What Is Invoice Discounting? UK Business Guide 2026

Action Accountants •2 July 2026

Invoice discounting is a business finance solution where a company borrows money against its outstanding invoices, getting an immediate cash injection instead of waiting weeks or months for clients to pay. In the UK, the invoice finance and asset-based lending sector supported businesses with over £22 billion in funding at the end of 2025, which tells you this isn't a fringe option. It's a mainstream way for SMEs to steady cash flow when customers are slow to pay.

If you're reading this, there's a good chance your sales look fine on paper but your bank balance says something else. You've done the work, sent the invoice, and now you're stuck waiting while payroll, VAT, suppliers, and subcontractors all want paying now.

That gap is where good businesses get squeezed. It happens all the time in construction, trade services, and growing B2B firms. Revenue alone doesn't keep the lights on. Cash does.

So, what is invoice discounting in practical terms? It's a way to turn your unpaid invoices into working capital without handing over your entire customer relationship. Used properly, it can take pressure off your day-to-day trading. Used badly, it can lock you into a facility that doesn't fit your business.

You need to understand the mechanics, the cost, and whether your invoicing process is clean enough for a lender to back it. That's what matters.

Table of Contents

- How Invoice Discounting Unlocks Your Cash Flow

- Confidential or Disclosed Which Path to Choose

- The Real Costs and Eligibility for Your Business

- Is Invoice Discounting Right for Your Company

- Invoice Discounting vs Factoring and Other Finance

- Notes for Construction and CIS Clients

- How Action Accountants Can Guide Your Funding Strategy

How Invoice Discounting Unlocks Your Cash Flow

A common small business problem looks like this. You finish the job, raise the invoice, pay wages, cover fuel, materials, and VAT, then wait 30, 60, or 90 days to get paid. In construction, that gap can be worse because applications, valuations, retentions, and CIS deductions slow everything down.

Invoice discounting lets you access cash from invoices you have already raised, instead of waiting for the customer to pay in full. The lender advances a large share of the invoice value up front, then releases the remainder, less fees, once payment comes in.

That matters because profit does not pay this week's supplier bill. Cash does.

If you want to optimize your business cash flow, invoice discounting is often a practical option for B2B firms with decent customers and a steady sales ledger. It ties funding to work you have already billed, which is usually a better fit than stretching an overdraft to cover late payments.

