FRS 102 Changes: A UK SME Guide for 2026

Action Accountants •9 July 2026

You've probably already had the email, the software alert, or the passing comment from your bookkeeper: FRS 102 is changing. You know it matters, but you're not sure whether it's a paperwork issue, a software issue, or something that could hit profit, net assets, and conversations with the bank.

For many small business owners, that uncertainty is the main problem. You don't need another technical summary full of accounting jargon. You need to know what's changing, where the risk sits, and what to do now so you're not fixing it under deadline pressure.

The upcoming FRS 102 changes are not cosmetic. They alter how many UK businesses recognise revenue, account for leases, and present key figures in their financial statements. If you run a startup, contractor business, property company, or growing SME, this can affect reported performance even when your cash hasn't changed.

Table of Contents

- Are You Ready for the Biggest UK Accounting Shake-Up in a Decade

- Decoding the Core FRS 102 Amendments for 2026

- Why These Changes Matter to Your Business

- Your Critical FRS 102 Transition Timeline

- Real-World Examples of the New Accounting

- Your FRS 102 Compliance Action Plan

- How Action Accountants Can Secure Your Transition

Are You Ready for the Biggest UK Accounting Shake-Up in a Decade

If your business prepares accounts under FRS 102, this is one of those moments where waiting is a mistake. Owners often assume accounting standards only matter to auditors and finance teams. That's wrong. These changes affect how your business looks on paper, and that feeds directly into lending decisions, investor confidence, tax planning conversations, and sale readiness.

The biggest risk isn't just technical non-compliance. It's walking into your next year-end with contracts, leases, and reporting systems that were built for old rules. That's how businesses end up with last-minute adjustments, awkward board conversations, and accounts that need more work than expected.

Why this is more than an accounting tidy-up

FRS 102 sits underneath a large part of UK SME reporting. When that framework shifts, the knock-on effect spreads fast. Revenue may no longer follow your invoicing routine. Lease commitments that used to sit unrecognised in the background may need to appear on the balance sheet. Disclosures that felt light-touch may become more involved.

That means the frs 102 changes aren't just for finance directors. They matter to founders signing customer contracts, landlords agreeing lease terms, and construction firms managing staged jobs.

Practical rule: If a change affects when profit appears or where liabilities sit, it's a business issue, not just an accounting issue.

The cost of leaving it too late

Busy owners usually delay this work for understandable reasons. Trading comes first. Client delivery comes first. Payroll, VAT, and cash flow come first. But these changes need contract review, judgement, and system preparation. None of that is quick if you start close to year-end.

Take a blunt view. If your business has multi-part customer contracts, office or equipment leases, group relationships, or external finance, you should assume there's work to do. The sensible approach is to assess now, decide early, and avoid surprises later.

