaces a tired fridge with a larger American-style model, books it as a straightforward replacement, and assumes the full cost is deductible. That is exactly the sort of claim HMRC queries. The routine expenses are usually easy. The expensive mistakes often sit inside items that look routine but contain an element of improvement.

Start with the costs that arise because the property is being let and managed. HMRC's property income manual on allowable expenses sets the basic approach, and in practice landlords usually review these categories first:

- Letting agent and management fees

Tenant-find fees, rent collection charges, inventory fees, and full management fees are usually allowable if they relate to the let property. - Repairs and maintenance

Boiler repairs, roof patching, repainting between tenancies, replacing broken locks, and similar works are commonly allowable where they restore the property to a usable condition rather than improve it. - Landlord insurance

Buildings, contents for furnished lets, rent guarantee, and landlord liability cover are generally allowable where the policy is for the rental business. - Ground rent and service charges

These are often allowable where they are the landlord's cost of holding and letting the property. Leasehold landlords should still separate normal charges from one-off major works demands that may need closer review. If that area causes problems in your books, this guide to service charge accounting for UK landlords will help. - Council tax during void periods

Where the liability sits with the landlord, the cost is usually deductible as part of running the property business. - Utilities paid by the landlord

Gas, electricity, water, broadband, or similar bills can be claimed where the tenancy agreement makes them the landlord's expense. - Business travel

Visits for inspections, maintenance checks, meetings with agents, and other rental-business journeys may be allowable. HMRC explains the basis in its guidance on expenses if you use cash basis. Keep a mileage log or clear records of actual travel costs. - Pre-letting expenses

Some costs incurred before the first tenant moves in can still qualify. HMRC's guidance on pre-letting expenses allows relief where the expense was incurred within seven years before the rental business started and would have been allowable if incurred later.

For a broader checklist, this summary of 2025 tax deductions for landlords is a useful comparison point. The UK tax result still depends on HMRC's rules and on how the invoice is described.

Allowable vs disallowed expenses at a glance

| Expense Type | Allowable (Revenue) | Disallowed (Capital/Personal) |

|---|---|---|

| Letting agent fees | Yes, if incurred for the rental business | No if unrelated to the let property |

| Repairs to existing items | Usually yes | No if the work is actually an improvement |

| Landlord insurance | Usually yes | No for personal insurance unrelated to letting |

| Service charges and ground rent | Usually yes | No if the cost is private or not linked to the rental business |

| Council tax in voids | Usually yes where landlord pays it | No if it is not the landlord's expense |

| Utilities paid by landlord | Usually yes | No for personal household costs |

| Replacement domestic items | Often yes, but only up to the cost of a modern equivalent | Extra cost for an upgrade is not deductible as revenue |

| New bathroom where none existed before | No | Capital expenditure |

| Personal travel | No | Personal expenditure |

| Residential mortgage finance costs | Not deducted as a revenue expense | Relief is handled separately, not as a direct deduction |

The replacement categories landlords misread

The trap is not usually the obvious capital project. It is the invoice that mixes repair, replacement, and upgrade into one figure.

Replacing a worn-out item with the nearest current equivalent can still be allowable. Replacing it with something materially better can push part of the cost out of revenue. HMRC deals with this in its manual on replacement of domestic items and related property income guidance. In plain terms, the deductible amount is restricted to the cost of the modern equivalent, plus any incidental disposal or installation costs, less any proceeds from the old item.

That matters in real jobs. A standard hob replaced with a premium induction range is not a full repair claim just because an old hob came out. A basic carpet replaced with hardwood flooring can trigger the same issue. The landlord still gets relief for the replacement element, but the uplift attributable to the better specification is usually not a normal rental expense.

When the property allowance may suit you better

Some landlords are better off keeping it simple. GOV.UK's property allowance guidance explains that a landlord with low rental receipts may choose the allowance instead of claiming actual expenses.

The decision is arithmetic, not preference. If actual allowable costs are under the allowance, the allowance can produce a better result with less admin. If real expenses are higher, claiming the actual figures usually saves more tax. That is especially true for landlords with agent fees, insurance, service charges, and regular repairs showing up throughout the year.

Navigating Mortgage Interest and Travel Costs

These are two areas landlords routinely misunderstand, but for different reasons. Travel is often under-claimed because people don't keep records. Mortgage interest is often over-claimed because people still think it reduces rental profit in the old way.