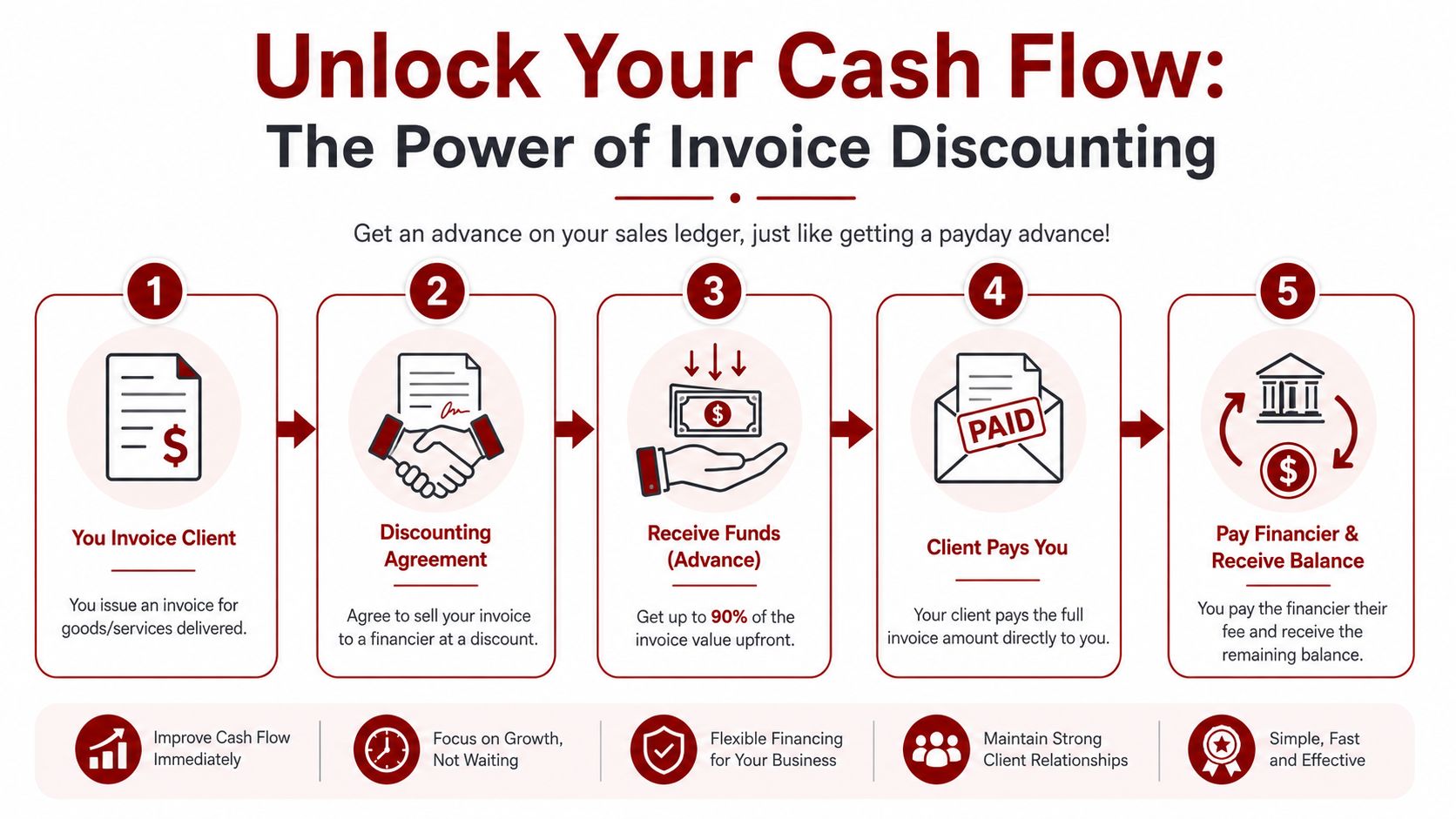

The process in plain English

Here's the usual sequence.

- You issue an invoice after supplying goods or services.

- You assign that invoice to the finance provider under your facility terms.

- The provider advances most of the invoice value, giving you cash far sooner than your payment terms would allow.

- Your customer pays the invoice, and you receive the balance after the lender deducts its fees and any agreed charges.

Simple on paper. Less simple if your records are messy.

Invoice discounting works well when invoices are accurate, paperwork is complete, and customer accounts are kept up to date. Lenders care about the quality of your ledger as much as the quality of your customers. If invoices go out late, disputes drag on, or credit notes appear after submission, the facility becomes harder to set up and harder to use.

Construction firms need to be even more disciplined. If your invoices depend on applications for payment, proof of delivery, timesheets, stage sign-off, or contract valuations, the finance provider will look closely at how those documents support each debt. CIS businesses also need to separate what has been genuinely invoiced from what is still tied up in certification or retention.

My advice is simple. Get your invoicing process under control before you apply. Raise invoices promptly, reconcile the ledger every month, and deal with disputes before they age. If your cash keeps tightening, review the wider process as well. This guide on how to improve cash flow will help you fix the habits causing the pressure, not just plug the gap.

Confidential or Disclosed Which Path to Choose

There isn't just one version of invoice discounting. The main choice is whether you want the arrangement kept behind the scenes or made visible to your customers.

That decision affects control, perception, and access.

Confidential discounting suits businesses that want control

With confidential invoice discounting, you stay front and centre with your customer. You continue managing the sales ledger, credit control, and day-to-day payment conversations. Your clients typically won't see a finance provider stepping into the relationship in an obvious way.

This is usually the better route for established businesses with decent internal systems. If you've built trust with clients and you don't want a third party muddying the tone of collections, confidential discounting is the cleaner option.

It also suits firms that issue regular invoices to repeat customers and already have organised back-office procedures.

Disclosed discounting can be easier to access

With disclosed discounting, the lender's role is visible. That can feel less attractive at first, but don't dismiss it too quickly. For newer businesses or firms without strong in-house credit control, it can be the more realistic route.

The trade-off is simple:

- Choose confidential if preserving customer-facing control is the priority.

- Choose disclosed if access to funding matters more than keeping the arrangement invisible.

- Choose neither until your contracts, invoice wording, and payment terms are watertight.

That last point matters. A weak contract causes more problems in invoice finance than many owners realise. If payment terms are vague or your right to invoice is open to challenge, the lender will price for risk or walk away. This guide on everything businesses need to know about creating business contracts is worth reading before you sign any facility.

The best facility isn't the one with the nicest sales pitch. It's the one your operations can actually support.

If your ledger is disciplined and your customer relationships are valuable, confidential is usually the stronger choice. If you're still building systems and need funding sooner, disclosed may get you over the line. Pick based on reality, not pride.