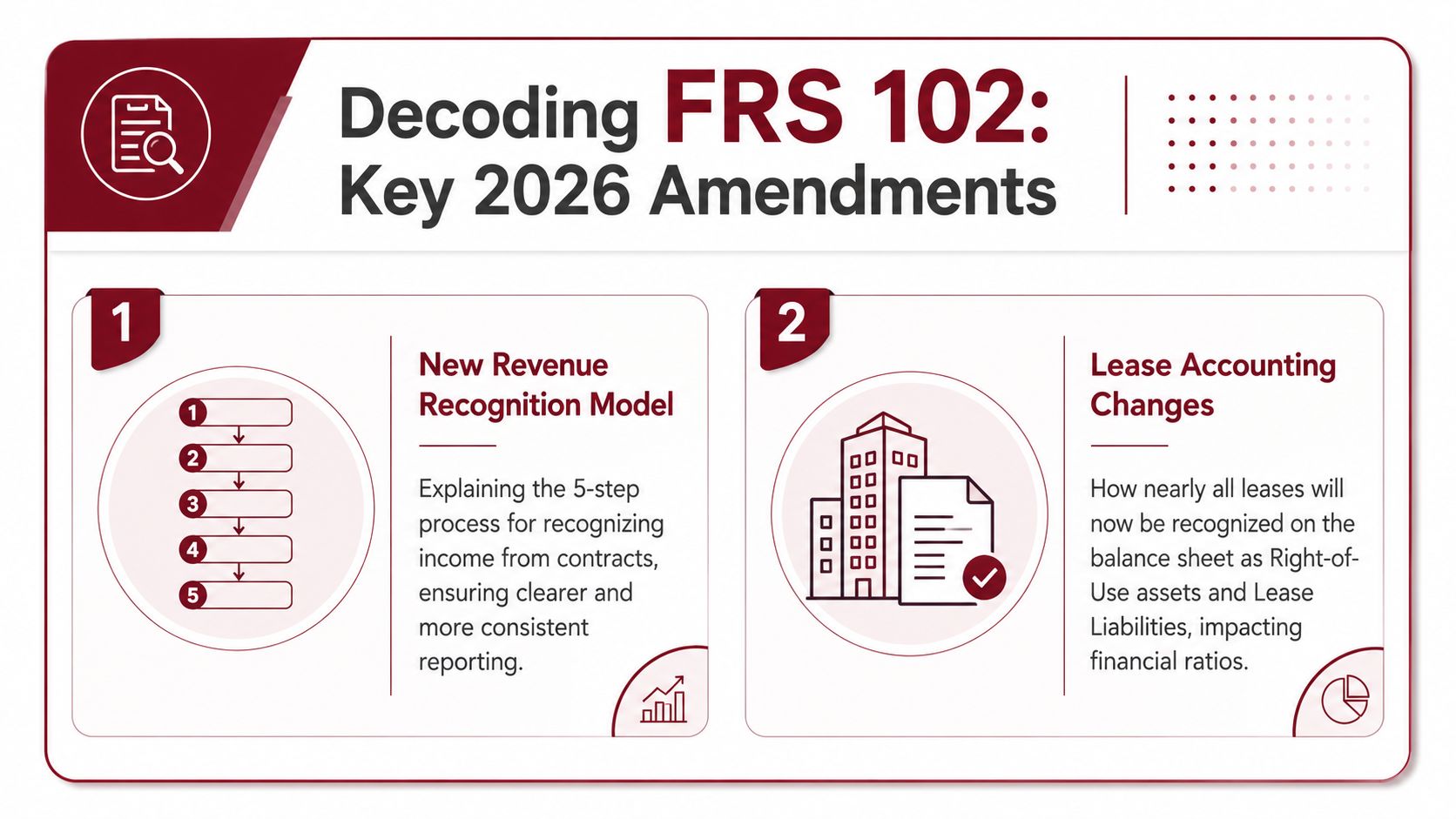

Decoding the Core FRS 102 Amendments for 2026

The Financial Reporting Council issued substantial amendments to FRS 102 on 27 March 2024, introducing a five-step revenue recognition model aligned with IFRS 15. The changes are effective for accounting periods beginning on or after 1 January 2026, early adoption is allowed only if all amendments are adopted simultaneously, and disclosure of supplier finance arrangements is required for periods beginning on or after 1 January 2025, as outlined in RSM UK's summary of the FRS 102 amendments.

Revenue now follows obligations, not habit

Under the new model, revenue recognition becomes more disciplined. In plain English, you need to look at what you promised the customer, work out the price, split that price across the promises if needed, and recognise revenue when each obligation is satisfied.

Think of a contract like a building project or a software implementation. If the job contains distinct pieces of work, the accounting may need to follow those pieces rather than your normal invoicing cycle. Sending an invoice doesn't automatically settle the accounting question. Delivery does.

The five-step structure is straightforward in theory:

- Identify the contract

- Identify the performance obligations

- Determine the transaction price

- Allocate the price to the obligations

- Recognise revenue when each obligation is satisfied

That sounds technical, but the commercial message is simple. Your contract wording matters more. So does the timing of handover, sign-off, milestones, and bundled services.

If your current records are loose, tighten them. Good contract administration and small business accounting processes will matter more under the revised rules.

Leases move onto the balance sheet

The other major shift is lease accounting for lessees. Many businesses are used to treating an office, vehicle, or equipment lease as a regular expense through the profit and loss account. That old simplicity is disappearing for many lease arrangements.

Instead, the business may need to recognise a right-of-use asset and a lease liability on the balance sheet. That changes how the accounts look. It can also change how outside parties read them.

A few consequences follow immediately:

- Balance sheets get larger because both an asset and liability are recorded.