Why mortgage interest catches landlords out

For UK residential properties, finance costs such as mortgage interest are no longer deducted from rental income in the normal sense. Instead, landlords receive a basic rate tax credit of 20% on those finance costs, a rule fully effective since April 2020, as explained in this overview of mortgage interest relief restrictions for landlords.

This changes the tax logic completely. A landlord might have significant interest payments, but those costs do not reduce rental profit pound-for-pound before tax in the way many still assume. The rental profit is worked out after other allowable expenses, excluding finance costs, and the tax credit is applied under the finance cost rules instead.

That matters most where borrowing is heavy. The cash cost feels real because it is real, but the tax treatment is narrower than many first-time landlords expect.

Don't treat mortgage interest like repairs, insurance, or agent fees. It sits in its own box.

Travel claims that actually stand up

Travel is simpler, but only if the records are clean. The question is whether the journey was for the rental business. Going to inspect storm damage, meet a contractor, collect keys from an agent, or check work after a tenant leaves can all point to business use.

The mileage method is often the easiest route for small landlords because it avoids trying to reconstruct fuel receipts months later. To make that work properly, keep a log showing:

- Date of journey

- Start and end location

- Reason for the trip

- Miles travelled

- Which property the trip related to

What doesn't work is rebuilding a mileage claim from memory at year end. It may still be partly right, but it won't be persuasive if queried.

A practical way to think about travel is this:

| Travel type | Treatment |

|---|---|

| Visiting the property to inspect repair work | Usually business-related |

| Meeting a letting agent about tenants | Usually business-related |

| Driving past the property while on a personal trip | Usually not a clean business claim |

| Combining business and private reasons in one trip | Apportion carefully and only claim the business part |

That same discipline applies to parking, train fares, and other travel costs if you choose not to use mileage. The principle remains the same. Keep it connected to the rental activity, and keep proof.