The Real Costs and Eligibility for Your Business

Invoice discounting helps cash flow, but it is not cheap. If your margins are already tight, especially in construction, the wrong facility will drain profit as quickly as it releases cash.

Price it properly before you sign anything. The headline rate is only part of the story.

Where the cost sits

Most invoice discounting facilities include two core charges.

- Discount fee. The cost of getting an advance against unpaid invoices.

- Service fee. The cost of running the facility, including reporting, administration, and account management.

Many providers also add fees for onboarding, audits, minimum usage, renewals, amendments, or early exit. That is where owners get caught out. A low quoted rate can still turn into an expensive facility once the extras start stacking up.

Use this table when you review terms:

| Cost area | What to check |

|---|---|

| Discount fee | How it is calculated and when the charge starts |

| Service fee | Whether it is fixed, variable, or linked to ledger size |

| Extra charges | Audit fees, renewal fees, minimum volume clauses, termination terms |

| Contract limits | Notice periods, lock-ins, and personal guarantee wording |

Get the full fee schedule in writing. Read every line. Do not rely on a broker summary or a lender saying the rest is standard.

If you cannot explain the charges in plain English, do not sign the agreement.

For UK SMEs in construction, look even harder at the small print. Retentions, pay less notices, valuation disputes, and contract variations can all affect what the lender will fund and what they will exclude. A facility that looks fine for a straightforward service business can be a poor fit for a subcontractor under CIS.

What lenders usually want to see

Lenders are funding your invoices, but they are judging your systems at the same time. They want evidence that your invoices are valid, your records are current, and your customers pay on terms that can be tracked and enforced.

They usually look for:

- Business-to-business sales rather than consumer work or cash takings

- A tidy sales ledger with clear invoice history and limited disputes

- Credit control that is done consistently so old debts do not drift

- More than one meaningful customer instead of heavy reliance on a single account

- Trading records they can verify through accounts, bank statements, bookkeeping, and reconciliations

Construction and CIS firms face a tougher review. That is normal. Applications often stall because the paperwork is incomplete, applications for payment do not match invoices, or retention terms are poorly documented. You can still get approved, but your file needs to be cleaner than average.

Before you approach a provider, get your debtor list, reconciliations, contracts, invoice copies, proof of delivery, and payment terms in order. If those basics need work, practical ways an accountant can help your small business will show you where proper support saves time, avoids errors, and puts you in a stronger position with lenders.

Is Invoice Discounting Right for Your Company

The right question isn't “can I get it?”. The right question is “will it improve the business after fees, admin, and lender control are taken into account?”

That answer depends on how you trade.

When it makes sense

Invoice discounting is often a good fit when your business is profitable, invoicing regularly, and being stretched by payment timing rather than lack of demand.

It tends to suit companies that:

- Invoice other businesses on terms and can't afford to wait for cash to land.

- Need working capital that rises with sales instead of a static facility.

- Want to keep chasing their own debtors rather than handing collections to a third party.

- Are growing quickly and need cash to fund wages, materials, and supplier payments before customer money arrives.

This matters for limited companies in particular, because the structure, liability, and funding choices need to line up. If you're still deciding how your business should be set up, review limited company vs sole trader before layering on invoice finance.

When you should think twice

Invoice discounting won't fix a broken business model. It won't rescue poor margins, chaotic admin, or customers who constantly dispute invoices.

Be cautious if any of these sound familiar:

- Your invoices are often challenged because scope, sign-off, or pricing isn't clear.

- Your ledger is concentrated in one or two major customers.

- You need long-term capital for equipment, expansion, or structural investment.

- You struggle with bookkeeping discipline and only update records when someone chases you.

- You're uncomfortable with legal commitments such as guarantees, fixed terms, or restrictive covenants.

There's also the human side. Some owners like the immediate relief and then become dependent on it. That's dangerous. The facility should support operations, not become the only thing holding them together.

A short explainer can help you think through the trade-offs before committing.

Decision test: If faster access to invoice cash will help you trade better, invoice discounting may fit. If you're using it to plug repeated losses or disorder, fix the business first.

Invoice Discounting vs Factoring and Other Finance

If you're comparing options properly, don't stop at “what is invoice discounting”. Ask what problem you're trying to solve and who you want controlling customer payments.

In the UK, the invoice finance and asset-based lending sector supported businesses with over £22 billion in funding at the end of 2025 according to UK Finance's invoice finance and asset-based lending commentary. That tells you the market is established. It doesn't tell you which product is right for your business.