- Profit presentation changes because the pattern of expense recognition differs from a simple rent charge.

- Ratios may move even though the cash going out each month is unchanged.

The headline point is this. The lease didn't become more expensive. Your reporting became more transparent.

That distinction matters when you explain the numbers to a lender, investor, or buyer.

Why These Changes Matter to Your Business

These changes matter because accounts are not just a compliance file. They're the document banks review, investors question, and buyers scrutinise. A shift in revenue timing or lease presentation can alter the story your numbers tell, even if your trading position hasn't changed overnight.

Your accounts may look different even if cash stays the same

Owners often get caught out. They focus on cash and assume the accounts will broadly follow. Sometimes they won't. Lease liabilities can push gearing higher on paper. Revenue recognised later can compress reported profit in one period and push it into another. Net assets may move. EBITDA-style discussions may also feel different depending on the business.

That creates practical problems:

- Bank conversations can become harder if covenants or affordability reviews rely on figures that now look different.

- Investor reporting can become less comparable if prior expectations were built on old presentation.

- Business valuations may need more explanation because reported results no longer map neatly to old patterns.

If you're self-employed or a director whose borrowing depends on business figures, clean, well-explained accounts become even more important. Alongside your accountant, a broker familiar with owner-managed business income can help. This guide on EHF Mortgages self-employed help is useful if your personal lending case depends on understanding how accounts are read.

Construction firms and landlords should pay attention early

Construction businesses are especially exposed because staged delivery, variations, retention issues, and milestone billing rarely fit a simplistic revenue model. If your contract says one thing, your invoice says another, and your site progress says something else, the accounting judgement becomes more important.

Landlords and property investors also need to pay attention. Head leases, longer property commitments, and mixed-use arrangements can affect presentation and decision-making. Even if the economics of the deal remain sensible, the reported position may look heavier on liabilities.

That matters when checking whether your business still fits assumptions around lending, dividend planning, or audit exemption thresholds.

Before you speak to the bank, model the reporting impact. Don't let them discover it before you do.

Micro-entities face a hidden reporting jump

This is the trap too many guides gloss over. Some micro-entities that have operated with a lighter reporting burden may find the lease-related changes drag them into a more demanding framework. Once that happens, the issue isn't just lease accounting. It's the extra disclosure burden that comes with it.

According to ACCA's discussion of the FRS 102 amendments, 65% of micro-entities in the construction sector were unaware that lease accounting changes could force them to adopt FRS 102, bringing in additional related-party and going concern disclosures that had previously been voluntary.

Small doesn't mean sheltered. A micro-entity can still hit a reporting step-up very quickly if lease arrangements push it there.

That's why businesses with connected parties, director loans, family ownership, or informal support arrangements should review disclosure implications now, not after draft accounts are prepared.

A short technical explainer can also help reset the team's understanding before implementation starts:

Your Critical FRS 102 Transition Timeline

The timeline matters because these changes don't arrive as one tidy admin task. They arrive through contracts, disclosures, system updates, and judgement calls. If you treat this as a final-quarter job, you'll create avoidable pressure.

Key dates you can't ignore

Use this as your baseline roadmap.

| Amendment | Effective Date | Key Impact Area |

|---|---|---|

| Supplier finance arrangement disclosures | For periods beginning on or after 1 January 2025 | Cash flow and financing disclosures |

| Main FRS 102 amendments including revenue and leases | For periods beginning on or after 1 January 2026 | Revenue recognition, lease accounting, wider reporting changes |

The date that catches many owners first is the supplier finance disclosure requirement. That arrives earlier than the main package, so don't assume everything waits until 2026.

The compliance cliff for early adopters

Here's the part that SMEs keep missing. Early adoption sounds flexible, but it isn't flexible in the way often assumed. You don't get to cherry-pick the convenient pieces.

As explained in EY's review of the FRS 102 periodic update, 78% of UK SMEs in ACCA's 2025 survey were confused about whether partial adoption was viable. It wasn't. If you early adopt, you must adopt every amendment simultaneously.

That creates a real compliance cliff.

You might be ready on leases but not revenue. Or ready on revenue but not fair value or disclosures. In operational terms, partial readiness gives you nothing. If one strand is incomplete, early adoption falls away.