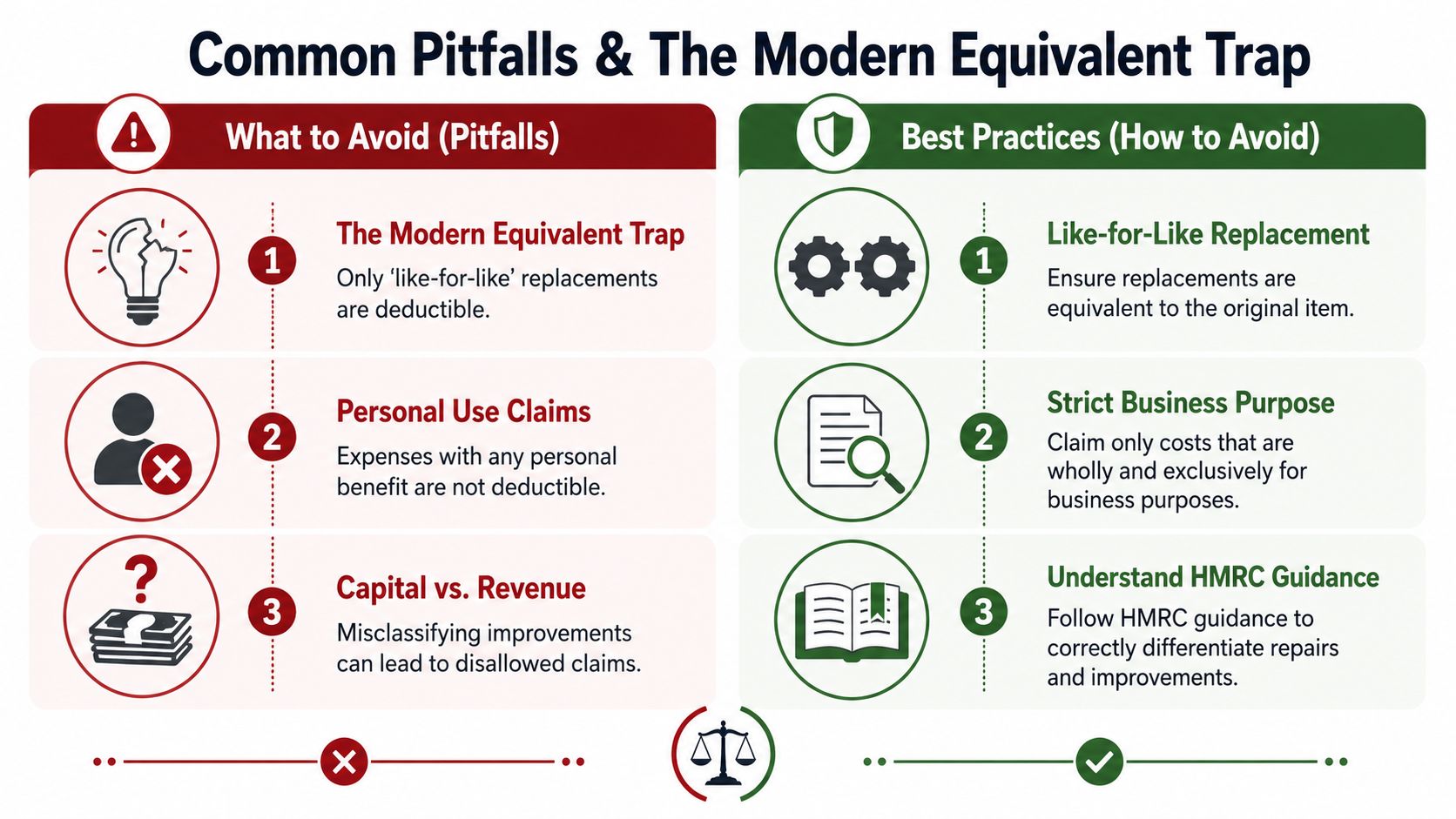

Common Pitfalls and The Modern Equivalent Trap

A landlord swaps a failed basic oven for a smart model with pyrolytic cleaning, app controls, and a higher-spec finish. The invoice says “replacement”. The tax return claims the full cost. That is exactly how the modern equivalent trap starts.

The trap matters because HMRC does allow a deduction for replacing domestic items with a reasonable modern equivalent, but that rule is narrower than many landlords assume. The fact that an item is newer, better, or more expensive does not make it revenue expenditure. HMRC's guidance on working out rental income and replacement items is the starting point, but the primary risk sits in how the facts are presented and evidenced.

Where replacement stops and improvement starts

Modern equivalent means the nearest current-day substitute for what the property already had and needed. It does not mean taking the opportunity to improve the asset and then calling the whole spend a repair or replacement.

In practice, I look at three questions:

- What was there before?

A worn standard kitchen, budget carpet, or ordinary combi boiler sets the baseline. - What was bought instead?

If the replacement matches current market standard for a similar item, the claim is usually easier to defend. - Why was it chosen?

If the answer is better durability, legal compliance, or because the old model no longer exists, that supports replacement treatment. If the answer is to create a premium finish or push up rents through a higher specification, that points toward improvement.

A more energy-efficient boiler can still be a replacement if it performs the same job and reflects what is now commonly available. Quartz worktops replacing old laminate are harder to defend if the property previously sat at a standard finish and the new surface was chosen to upgrade the kitchen.

The clean test is simple. A replacement keeps the rental business running at broadly the same standard. An improvement gives you something better than the property had before.

Why this catches landlords out

The modern equivalent trap is one of the highest-risk areas because the facts often sit in a grey zone. Builders and suppliers use commercial language, not tax language. “Upgrade”, “refit”, “premium finish”, and “full refurbishment” can all appear on an invoice where only part of the job is allowable as a revenue expense.

That creates two problems. First, the tax treatment may be wrong. Second, the paperwork may tell the wrong story even where part of the claim is valid.

A landlord who replaces damaged cabinet doors, retouches plaster, and installs higher-spec appliances under one invoice headed “kitchen upgrade” should not claim the whole amount as repairs. Split the invoice. Identify the repair element, the replacement element, and the capital improvement element. If the contractor has not done that, ask for a revised breakdown before filing the return.

Landlords with furnished or short-stay properties need to be especially careful because item replacement happens more often and specification creep is common. Different rules and planning points can also apply, so check our guide to furnished holiday let tax rules and deductions if that is your setup.

Other mistakes that trigger HMRC challenges

The modern equivalent trap is the headline issue here, but it is rarely the only one in a disputed return.

- Mixed-use costs claimed in full

If an expense has a private element, only the rental share is deductible. Phones, broadband, software, and travel are common problem areas. - Pre-letting costs claimed without checking the timing rules

Some expenses incurred before the first tenant moves in can qualify. Others do not. The key question is whether the cost would have been allowable if incurred once the rental business had started. - Bundling everything into “repairs”

Large projects often include patch repairs, replacements, and improvements in one job. Treating the whole invoice as revenue usually overstates the deduction. - Cosmetic uplift dressed up as maintenance

Replacing tired but usable fittings with premium alternatives often feels like ordinary upkeep. For tax, it usually is not.