Invoice Discounting vs. Invoice Factoring at a Glance

The biggest difference between discounting and factoring is control of the sales ledger.

| Feature | Invoice Discounting | Invoice Factoring |

|---|---|---|

| Sales ledger control | You keep control | Provider usually manages collections |

| Customer contact | You continue chasing payment | Provider contacts customers for payment |

| Visibility to customer | Often more discreet | Usually more visible |

| Suitability | Better for firms with stronger internal systems | Better for firms needing more support with collections |

| Brand and relationship impact | More control over tone and timing | Less control over how collections are handled |

| Admin burden | More work stays with you | More administration shifts to the provider |

If you want a separate plain-English overview, you can learn about invoice factoring from MCA Pay. It's useful if you're deciding whether you want funding only or funding plus outsourced credit control.

Where discounting sits among other finance options

Factoring isn't the only alternative. You might also consider an overdraft, a term loan, or trade credit arrangements.

Here's the practical difference:

- Overdrafts are useful for short-term dips, but they're still bank-led and often limited.

- Term loans work better for planned investment, not for bridging slow-paying customers.

- Trade credit helps with supplier timing, but it doesn't solve your own debtor lag.

- Invoice discounting follows your invoicing activity, so it can flex with trading when sales rise.

That flexibility is the main attraction. The weakness is that it relies on a good ledger. If your invoicing process is sloppy, the facility will feel fragile.

The cleanest rule is this. Choose discounting when you have a decent accounts function and want to stay in charge. Choose factoring when cash flow is tight and you also need external help collecting debts. Choose a loan when the money is for investment rather than live receivables.

Notes for Construction and CIS Clients

Construction businesses have a different cash flow rhythm. Applications for payment, valuation disputes, retention, stage billing, and CIS deductions all complicate what looks like a simple invoice on paper.

That's why some lenders hesitate. They don't just want to see an invoice. They want confidence that the amount is due, properly supported, and likely to be paid without argument.

Why construction firms need a different approach

For subcontractors and contractors under CIS, invoice discounting can still work, but the facility has to reflect commercial reality.

A sensible lender will look closely at:

- Certified amounts rather than informal expectations.

- Net invoice values where CIS deductions affect what's received.

- Contract wording around payment milestones, variations, and sign-off.

- Retention exposure so future deductions don't distort the ledger.

If you're in construction, don't walk into a generic facility and hope for the best. A lender that doesn't understand staged payments can create more friction than relief.

The answer is structure, not avoidance. Present clean applications, reconcile deductions properly, and keep backup paperwork ready. In this sector, cash flow problems often come from documentation gaps as much as payment delays.

How Action Accountants Can Guide Your Funding Strategy

You win a decent contract, send the invoice, and still feel short of cash three weeks later. Payroll is due, suppliers want paying, and the bank balance does not care that money is technically on the way. That is the point where funding decisions need proper accounting input, not a rushed application.

A facility only works if it suits your trading pattern, the quality of your sales ledger, and the way your accounts are kept. At Action Accountants, we start by checking the actual cause of the pressure. If slow cash comes from weak credit control, disputed invoices, poor job costing, or messy bookkeeping, adding finance too early usually adds cost without fixing the problem.

Good funding decisions start before the application

The first job is a proper cash flow review. We look at who pays late, which invoices are regularly queried, how much of the ledger a lender is likely to accept, and whether your reporting is reliable enough to support a facility. Those points decide whether invoice discounting will improve cash flow or give short-term relief at the wrong price.

Construction firms need even more care. If you need a refresher on Construction Industry Scheme basics, get that clear first. CIS deductions, payment notices, retention, and contract wording all shape what a lender will fund, especially where stage payments and certification slow everything down.

Implementation matters as much as approval

Getting approved is only half the job. The bigger issue is choosing a lender that fits your business and setting the facility up so it works in day-to-day trading.

That means:

- Preparing clean records so the lender gets answers quickly and does not price in avoidable risk.

- Checking the terms carefully so minimum fees, lock-in periods, personal guarantees, and notice clauses are understood before you sign.

- Making sure bookkeeping is accurate so debtor reports, VAT, and management accounts stay consistent.

- Reviewing the facility after launch so it supports the business instead of becoming a habit that hides deeper margin or collection problems.

That is where experienced advice pays for itself. A generic broker may push whichever lender says yes fastest. A good accountant checks whether the funding still makes sense after fees, reserves, and admin are taken into account.

If you want clear advice on whether invoice discounting suits your business, speak to Action Accountants Limited. They work with UK SMEs, including construction and CIS clients, to improve cash flow, prepare lender-ready financials, and help you make better decisions about funding.