Decision point: Don't say you're “nearly ready” for early adoption. You're either ready across the full package or you're not.

That's why SMEs should stop treating early adoption as a casual option. It's a strategic choice with an all-or-nothing threshold.

A practical timeline for busy SMEs

A sensible plan looks like this:

-

Assess in the current preparation window

Pull every lease, customer contract, and finance arrangement into one review file. Identify what could trigger a reporting change and where judgement will be needed. -

Plan during 2025

Model the accounting impact. Test draft numbers. Check whether your software can cope with lease schedules, revised revenue treatment, and expanded disclosures. -

Implement before the first live reporting cycle

Lock down policies, train staff, update management accounts, and brief stakeholders before the first affected accounts are prepared.

Use that sequence to avoid scramble. The businesses that cope best won't be the cleverest. They'll be the ones that organised the groundwork early.

Real-World Examples of the New Accounting

Examples make this easier. The rules are technical, but the business impact is very familiar once you see it in context.

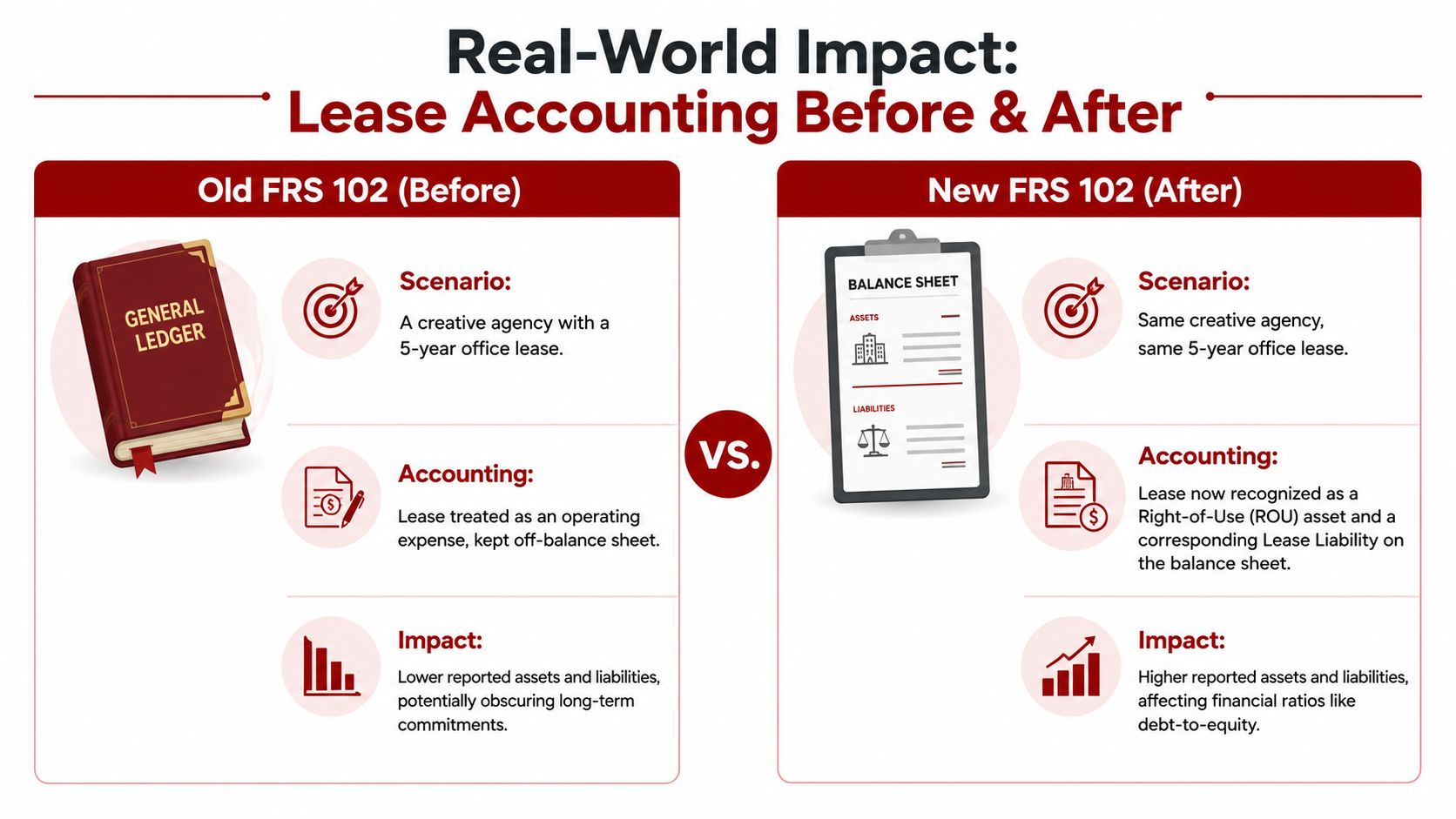

Example one office lease before and after

A creative agency signs a multi-year office lease. Under the old habit, the rent is often treated as a straightforward operating cost in the profit and loss account. The lease commitment is commercially important, but the balance sheet doesn't fully show that long-term obligation in the same way.

Under the revised approach, the same lease is more likely to appear as a right-of-use asset and a lease liability. The office hasn't changed. The monthly payment hasn't changed. What changes is the visibility of the commitment in the accounts.

That can affect how directors, lenders, and buyers read the balance sheet. It may also change how impairment and value discussions are framed in wider reporting work, particularly where intangible and balance sheet judgement already matter in areas like goodwill impairment testing.

Example two staged contract revenue

Now take a construction subcontractor working on a project with design input, mobilisation, staged on-site work, and final completion. Under an older mindset, the business may have recognised revenue largely in line with applications, invoices, or monthly routines.

The new model pushes management to ask a sharper question. What exactly was promised, and when was each obligation satisfied?

That may lead to a different timing pattern:

- Early mobilisation work might not justify the same revenue pattern the invoice suggests.

- Distinct stages may need separate assessment.

- Final sign-off items could hold back recognition on part of the arrangement.

Revenue now follows performance more closely. If your contract administration is weak, the accounting will expose it.

This isn't necessarily bad news. In some cases it produces cleaner, more defensible reporting. But it does mean project managers, commercial managers, and finance staff need to align. If they all describe the job differently, the year-end becomes messy very quickly.