One practical step prevents a lot of trouble. Review the wording on invoices before you pay them. “Replace damaged sink with standard equivalent” is easier to support than “upgrade bathroom finish”. HMRC will look at the substance, but poor wording gives them a reason to ask harder questions.

Flawless Recordkeeping and Worked Examples

A landlord buys a replacement cooker, keeps the card receipt, and assumes that is enough. Six months later, HMRC asks what was replaced, why the new model cost more, and whether any part of the spend was an improvement rather than a like-for-like replacement. That is where weak records turn an allowable claim into a disallowed one.

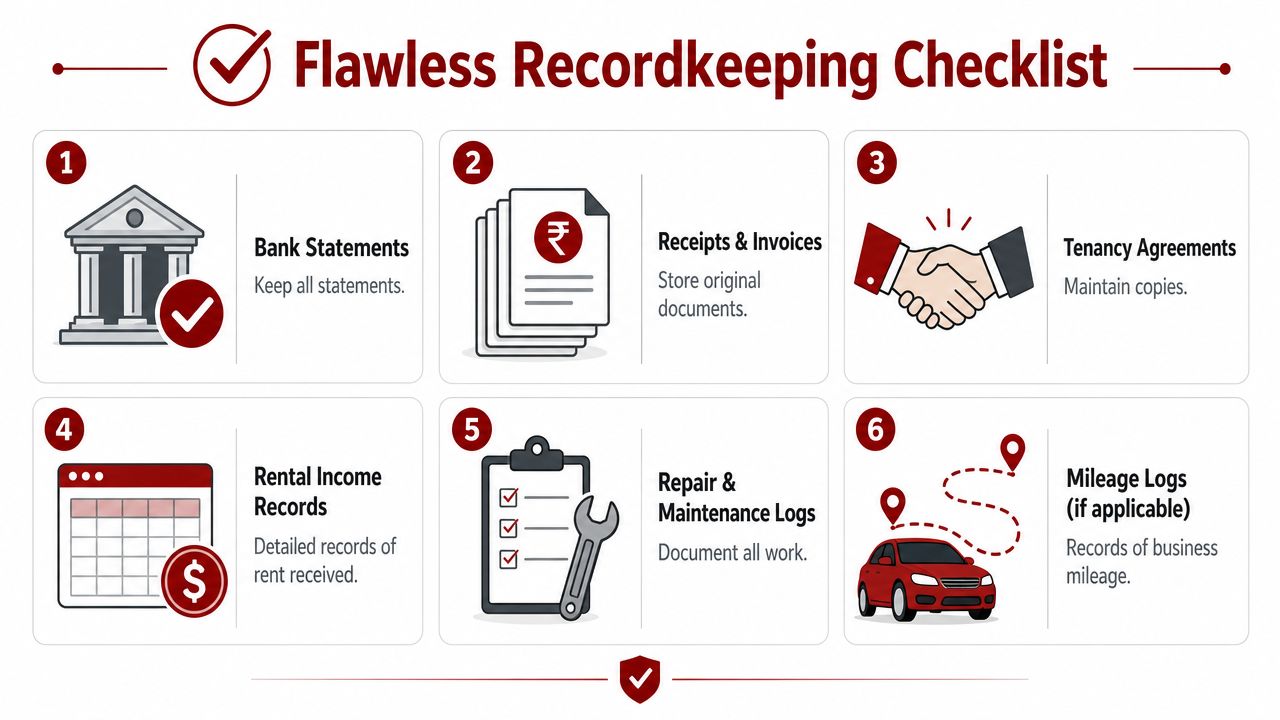

For rental property, records need to do more than prove you paid. They need to show what the cost related to, which property it belonged to, and why the tax treatment is right. HMRC expects landlords to keep records such as receipts, invoices, bank statements, mileage logs, and tenancy documents for years after the filing deadline. If you cannot trace an expense back to the rental business, you are relying on memory. That is a poor position in an enquiry.

The records HMRC expects

Keep one file for each property, whether digital or paper, and make sure each document answers three questions. What was bought. Why it was needed. Whether it was a repair, a replacement, a finance cost, or something capital.

The practical records pack usually includes:

- Bank statements showing the payment leaving your account

- Invoices and receipts describing the item or work carried out

- Letting agent statements supporting fees and rent received

- Tenancy agreements showing the property was let or available to let

- Mortgage statements to separate finance costs from other expenses

- Mileage logs if you claim business travel

- Before-and-after notes or photos for replacement items, especially where HMRC could argue there was an upgrade

That last point matters more than many landlords realise. The modern equivalent trap often sits in ordinary household replacements. If an old basic hob is replaced with the closest current model, that can still be allowable. If the invoice says “kitchen upgrade” or bundles in better specification features without showing the equivalent cost, you may lose part of the deduction. Good records protect the claim before the question is ever asked.

Clean bookkeeping also makes the wider tax position easier to manage. Rising rental profit often brings surprise payments on account for landlords, and poor records make those estimates harder to check. Some landlords also move from ad hoc spreadsheets to monthly bookkeeping services once the admin starts swallowing time that should be spent reviewing the property itself.

Records defend the claim and improve the claim.

Two worked examples

Example one. A landlord collects rent and pays agent fees, insurance, repair costs, and council tax during a void period. Those revenue expenses go into the property pages of the Self Assessment return. Mortgage interest is tracked separately because it does not reduce rental profit in the same way as repairs or agent fees.

The working matters here. One column for rent. One for revenue expenses. One for finance costs. One for anything that might be capital. That simple split prevents a lot of avoidable errors at year end.

Example two. A landlord replaces a broken freestanding fridge with a current model because the discontinued original is no longer sold. The new fridge costs more than the old one did years ago, but it performs the same basic function and sits in the same rental kitchen. The claim can still be allowable as a replacement, but the file should keep the purchase invoice, a note that the old unit failed, and evidence that the new model was the nearest current equivalent rather than a lifestyle upgrade.

If the landlord instead installs an American-style fridge freezer with extra storage, ice dispenser, and a reworked kitchen layout, the position changes. Part or all of that extra spend may be capital, not revenue. This is the point many general guides miss. HMRC does not just look at whether something was replaced. It looks at whether the landlord went beyond the modern equivalent and improved the asset.

Mixed-use expenses need the same discipline. If a mobile phone is used for tenant calls and private use, claim the business proportion and keep the method used to calculate it on file. A sensible apportionment supported by records is far easier to defend than a rough guess made after year end.

When to Partner with a Property Accountant

A landlord often calls after HMRC has opened an enquiry into what looked like a routine replacement. The figures are usually not the actual problem. The problem is that the file does not show why the new item was the nearest modern equivalent rather than an improvement, or why a cost posted as a repair was not capital. That is the point where DIY accounting stops saving money.

Some landlords can handle their own records well if the portfolio is simple and the bookkeeping is tidy. The pressure point comes when judgement matters more than data entry. Property tax is full of areas where the treatment depends on facts, timing, and evidence. Replacement items are a good example. A general expense checklist will not tell you whether HMRC is likely to accept a higher-cost replacement as revenue, partly disallow it as improvement, or ask for more support.

Professional input usually makes sense if your position includes:

- Non-resident landlord issues, where reporting and withholding rules affect how UK rental income is handled

- Capital Gains Tax planning after a sale, especially where there has been previous occupation, transfers between spouses, or several properties

- Portfolio restructuring, such as reviewing company ownership, incorporation, or how future purchases should be held

- Mixed property activities, where one record set covers standard lets, short lets, or other arrangements with different tax treatment

- Weak bookkeeping history, where earlier returns may need correction or the current year has gaps

- Frequent replacement claims, particularly where the new item costs more because the old model is obsolete and you need to prove it was the closest modern equivalent, not an upgrade

That last point is where I see avoidable errors most often. Landlords replace a worn bathroom suite, kitchen appliance, or flooring with what is sold today, then assume the full cost is automatically deductible. Sometimes it is. Sometimes part of the spend relates to improvement, better specification, or altered layout. Getting that split wrong can mean an overstated expense, a weaker tax return, and a difficult conversation with HMRC later.

A good property accountant does more than complete the return. They review grey areas before filing, classify costs with a defensible basis, and tell you when a claim is too weak to include. They also help set up records properly so next year's return is faster and cleaner.

If you are comparing outsourced support models more generally, even a service overview like monthly bookkeeping services shows the value of regular bookkeeping over trying to rebuild a year of transactions from bank statements and receipts.

If you want that kind of practical, fast, and grounded support for your property business, Action Accountants Limited can help. They support landlords across North West London and the wider UK with bookkeeping, Self-Assessment, property tax compliance, and structuring advice, so you can claim correctly, document replacement items properly, and avoid expensive HMRC disallowances.