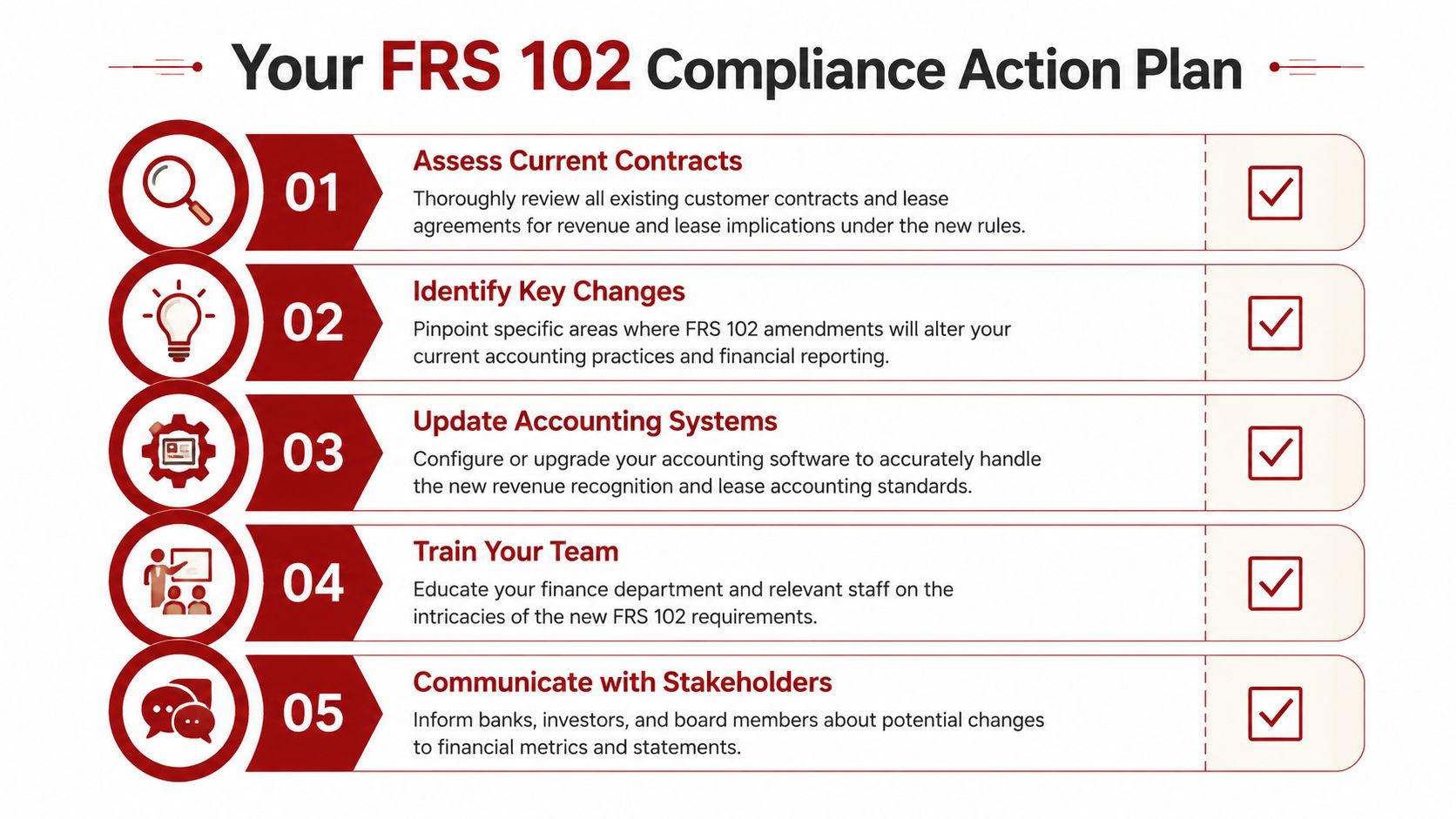

Your FRS 102 Compliance Action Plan

You don't need a giant transformation programme. You need a disciplined checklist and someone senior taking ownership. The worst approach is passive optimism.

Start with contracts, not software

Businesses often start by asking whether Xero, QuickBooks, or another platform can handle the changes. That's the wrong first question. Software only processes what you tell it. If you haven't reviewed the underlying contracts, the system won't save you.

Use this working checklist:

- Gather every live lease: Include offices, vehicles, equipment, and any property arrangements that create ongoing obligations.

- Review customer contracts properly: Look for milestones, bundled services, staged delivery terms, variable consideration, and acceptance clauses.

- Map the pressure points: Note where the new treatment could alter profit timing, liabilities, disclosures, or stakeholder reporting.

- Test management information: Make sure internal reporting can reflect the revised treatment, not just statutory accounts.

Build a transition file before year-end pressure hits

Once the contracts are reviewed, build a practical transition file and keep it updated. That file should include draft accounting positions, policy decisions, judgement notes, and a list of stakeholders who need briefing.

A good file usually covers:

- Draft accounting papers for leases and revenue positions

- Disclosure requirements for entities moving into fuller FRS 102 reporting

- Bank and investor communications where ratios or reported trends may look different

- Team training notes so operations and finance use the same language

- A year-end checklist aligned to revised reporting requirements, such as this 2026 year-end accounts checklist

If you do only one thing this month, nominate an owner and start the review. That alone will put you ahead of businesses still treating the frs 102 changes as an abstract future issue.

How Action Accountants Can Secure Your Transition

Most businesses don't struggle because the rules are impossible. They struggle because the work cuts across contracts, bookkeeping, software, disclosures, tax conversations, and stakeholder communication. Someone has to bring that together properly.

That's where specialist support matters. A firm that works closely with UK SMEs, construction contractors, property investors, and founders can help you assess exposure early, model the impact on your accounts, update systems, and document the judgements that sit behind the numbers.

The right support should be practical. You need clear answers on lease treatment, revenue timing, disclosure exposure, and the knock-on effect on bank conversations or investor reporting. You also need a team that can move quickly when year-end pressure builds.

If your business is affected by the FRS 102 changes, the sensible move is to get ahead of them now. Review the contracts. Model the impact. Fix the weak spots before the first mandatory reporting period arrives.

If you want clear, no-nonsense help with the FRS 102 changes, Action Accountants Limited can help you review the impact on your business, prepare your systems and records, and move into the new reporting rules with confidence.